Verizon Wireless 2006 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2006 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

50

Prior to the merger, there were commercial transactions between us

and the former MCI entities for telecommunications services at

rates comparable to similar transactions with other third parties.

Subsequent to the merger, these transactions are eliminated in

consolidation.

Reasons for the Merger

We believe that the merger will make us a more efficient competitor in

providing a broad range of communications services and will result in

several significant strategic benefits to us, including the following:

•Strategic Position. Following the merger, it is expected that our

core strengths in communication services will be enhanced by

MCI’s employee and business customer base, portfolio of

advanced data and IP services and network assets.

•Growth Platform. MCI’s presence in the U.S. and international

enterprise sector and its long haul fiber network infrastructure

are expected to provide us with a stronger platform from which

we can market our products and services.

•Operational Benefits. We believe that we will achieve operational

benefits through, among other things, eliminating duplicative

staff and information and operating systems and to a lesser

extent overlapping network facilities; reducing procurement

costs; using the existing networks more efficiently; reducing line

support functions; reducing general and administrative

expenses; improving information systems; optimizing traffic flow;

eliminating planned or potential Verizon capital expenditures for

new long-haul network capability; and offering wireless capabili-

ties to MCI’s customers.

Allocation of the Cost of the Merger

In accordance with SFAS No. 141, the cost of the merger was allo-

cated to the assets acquired and liabilities assumed based on their

fair values as of the close of the merger, with the amounts

exceeding the fair value being recorded as goodwill. The process to

identify and record the fair value of assets acquired and liabilities

assumed included an analysis of the acquired fixed assets,

including real and personal property; various contracts, including

leases, contractual commitments, and other business contracts;

customer relationships; investments; and contingencies.

The fair values of the assets acquired and liabilities assumed were

determined using one or more of three valuation approaches:

market, income and cost. The selection of a particular method for a

given asset depended on the reliability of available data and the

nature of the asset, among other considerations. The market

approach, which indicates value for a subject asset based on avail-

able market pricing for comparable assets, was utilized for certain

acquired real property and investments. The income approach,

which indicates value for a subject asset based on the present

value of cash flow projected to be generated by the asset, was

used for certain intangible assets such as customer relationships,

as well as for favorable/unfavorable contracts. Projected cash flow

is discounted at a required rate of return that reflects the relative

risk of achieving the cash flow and the time value of money.

Projected cash flows for each asset considered multiple factors,

including current revenue from existing customers; distinct analysis

of expected price, volume, and attrition trends; reasonable contract

renewal assumptions from the perspective of a marketplace partic-

ipant; expected profit margins giving consideration to marketplace

synergies; and required returns to contributory assets. The cost

approach, which estimates value by determining the current cost of

replacing an asset with another of equivalent economic utility, was

used for the majority of personal property. The cost to replace a

given asset reflects the estimated reproduction or replacement cost

for the property, less an allowance for loss in value due to depreci-

ation or obsolescence, with specific consideration given to

economic obsolescence if indicated.

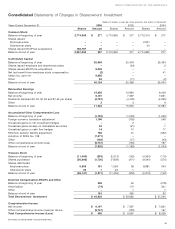

The following table summarizes the allocation of the cost of the

merger to the assets acquired, including cash of $2,361 million, and

liabilities assumed as of the close of the merger. Certain of the

amounts in the following table have been revised since the initial

allocation to reflect information that has since become available.

(dollars in millions)

Assets acquired

Current assets $ 6,001

Property, plant & equipment 6,453

Intangible assets subject to amortization

Customer relationships 1,162

Rights of way and other 176

Deferred income taxes and other assets 1,995

Goodwill 5,085

Total assets acquired $ 20,872

Liabilities assumed

Current liabilities $ 6,093

Long-term debt 6,169

Deferred income taxes and other non-current liabilities 1,720

Total liabilities assumed 13,982

Purchase price $ 6,890

The goodwill resulting from the merger with MCI was assigned to

the Wireline segment, which includes the operations of the former

MCI. The customer relationships are being amortized on a straight-

line basis over 3-8 years based on whether the relationship is with

a consumer or a business customer since this correlates to the pat-

tern in which the economic benefits are expected to be realized.

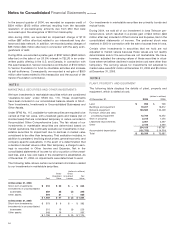

In connection with the merger, we recorded $193 million of sever-

ance and severance-related costs and $427 million of contract

termination costs in the above allocation of the cost of the merger

in accordance with the Emerging Issues Task Force Issue (EITF) No.

95-3, “Recognition of Liabilities in Connection with a Purchase

Business Combination.” We paid $116 million of the severance and

severance-related costs in 2006 with the remaining costs to be paid

in 2007. We paid $128 million of contract termination costs in 2006

and the remaining costs will be paid over the remaining contract

periods through 2009. The following table summarizes the obliga-

tions recognized in connection with the MCI merger and the activity

to date:

(dollars in millions)

Initial Other Ending

Allocation Increases Payments Balance

Severance costs and contract

termination costs $ 459 $ 161 $ (244) $ 376

Notes to Consolidated Financial Statements continued