Sysco 2013 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2013 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

|

|

SYSCO CORPORATION-Form10-K 55

PARTII

ITEM8Financial Statements and Supplementary Data

and lending transactions that are offset in accordance with GAAP or are subject to an enforceable master netting arrangement or similar agreement. The

disclosure requirements continue to be effective for annual reporting periods, and interim periods within those years, beginning on or after January1,2013,

which will be scal 2014 for Sysco. Based on the scope clari cation of this update, Sysco does not believe it has any nancial instruments requiring these

disclosures but will continue to evaluate this assessment.

Reporting of Amounts Reclassifi ed Out of Accumulated Other Comprehensive Income

In February2013, the FASB issued ASU 2013-02, “Reporting of Amounts Reclassi ed Out of Accumulated Other Comprehensive Income.” This update

amends ASC 220, “Comprehensive Income,” to require an entity to report the effect of signi cant reclassi cations out of accumulated other comprehensive

income on the respective line items in net earnings if the amount is being reclassi ed in its entirety to net earnings. For other amounts that are not being

reclassi ed in their entirety to net earnings, an entity is required to cross-reference other disclosures that provide additional detail about those amounts.

The amendments in this update are effective prospectively for scal years, and interim periods within those years, beginning after December15,2012,

which is scal 2014 for Sysco. Sysco is currently evaluating the impact this update will have on its disclosures.

Inclusion of the Fed Funds Effective Swap Rate(or Overnight Index Swap Rate) as a Benchmark

Interest Rate for Hedge Accounting Purposes

In July2013, the FASB issued ASU 2013-10, “Inclusion of the Fed Funds Effective Swap Rate(or Overnight Index Swap Rate) as a Benchmark Interest Rate

for Hedge Accounting Purposes.” This update amends ASC 815, “Derivatives and Hedging,” to permit the Fed Funds Effective Swap rate to be used as a

benchmark interest rate for hedge accounting purposes in addition to U.S. Treasury rates and the London Interbank Offered Rate swap rate. The update also

removes the restriction on using different benchmark rates for similar hedges. The amendments in this update are effective prospectively for new or redesignated

hedging relationships entered into on or after July17,2013. Sysco will consider all available benchmark interest rates for any new hedging relationships.

Presentation of an Unrecognized Tax Benefi t When a Net Operating Loss Carryforward, a Similar

Tax Loss, or a Tax Credit Carryforward Exists

In July2013, the FASB issued ASU 2013-11, “Presentation of an Unrecognized Tax Bene t When a Net Operating Loss Carryforward, a Similar Tax Loss,

or a Tax Credit Carryforward Exists.” This update amends ASC 740, “Income Taxes,” to require that in certain cases, an unrecognized tax bene t, or portion

of an unrecognized tax bene t, should be presented in the nancial statements as a reduction to a deferred tax asset for a net operating loss carryforward,

a similar tax loss, or a tax credit carryforward when such items exist in the same taxing jurisdiction. The amendments in this update are effective for

scal years, and interim periods within those years, beginning after December15,2013, which is scal 2015 for Sysco. Early adoption is permitted. The

amendments should be applied prospectively to all unrecognized tax bene ts that exist at the effective date, and retrospective application is permitted.

Sysco is currently evaluating the impact this update will have on its nancial statements.

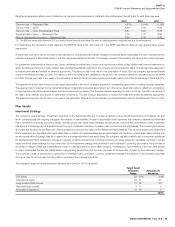

NOTE4 Fair Value Measurements

Fair value is de ned as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date (i.e. an exit price). The accounting guidance includes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure

fair value. The three levels of the fair value hierarchy are as follows:

•Level1– Unadjusted quoted prices for identical assets or liabilities in active markets;

•

Level2– Inputs other than quoted prices in active markets for identical assets and liabilities that are observable either directly or indirectly for substantially

the full term of the asset or liability; and

•

Level3– Unobservable inputs for the asset or liability, which include management’s own assumption about the assumptions market participants would

use in pricing the asset or liability, including assumptions about risk.

Sysco’s policy is to invest in only high-quality investments. Cash equivalents primarily include time deposits, certi cates of deposit, commercial paper,

high-quality money market funds and all highly liquid instruments with original maturities of three months or less. Restricted cash consists of investments

in high-quality money market funds.