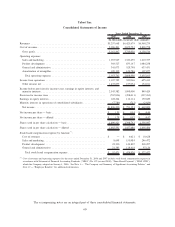

Yahoo 2007 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2007 Yahoo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

|

|

taxes. The valuation allowance decreased by $29 million during the year ended December 31, 2007. The decrease

is mainly due to adjustments to non-U.S. net operating loss carryforwards.

We establish reserves for tax-related uncertainties based on estimates of whether, and the extent to which, additional

taxes will be due. These reserves are established when we believe that certain positions might be challenged despite

our belief that our tax return positions are in accordance with applicable tax laws. Effective January 1, 2007, we

adopted the provisions of FIN 48. See Note 10 — “Income Taxes” in the consolidated financial statements for

additional information.

Goodwill and Other Intangible Assets. Goodwill is tested for impairment at the reporting unit level (operating

segment or one level below an operating segment) on an annual basis and between annual tests in certain

circumstances. Application of the goodwill impairment test requires judgment, including the identification of

reporting units, assigning assets and liabilities to reporting units, assigning goodwill to reporting units, and

determining the fair value of each reporting unit. Significant judgments required to estimate the fair value of

reporting units include estimating future cash flows, and determining appropriate discount rates, growth rates and

other assumptions. Changes in these estimates and assumptions could materially affect the determination of fair

value for each reporting unit which could trigger impairment. See Note 5 — “Goodwill” in the consolidated

financial statements for additional information. Based on our 2007 impairment test, there would have to be a

significant unfavorable change to our assumptions used in such calculations for an impairment to exist.

We amortize other intangible assets over their estimated useful lives. We record an impairment charge on these

assets when we determine that their carrying value may not be recoverable. The carrying value is not recoverable if

it exceeds the undiscounted future cash flows resulting from the use of the asset and its eventual disposition. When

there is existence of one or more indicators of impairment, we measure any impairment of intangible assets based on

a projected discounted cash flow method using a discount rate determined by our management to be commensurate

with the risk inherent in our business model. Our estimates of future cash flows attributable to our other intangible

assets require significant judgment based on our historical and anticipated results and are subject to many factors.

Different assumptions and judgments could materially affect the calculation of the fair value of our other intangible

assets which could trigger impairment.

Investments in Equity Interests. We account for investments in entities in which we can exercise significant

influence but do not own a majority equity interest or otherwise control using the equity method. In accounting for

these investments we record our proportionate share of these entities’ net income or loss, one quarter in arrears.

We review all of our investments in equity interests for impairment whenever events or changes in business

circumstances indicate that the carrying amount of the investment may not be fully recoverable. The impairment

review requires significant judgment to identify events or circumstances that would likely have a significant adverse

effect on the fair value of the investment. Investments identified as having an indication of impairment are subject

to further analysis to determine if the impairment is other-than-temporary and this analysis requires estimating the

fair value of the investment. The determination of the fair value of the investment involves considering factors such

as the following: the stock prices of public companies in which we have an equity investment, current economic and

market conditions, the operating performance of the companies including current earnings trends and undiscounted

cash flows, quoted stock prices of comparable public companies, and other company specific information including

recent financing rounds. The fair value determination, particularly for investments in privately-held companies,

requires significant judgment to determine appropriate estimates and assumptions. Changes in these estimates and

assumptions could affect the calculation of the fair value of the investments and the determination of whether any

identified impairment is other-than-temporary.

Stock-Based Compensation Expense. Effective January 1, 2006, we adopted SFAS 123R using the modified

prospective method and therefore have not restated prior periods’ results. Under the fair value recognition

provisions of SFAS 123R, we recognize stock-based compensation expense net of an estimated forfeiture rate and

therefore only recognize compensation cost for those shares expected to vest over the service period of the award.

Calculating stock-based compensation expense requires the input of highly subjective assumptions, including the

expected term of the stock-based awards, stock price volatility, and the pre-vesting option forfeiture rate. We estimate the

expected life of options granted based on historical exercise patterns, which we believe are representative of future

55