Verizon Wireless 2006 Annual Report Download - page 25

Download and view the complete annual report

Please find page 25 of the 2006 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

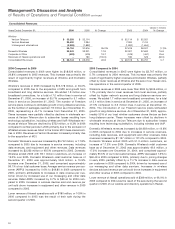

Minority Interest (dollars in millions)

Years Ended December 31, 2006 2005 2004

Minority interest $4,038 $3,001 $ 2,329

The increase in minority interest expense in 2006 compared to 2005,

and in 2005 compared to 2004 was attributable to higher earnings at

Domestic Wireless, which is 45% owned by Vodafone Group Plc

(Vodafone).

Provision for Income Taxes (dollars in millions)

Years Ended December 31, 2006 2005 2004

Provision for income taxes $2,674 $2,421 $ 2,078

Effective income tax rate 32.8% 28.7% 26.1%

The effective income tax rate is the provision for income taxes as a

percentage of income from continuing operations before the provi-

sion for income taxes. Our effective income tax rate in 2006 was

higher than 2005 primarily as a result of favorable tax settlements

and the recognition of capital loss carryforwards in 2005. These

increases were partially offset by tax benefits from foreign opera-

tions and lower state taxes in 2006 compared to 2005.

Our effective income tax rate in 2005 was higher than 2004 due to

taxes on overseas earnings repatriated during the year, lower for-

eign-related tax benefits and lower favorable deferred tax

reconciliation adjustments. Included in the provision of income taxes

in 2005 are capital gains realized in connection with the sale of our

Hawaii business, which resulted in the realization of tax benefits of

$336 million primarily related to capital loss carryforwards. This was

largely offset by a tax provision of $206 million related to the repatri-

ation of foreign earnings under the provisions of the American Jobs

Creation Act of 2004. The effective income tax rate in 2004 was

favorably impacted by the reversal of a valuation allowance relating

to investments, tax benefits related to deferred tax balance adjust-

ments and expense credits that are not taxable.

A reconciliation of the statutory federal income tax rate to the effec-

tive rate for each period is included in Note 16 to the consolidated

financial statements.

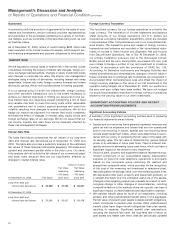

Discontinued Operations

Discontinued operations represents the results of operations of

TELPRI for all years presented in the consolidated statements of

income and Verizon Dominicana, Verizon Information Services and

Verizon Information Services Canada Inc. prior to their sale or spin-

off in December 2006, November 2006 and the fourth quarter of

2004, respectively.

In the second quarter of 2006, we announced our decision to sell

Verizon Dominicana and TELPRI and, in accordance with Statement

of Financial Accounting Standards (SFAS) No. 144, Accounting for

the Impairment or Disposal of Long-Lived Assets, (SFAS No. 144) we

have classified the results of operations of Verizon Dominicana and

TELPRI as discontinued operations. The sale of Dominicana closed

in December 2006 and, primarily due to taxes on previously

unremitted earnings, a pretax gain of $30 million resulted in an after-

tax loss of $541 million (or $.18 per diluted share).

We completed the spin-off of Idearc to our shareholders on

November 17, 2006, which resulted in an $8,695 million increase to

contributed capital in shareowners’ investment.

Discontinued operations also include the results of operations of

Verizon Information Services Canada Inc. prior to its sale in the fourth

quarter of 2004. The sale resulted in a pretax gain of $1,017 million

($516 million after-tax, or $.18 per diluted share).

23

Management’s Discussion and Analysis

of Results of Operations and Financial Condition continued

Income from discontinued operations, net of tax decreased by $611

million, or 44.6% in 2006 compared to 2005. This decrease was pri-

marily due to the after-tax loss recorded in 2006 on the sale of Verizon

Dominicana, partially offset by cessation of depreciation on fixed

assets held for sale. Income from discontinued operations, net of tax

decreased by $562 million, or 29.1% in 2005 compared to 2004. The

decrease was primarily driven by the after-tax gain recorded on the

sale of Verizon Information Services Canada Inc. in 2004.

Cumulative Effect of Accounting Change

In December 2004, the Financial Accounting Standards Board

(FASB) issued SFAS No. 123(R), Share-Based Payment, (SFAS No.

123(R)) which revises SFAS No. 123, Accounting for Stock-Based

Compensation (SFAS No. 123). SFAS No. 123(R) requires all share-

based payments to employees, including grants of employee stock

options, to be recognized as compensation expense based on their

fair value. Effective January 1, 2003, we adopted the fair value

recognition provisions of SFAS No. 123, using the prospective

method (as permitted under SFAS No. 148, Accounting for Stock-

Based Compensation – Transition and Disclosure (SFAS No. 148)) for

all new awards granted, modified or settled after January 1, 2003.

Under the prospective method, employee compensation expense in

the first year is recognized for new awards granted, modified, or set-

tled. The options generally vest over a term of three years, therefore,

the expenses related to stock-based employee compensation

included in the determination of net income for 2006, 2005 and 2004

are less than what would have been recorded if the fair value method

had been applied to previously issued awards.

Effective January 1, 2006, we adopted SFAS No. 123(R) utilizing the

modified prospective method. SFAS No. 123(R) requires the meas-

urement of stock-based compensation expense based on the fair

value of the award on the date of grant. Under the modified prospec-

tive method, the provisions of SFAS No. 123(R) apply to all awards

granted or modified after the date of adoption. SFAS No. 123(R) is

supplemented by Staff Accounting Bulletin (SAB) No. 107, “Share-

Based Payments” (SAB No. 107). This SAB, which was issued by the

Securities and Exchange Commission (SEC) in March 2005,

expresses the views of the SEC staff regarding the relationship

between SFAS No. 123(R) and certain SEC rules and regulations. In

particular, this SAB provides guidance related to valuation methods,

the classification of compensation expense, non-GAAP financial

measures, the accounting for income tax effects of share-based

payment arrangements, disclosures in Management’s Discussion

and Analysis subsequent to adoption of SFAS No. 123(R), and inter-

pretations of other share-based payment arrangements. We also

adopted SAB No. 107 on January 1, 2006.

We recorded a $42 million cumulative effect of accounting change

as of January 1, 2006, net of taxes and after minority interest, to rec-

ognize the effect of initially measuring the outstanding liability

awards (VARs) of the Verizon Wireless joint venture at fair value uti-

lizing a Black-Scholes model. We do not expect SFAS No. 123(R) to

have a material effect on our consolidated financial statements in

future periods.