BB&T 2014 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

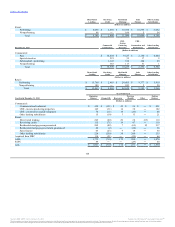

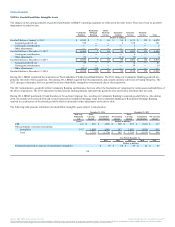

AFS securities:

MBS issued by GSE $ 10,259 $ 406 $ 1,935 $ 140 $ 12,194 $ 546

States and political subdivisions 232 8 441 83 673 91

Securities acquired from FDIC 34 1 ― ― 34 1

Total $ 10,525 $ 415 $ 2,376 $ 223 $ 12,901 $ 638

HTM securities:

U.S. Treasury $ 384 $ 8 $ ― $ ― $ 384 $ 8

GSE 4,996 397 ― ― 4,996 397

MBS issued by GSE 8,800 219 48 1 8,848 220

Total $ 14,180 $ 624 $ 48 $ 1 $ 14,228 $ 625

Periodic reviews are conducted to identify and evaluate each investment with an unrealized loss for OTTI. An unrealized loss exists when the current fair

value of an individual security is less than its amortized cost basis. Unrealized losses that are determined to be temporary in nature are recorded, net of tax, in

AOCI for AFS securities. The unrealized losses on GSE securities and MBS issued by GSE were the result of increases in market interest rates compared to the

date the securities were acquired rather than the credit quality of the issuers.

Cash flow modeling is used to evaluate non-agency MBS in an unrealized loss position for potential credit impairment. These models give consideration to

long-term macroeconomic factors applied to current security default rates, prepayment rates and recovery rates and security-level performance. At December

31, 2014, one non-agency MBS had an immaterial amount of other than temporary credit impairment.

At December 31, 2014, $55 million of the unrealized loss on municipal securities was the result of fair value hedge basis adjustments that are a component of

amortized cost. Municipal securities in an unrealized loss position are evaluated for credit impairment through a qualitative analysis of issuer performance

and the primary source of repayment. At December 31, 2014, the evaluation of municipal securities indicated one municipal security had an immaterial

amount of other than temporary credit impairment.

During the first quarter of 2014, approximately $8.3 billion of nonguaranteed, closed-end, first and second lien position residential mortgage loans, along

with the related allowance, were transferred from direct retail lending to residential mortgage to facilitate compliance with a series of new rules related to

mortgage servicing associated with first and second lien position mortgages collateralized by real estate.

During the first quarter of 2014, the CRE loan categories were realigned into CRE – income producing properties and CRE – construction and development

in order to better reflect the nature of the underlying loans. Prior period data has been reclassified to conform to this new presentation.

During the third quarter of 2014, approximately $550 million of loans, which were primarily performing residential mortgage TDRs, with a related ALLL of

$57 million were sold for a gain of $42 million. During the fourth quarter of 2014, approximately $140 million of loans, which were primarily residential

mortgage NPLs, with a related ALLL of $19 million were sold for a gain of $24 million. Both gains were recognized as reductions to the provision for credit

losses.

Effective October 1, 2014, loans subject to the commercial loss sharing agreement with the FDIC related to the Colonial acquisition were no longer covered

by loss sharing. At December 31, 2014, these loans had a carrying value of $561 million, a UPB of $836 million and an allowance of $38 million and are

included in acquired from FDIC loans. Loans totaling $654 million at December 31, 2014 continue to be covered by loss sharing and are included in the

acquired from FDIC balance.

During 2013, BB&T sold a consumer lending subsidiary with approximately $500 million in loans and $27 million of related ALLL. In addition,

approximately $230 million of loans, with $38 million of related ALLL, was transferred from retail other lending subsidiaries to residential mortgage and $47

million of unallocated ALLL was allocated to the loan portfolio segments.

106

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.