BB&T 2014 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

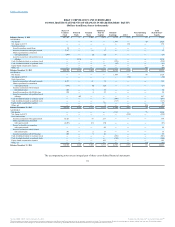

MSRs

BB&T has a significant mortgage loan servicing portfolio with two classes of MSRs for which it separately manages the economic risk: residential and

commercial. Residential MSRs are primarily carried at fair value with changes in fair value recorded as a component of mortgage banking income. BB&T

uses various derivative instruments to mitigate the income statement effect of changes in fair value due to changes in valuation inputs and assumptions of its

residential MSRs. MSRs do not trade in an active, open market with readily observable prices. While sales of MSRs do occur, the precise terms and

conditions typically are not readily available. Accordingly, BB&T estimates the fair value of residential MSRs using an OAS valuation model to project

MSR cash flows over multiple interest rate scenarios, which are then discounted at risk-adjusted rates. The OAS model considers portfolio characteristics,

contractually specified servicing fees, prepayment assumptions, delinquency rates, late charges, other ancillary revenue, costs to service and other economic

factors. BB&T reassesses and periodically adjusts the underlying inputs and assumptions in the OAS model to reflect market conditions and assumptions that

a market participant would consider in valuing the MSR asset.

Fair value estimates and assumptions are compared to industry surveys, recent market activity, actual portfolio experience and, when available, observable

market data. Due to the nature of the valuation inputs, MSRs are classified within Level 3 of the valuation hierarchy. The value of MSRs is significantly

affected by mortgage interest rates available in the marketplace, which influence mortgage loan prepayment speeds. In general, during periods of declining

interest rates, the value of MSRs declines due to increasing prepayments attributable to increased mortgage-refinance activity. Conversely, during periods of

rising interest rates, the value of MSRs generally increases due to reduced refinance activity. Commercial MSRs are carried at the lower of cost or market and

amortized over the estimated period that servicing income is expected to be received based on projections of the amount and timing of estimated future cash

flows. The amount and timing of servicing asset amortization is based on actual results and updated projections. Refer to Note 7 “Loan Servicing” in the

“Notes to Consolidated Financial Statements” for quantitative disclosures reflecting the effect that changes in management’s assumptions would have on the

fair value of MSRs.

LHFS

BB&T originates certain mortgage loans for sale to investors that are carried at fair value. The fair value is primarily based on quoted market prices for

securities backed by similar types of loans. Changes in the fair value are recorded as a component of mortgage banking income, while the related origination

costs are recognized in noninterest expense when incurred. The changes in fair value are largely driven by changes in interest rates subsequent to loan

funding and changes in the fair value of servicing associated with the LHFS. BB&T uses various derivative instruments to mitigate the economic effect of

changes in fair value of the underlying loans.

Derivative Assets and Liabilities

BB&T uses derivatives to manage various financial risks. The fair values of derivative financial instruments are determined based on quoted market prices

and internal pricing models that are primarily sensitive to market observable data. BB&T mitigates the credit risk by subjecting counterparties to credit

reviews and approvals similar to those used in making loans and other extensions of credit. In addition, certain counterparties are required to provide

collateral to BB&T when their unsecured loss positions exceed certain negotiated limits. The fair value of interest rate lock commitments, which are related

to mortgage loan commitments, is based on quoted market prices adjusted for commitments that BB&T does not expect to fund and includes the value

attributable to the net servicing fee.

Private Equity and Similar Investments

BB&T has private equity and similar investments that are carried at fair value. Changes in the fair value of these investments are recorded in other noninterest

income each period. In many cases there are no observable market values for these investments and management must estimate the fair value based on a

comparison of the operating performance of the company to multiples in the marketplace for similar entities. This analysis requires significant judgment, and

actual values in a sale could differ materially from those estimated. As of December 31, 2014, BB&T had $329 million of these investments, which

represented less than 1% of total assets.

84

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.