BB&T 2014 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

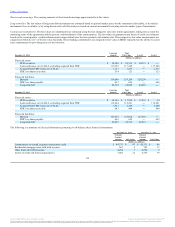

The allocated provision for loan and lease losses is also allocated to the relevant segments based on management’s assessment of the segments’ credit risks.

The allocated provision is designed to achieve a high degree of correlation between the loan loss experience and the GAAP basis provision at the segment

level, while at the same time providing management with a measure of operating performance that gives appropriate consideration to the risks inherent in

each of the Company’s operating segments. Any over or under allocated provision for loan and lease losses is reflected in Other, Treasury and Corporate to

arrive at consolidated results.

BB&T allocates expenses to the reportable segments based on various methodologies, including volume and amount of loans and deposits and the number of

full-time equivalent employees. Allocation systems are refined from time to time along with further identification of certain cost pools. These cost pools and

refinements are implemented to provide for improved managerial reporting of cost to the appropriate business segments. A portion of corporate overhead

expense is not allocated, but is retained in corporate accounts and reflected as Other, Treasury and Corporate in the accompanying tables. The majority of

depreciation expense is recorded in support units and allocated to the segments as part of allocated corporate expense. Income taxes are allocated to the

various segments based on taxable income and statutory rates applicable to the segment.

Community Banking

Community Banking serves individual and business clients by offering a variety of loan and deposit products and other financial services. Community

Banking is primarily responsible for serving client relationships and, therefore, is credited with certain revenue from the Residential Mortgage Banking,

Financial Services, Insurance Services, Specialized Lending, and other segments, which is reflected in net referral fees.

Residential Mortgage Banking

Residential Mortgage Banking retains and services mortgage loans originated by Community Banking as well as those purchased from various

correspondent originators. Mortgage loan products include fixed and adjustable rate government and conventional loans for the purpose of constructing,

purchasing or refinancing residential properties. Substantially all of the properties are owner occupied. BB&T generally retains the servicing rights to loans

sold. Residential Mortgage Banking earns interest on loans held in the warehouse and portfolio, earns fee income from the origination and servicing of

mortgage loans and recognizes gains or losses from the sale of mortgage loans.

Dealer Financial Services

Dealer Financial Services originates loans to consumers on a prime and nonprime basis for the purchase of automobiles. Such loans are originated on an

indirect basis through approved franchised and independent automobile dealers throughout the BB&T market area and nationally through Regional

Acceptance Corporation. This segment also originates loans for the purchase of boats and recreational vehicles originated through dealers in BB&T’s market

area. In addition, financing and servicing to dealers for their inventories is provided through a joint relationship between Dealer Financial Services and

Community Banking.

Specialized Lending

BB&T's Specialized Lending consists of LOBs and subsidiaries that provide specialty finance products to consumers and businesses. The LOBs include

Commercial Finance and Governmental Finance. Commercial Finance structures and manages asset-based working capital financing, supply chain financing,

export-import finance, accounts receivable management and credit enhancement. Commercial Finance also contains the Mortgage Warehouse Lending

business, which provides short-term lending solutions to finance first-lien residential mortgage LHFS by independent mortgage companies. Governmental

Finance provides tax-exempt financing to meet the capital project needs of local governments. Operating subsidiaries include BB&T Equipment Finance,

which provides equipment leasing largely within BB&T’s banking footprint; Sheffield Financial, a dealer-based financer of equipment for both small

businesses and consumers; Prime Rate Premium Finance Corporation, which includes AFCO and CAFO, insurance premium finance LOBs that provide

funding to businesses in the United States and Canada and to consumers in certain markets within BB&T’s banking footprint; and Grandbridge, a full-service

commercial mortgage banking lender providing loans on a national basis. Lendmark Financial Services, a direct consumer finance lending company, was

sold during the fourth quarter of 2013, resulting in the sale of $500 million of loans and the transfer of $230 million of loans to Residential Mortgage

Banking. Branch Bank clients as well as nonbank clients within and outside BB&T’s primary geographic market area are served by these LOBs. The

Community Banking segment receives credit for referrals to these LOBs with the corresponding charge retained as part of Other, Treasury and Corporate in

the accompanying tables.

145

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.