APC 2009 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2009 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

|

|

2009 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC166

CONSOLIDATED FINANCIAL STATEMENTS

5NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

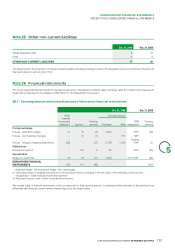

Note29

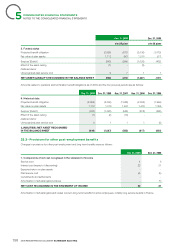

Commitments and contingent liabilities

29.1 - Guarantees given and received

Dec. 31, 2009 Dec. 31 2008

Contract counterguarantees (1) 469 303

Mortgages and collateral (2) 16 23

Guarantees 10 0

Other commitments given (3) 176 123

GUARANTEES GIVEN 671 449

Other guarantees received 64 53

GUARANTEES RECEIVED 64 53

(1) On certain contracts, customers require a guarantee from a bank that the contract will be fully executed by the Group. For these

contracts, the Group gives a counterguarantee to the bank. If a claim occurs, the risk linked to the commitment is assessed and a

provision for contingencies is recorded when the risk is considered probable and can be reasonably estimated.

(2) Certain loans are secured by property, plant and equipment and securities lodged as collateral.

(3) Other guarantees given comprise guarantees to certain lessors that rental payments will be made until the end of the lease.

29.2 - Purchase commitments

Shares in subsidiaries and affiliates

Commitments to purchase equity investments correspond to put

options given to minority shareholders in consolidated companies

or relate to earn-out payments. The amount of these commitments

was not material at December 31, 2009.

Information technology services

The Group signed a facilities management contract with CAPGEMINI

in 2004. The reciprocal commitments between CAPGEMINI and

Schneider Electric run until 2016.

The 2009 expense related to this outsourcing agreement amounted

to EUR 119million, including volume and indexation effects provided

for in the contract. This compares with EUR 133million in 2008.

29.3 - Contingent liabilities

Management is confi dent that balance sheet provisions for known

disputes in which the Group is involved are suffi cient to ensure that

these disputes do not have a material impact on its fi nancial position

or profi t. This is notably the case for the potential consequences of

a current dispute in Belgium involving former senior executives and

managers of the Group.

The Group has signed an agreement concerning statutory employee

training rights in France (DIF). In accordance with French national

accounting board (CNC) opinion 2004-F, the related costs are treated

as an expense for the period when the training is received and no

provision is set aside in the periods when the training rights accrue.

As of December 31, 2009, accrued rights corresponded to around

1,200,000 hours.

Note30

Subsequent events

30.1 - Signature of an agreement to acquire

Areva T&D in partnership with Alstom

On January 20, 2010, Alstom and Schneider Electric announced the

signature of an agreement with Areva concerning the acquisition of

Areva T&D. The transaction must still be approved by the appropriate

anti-trust authorities and France’s Holdings & Transfers Committee

(CPT). The deal could be closed in the spring of 2010.

Once the acquisition is completed, Schneider Electric intends to

combine the highly synergistic medium-voltage teams to create a

new Energy Business with revenue of around EUR 4.6billion and

22,000 employees.

30.2 - Acquisition of Cimac

On January 21, 2010, Schneider Electric announced the signature

of an agreement to acquire Cimac, the leading systems integrator

for industrial automation solutions in the Persian Gulf region. Cimac

has more than 400 employees and generates revenue of more than

EUR 40million.

30.3 - Press release issued by France’s national

accounting board (CNC)

on January 14, 2010

On January 14, 2010, France’s national accounting board issued a

press release concerning the accounting treatment of the CET tax

introduced in the French law of December 31, 2009 reforming the

country’s local business tax. The press release explains that the CET

is assessed in part on value added (CVAE) and notes that there is

no clear guidance in IAS12 and the related IFRIC interpretations as

to whether this component should be treated as income tax or an