BB&T 2014 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

Changes in Accounting Principles and Effects of New Accounting Pronouncements

In February 2015, the FASB issued new guidance related to Consolidation. The new guidance provides an additional requirement for a limited partnership or

similar entity to qualify as a voting interest entity and also amends the criteria for consolidating such an entity. In addition, the new guidance amends the

criteria for evaluating fees paid to a decision maker or service provider as a variable interest and amends the criteria for evaluating the effect of fee

arrangements and related parties on a VIE primary beneficiary determination. This guidance is effective for interim and annual reporting periods beginning

after December 15, 2015. The Company is currently evaluating this guidance to determine the impact on its consolidated financial statements.

In August 2014, the FASB issued new guidance related to Receivables. The new guidance requires that a government guaranteed mortgage loan be

derecognized and that a separate other receivable be recognized upon foreclosure if certain conditions are met. This guidance is effective for interim and

annual reporting periods beginning after December 15, 2014. The adoption of this guidance is not expected to be material to the consolidated financial

statements.

In June 2014, the FASB issued new guidance related to Repurchase-to-Maturity Transactions and Repurchase Financings. The new guidance changes the

accounting for repurchase-to-maturity transactions to secured borrowing accounting. The guidance also requires separate accounting for a transfer of a

financial asset executed contemporaneously with a repurchase agreement with the same counterparty, which will result in secured borrowing accounting for

the repurchase agreement. This guidance is effective for interim and annual reporting periods beginning after December 15, 2014. The adoption of this

guidance is not expected to be material to the consolidated financial statements.

In May 2014, the FASB issued new guidance related to Revenue from Contracts with Customers. This guidance supersedes the revenue recognition

requirements in Accounting Standards Codification Topic 605, Revenue Recognition, and most industry-specific guidance throughout the Accounting

Standards Codification. The guidance requires an entity to recognize revenue to depict the transfer of promised goods or services to customers in an amount

that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. This guidance is effective for interim and

annual reporting periods beginning after December 15, 2016. The Company is currently evaluating this guidance to determine the impact on its consolidated

financial statements.

In January 2014, the FASB issued new guidance related to Investments in Qualified Affordable Housing Projects. The new guidance allows an entity,

provided certain criteria are met, to elect the proportional amortization method to account for these investments. The proportional amortization method

allows an entity to amortize the initial cost of the investment in proportion to the amount of tax credits and other tax benefits received and recognize the net

investment performance in the income statement as a component of the provision for income taxes. This guidance is effective for interim and annual

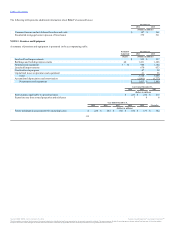

reporting periods beginning after December 15, 2014. See Note 15 “Commitments and Contingencies” for the estimated impact of the adoption of this

guidance.

Effective January 1, 2014, the Company adopted new guidance related to Troubled Debt Restructurings. The new guidance clarifies the timing of when an in

substance repossession or foreclosure of collateralized residential real property is deemed to have occurred and also requires disclosure of the amount of

foreclosed residential real estate property and the recorded investment in consumer mortgage loans collateralized by residential real estate property that are in

the process of foreclosure. The adoption of this guidance was not material to the consolidated financial statements.

Effective January 1, 2014, the Company adopted new guidance related to Investment Companies. The new guidance amends the criteria for an entity to

qualify as an investment company and requires an investment company to measure all of its investments at fair value. The adoption of this guidance was not

material to the consolidated financial statements.

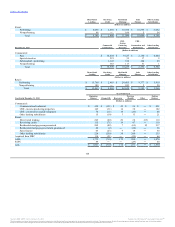

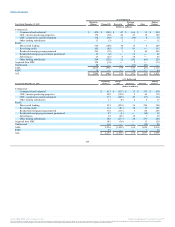

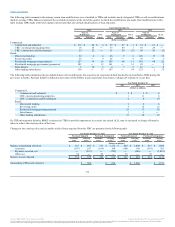

During 2014, BB&T purchased 21 bank branches in Texas from Citigroup, Inc., resulting in the acquisition of $1.2 billion in deposits, $112 million in loans

and $1.1 billion in cash and other assets. Goodwill of $29 million and CDI of $20 million were recognized in connection with the transaction.

During 2012, BB&T completed the acquisition of Fort Lauderdale, Florida-based BankAtlantic. BB&T acquired approximately $1.7 billion in loans and

assumed approximately $3.5 billion in deposits.

BB&T has reached agreements to acquire Susquehanna Bancshares, Inc., The Bank of Kentucky Financial Corporation and additional retail branches in

Texas.

103

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.