BB&T 2014 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

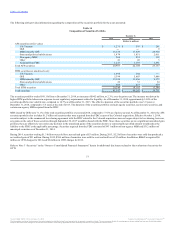

(6) Excludes government guaranteed GNMA mortgage loans that BB&T does not have the obligation to repurchase that are past due 30-89 days totaling $2

million, $4 million, $5 million, $7 million and $7 million at December 31, 2014, 2013, 2012, 2011 and 2010, respectively.

Loans 90 days or more past due and still accruing interest, excluding government guaranteed GNMA mortgage loans, totaled $535 million at December 31,

2014, compared with $722 million at year-end 2013, a decline of 25.9%. Loans 30-89 days past due, excluding government guaranteed GNMA mortgage

loans, totaled $896 million at December 31, 2014, which was a decline of $211 million, or 19.1%, compared to prior year. These reductions reflect continued

improvement in credit quality and the effects of the sale of residential mortgage NPLs as previously discussed.

Asset Quality Ratios (including assets acquired from FDIC)

Loans 30 - 89 days past due and still accruing as a

percentage of loans and leases HFI (1) 0.75 % 0.95 % 1.10 % 1.30 % 1.76 %

Loans 90 days or more past due and still accruing as a

percentage of loans and leases HFI (1) 0.45 0.62 0.75 1.06 1.54

NPLs as a percentage of loans and leases HFI 0.51 0.81 1.20 1.74 2.07

NPAs as a percentage of:

Total assets 0.42 0.64 0.97 1.62 2.40

Loans and leases HFI plus foreclosed property 0.65 1.01 1.56 2.63 3.63

Net charge-offs as a percentage of average loans

and leases HFI (2) 0.46 0.69 1.17 1.60 2.47

ALLL as a percentage of loans and leases HFI 1.23 1.49 1.76 2.10 2.62

Ratio of ALLL to:

Net charge-offs (2) 2.74 x 2.19 x 1.56 x 1.36 x 1.07 x

NPLs 2.39 1.85 1.46 1.21 1.26

Asset Quality Ratios (excluding acquired from FDIC)(3)

Loans 90 days or more past due and still accruing as a

percentage of loans and leases HFI (1) 0.29 % 0.37 % 0.38 % 0.39 % 0.46 %

(1) Excludes government guaranteed GNMA mortgage loans that BB&T has the right but not the obligation to repurchase. Refer to the footnotes of Table

22 for amounts related to these loans.

(2) Net charge-offs for 2011 and 2010 include $236 million and $695 million, respectively, related to BB&T’s NPA disposition strategy. In connection with

this strategy, approximately $271 million and $1.9 billion of problem loans were transferred from loans held for investment to LHFS in 2011 and 2010,

respectively. The disposition of all such loans was complete as of December 31, 2011.

(3) These asset quality ratios have been adjusted to remove the impact of assets acquired from the FDIC. Appropriate adjustments to the numerator and

denominator have been reflected in the calculation of these ratios.

Potential problem loans include loans on nonaccrual status or past due as disclosed in Table 22. In addition, for the commercial portfolio segment, loans that

are rated special mention or substandard performing are closely monitored by management as potential problem loans. Refer to Note 4 “Loans and ACL” in

the “Notes to Consolidated Financial Statements” herein for additional disclosures related to these potential problem loans.

TDRs generally occur when a borrower is experiencing, or is expected to experience, financial difficulties in the near-term. As a result, BB&T will work with

the borrower to prevent further difficulties, and ultimately to improve the likelihood of recovery on the loan. To facilitate this process, a concessionary

modification that would not otherwise be considered may be granted, resulting in classification of the loan as a TDR. Refer to Note 1 “Summary of

Significant Accounting Policies” in the “Notes to Consolidated Financial Statements” for additional policy information regarding TDRs.

BB&T’s performing TDRs, excluding government guaranteed GNMA mortgage loans, totaled $1.1 billion at December 31, 2014, a reduction of $655 million

compared to the prior year. This decline includes the sale of $540 million of performing residential mortgage TDRs during the third quarter of 2014.

59

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.