Verizon Wireless 2006 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2006 Verizon Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

Notes to Consolidated Financial Statements continued

59

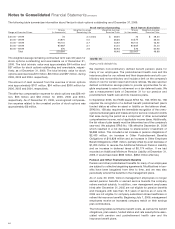

In addition, on January 20, 2006, Verizon announced an offer to

repurchase MCI $1,983 million aggregate principal amount of

5.908% Senior Notes Due 2007 at 101% of their par value. On

February 21, 2006, $1,804 million of these notes were redeemed by

Verizon. Verizon satisfied and discharged the indenture governing

this series of notes shortly after the close of the offer for those

noteholders who did not accept this offer.

Other Debt Redemptions/Prepayments

During the second quarter of 2006, we redeemed/prepaid several

debt issuances, including: Verizon North Inc. $200 million 7.625%

Series C debentures due May 15, 2026; Verizon Northwest Inc. $175

million 7.875% Series B debentures due June 1, 2026; Verizon

South Inc. $250 million 7.5% Series D debentures due March 15,

2026; Verizon California Inc. $25 million 9.41% Series W first mort-

gage bonds due 2014; Verizon California Inc. $30 million 9.44%

Series X first mortgage bonds due 2015; Verizon Northwest Inc. $3

million 9.67% Series HH first mortgage bonds due 2010 and Contel

of the South Inc. $14 million 8.159% Series GG first mortgage bonds

due 2018. The gain/(loss) from these retirements was immaterial.

During the third quarter of 2005, we redeemed Verizon New

England Inc. $250 million 6.875% debentures due October 1, 2023

resulting in a pretax charge of $10 million ($6 million after-tax) in

connection with the early extinguishment of the debt.

Zero-Coupon Convertible Notes

Previously in May 2001, Verizon Global Funding issued approxi-

mately $5.4 billion in principal amount at maturity of zero-coupon

convertible notes due 2021, resulting in gross proceeds of approxi-

mately $3 billion. The notes were convertible into shares of our

common stock at an initial price of $69.50 per share if the closing

price of Verizon common stock on the New York Stock Exchange

exceeded specified levels or in other specified circumstances. The

conversion price increased by at least 3% a year. The initial conver-

sion price represented a 25% premium over the May 8, 2001

closing price of $55.60 per share. The notes were redeemable at the

option of the holders on May 15th in each of the years 2004, 2006,

2011 and 2016. On May 15, 2004, $3,292 million of principal

amount of the notes ($1,984 million after unamortized discount)

were redeemed by Verizon Global Funding. In addition, the zero-

coupon convertible notes were callable by Verizon on or after May

15, 2006. On May 16, 2006, we redeemed the remaining $1,375 mil-

lion accreted principal of the remaining outstanding zero-coupon

convertible principal. The total payment on the date of redemption

was $1,377 million.

Support Agreements

All of Verizon Global Funding’s debt had the benefit of Support

Agreements between us and Verizon Global Funding, which gave

holders of Verizon Global Funding debt the right to proceed directly

against us for payment of interest, premium (if any) and principal

outstanding should Verizon Global Funding fail to pay. The holders

of Verizon Global Funding debt did not have recourse to the stock

or assets of most of our telephone operations; however, they did

have recourse to dividends paid to us by any of our consolidated

subsidiaries as well as assets not covered by the exclusion. On

February 1, 2006, Verizon announced the merger of Verizon Global

Funding into Verizon. As a result of the merger all of Verizon Global

Funding’s debt has been assumed by Verizon by operation of law.

In addition, Verizon Global Funding had guaranteed the debt obli-

gations of GTE Corporation (but not the debt of its subsidiary or

affiliate companies) that were issued and outstanding prior to July

1, 2003. In connection with the merger of Verizon Global Funding

into Verizon, Verizon has assumed this guarantee. As of December

31, 2006, $2,950 million principal amount of these obligations

remained outstanding.

Verizon and NYNEX Corporation are the joint and several co-

obligors of the 20-Year 9.55% Debentures due 2010 previously

issued by NYNEX on March 26, 1990. As of December 31, 2006,

$92 million principal amount of this obligation remained out-

standing. NYNEX and GTE no longer issue public debt or file SEC

reports. See Note 20 for information on guarantees of operating

subsidiary debt listed on the New York Stock Exchange.

Debt Covenants

We and our consolidated subsidiaries are in compliance with all of

our debt covenants.

Maturities of Long-Term Debt

Maturities of long-term debt outstanding at December 31, 2006 are

$4.1 billion in 2007, $2.5 billion in 2008, $1.4 billion in 2009, $2.8

billion in 2010, $2.6 billion in 2011 and $19.4 billion thereafter.

NOTE 12

FINANCIAL INSTRUMENTS

Derivatives

The ongoing effect of SFAS No. 133 and related amendments and

interpretations on our consolidated financial statements will be

determined each period by several factors, including the specific

hedging instruments in place and their relationships to hedged

items, as well as market conditions at the end of each period.

Interest Rate Risk Management

We have entered into domestic interest rate swaps, to achieve a tar-

geted mix of fixed and variable rate debt, where we principally

receive fixed rates and pay variable rates based on LIBOR. These

swaps hedge against changes in the fair value of our debt portfolio.

We record the interest rate swaps at fair value in our balance sheet as

assets and liabilities and adjust debt for the change in its fair value

due to changes in interest rates. The ineffective portions of these

hedges were recorded as gains in the consolidated statements of

income of $4 million for the year ended December 31, 2004.

We also enter into interest rate derivatives to limit our exposure to

interest rate changes. In accordance with the provisions of SFAS

No. 133, changes in fair value of these cash flow hedges due to

interest rate fluctuations are recognized in Accumulated Other

Comprehensive Loss. We recorded Other Comprehensive Income

(Loss) of $14 million and $10 million related to these interest rate

cash flow hedges for the years ended December 31, 2006 and

2005, respectively.

Foreign Exchange Risk Management

From time to time, our foreign exchange risk management has

included the use of foreign currency forward contracts and cross

currency interest rate swaps with foreign currency forwards. These

contracts are typically used to hedge short-term foreign currency

transactions and commitments, or to offset foreign exchange gains

or losses on the foreign currency obligations and are designated as

cash flow hedges. There were no foreign currency contracts out-

standing as of December 31, 2006 and 2005. We record these

contracts at fair value as assets or liabilities and the related gains or

losses are deferred in shareowners’ investment as a component of

Accumulated Other Comprehensive Loss. We have recorded net