Toyota 2015 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2015 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

TOYOTA MOTOR CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Interest income on nonaccrual receivables is recognized only to the extent it is received in cash. Accounts

are restored to accrual status only when interest and principal payments are brought current and future payments

are reasonably assured. Receivable balances are written-off against the allowance for credit losses when it is

probable that a loss has been realized. Retail receivables class and finance lease receivables class are not placed

generally on nonaccrual status when principal or interest is 90 days or more past due. However, these receivables

are generally written-off against the allowance for credit losses when payments due are no longer expected to be

received or the account is 120 days contractually past due, whichever occurs first.

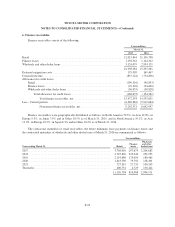

As of March 31, 2015 and 2016, finance receivables on nonaccrual status are as follows:

Yen in millions

March 31,

2015 2016

Retail ............................................................. 7,629 8,107

Finance leases ...................................................... 5,562 682

Wholesale ......................................................... 11,573 16,122

Real estate ......................................................... 8,592 16,801

Working capital ..................................................... 446 822

33,802 42,534

As of March 31, 2015 and 2016, finance receivables 90 days or more past due and accruing are as follows:

Yen in millions

March 31,

2015 2016

Retail ............................................................. 28,147 23,419

Finance leases ...................................................... 3,954 3,984

32,101 27,403

Allowance for credit losses -

Allowance for credit losses is established to cover probable losses on finance receivables and vehicles and

equipment on operating leases, resulting from the inability of customers to make required payments. Provision

for credit losses is included in selling, general and administrative expenses.

The allowance for credit losses is based on a systematic, ongoing review and evaluation performed as part

of the credit-risk evaluation process, historical loss experience, the size and composition of the portfolios, current

economic events and conditions, the estimated fair value and adequacy of collateral and other pertinent factors.

Vehicles and equipment on operating leases are not within the scope of accounting guidance governing the

disclosure of portfolio segments.

Retail receivables portfolio segment -

Toyota calculates allowance for credit losses to cover probable losses on retail receivables by applying

reserve rates to such receivables. Reserve rates are calculated mainly by historical loss experience, current

economic events and conditions and other pertinent factors.

F-14