BB&T 2014 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

Other securities: These securities consist primarily of mutual funds and corporate bonds. These securities are valued based on a review of quoted market

prices for assets as well as through the various other inputs discussed previously.

Acquired from FDIC securities: Securities acquired from the FDIC consist of re-remic non-agency MBS, municipal securities and non-agency MBS. State and

political subdivision securities and certain non-agency MBS acquired from the FDIC are valued in a manner similar to the approach described above for

those asset classes. The re-remic non-agency MBS, which are categorized as Level 3, are valued based on broker dealer quotes that reflected certain

unobservable market inputs.

LHFS: Certain mortgage loans are originated to be sold to investors, which are carried at fair value. The fair value is primarily based on quoted market prices

for securities backed by similar types of loans. The changes in fair value of these assets are largely driven by changes in interest rates subsequent to loan

funding and changes in the fair value of servicing associated with the mortgage LHFS.

Residential MSRs: Residential MSRs are valued using an OAS valuation model to project cash flows over multiple interest rate scenarios, which are then

discounted at risk-adjusted rates. The model considers portfolio characteristics, contractually specified servicing fees, prepayment assumptions, delinquency

rates, late charges, other ancillary revenue, costs to service and other economic factors. Fair value estimates and assumptions are compared to industry

surveys, recent market activity, actual portfolio experience and, when available, other observable market data.

Derivative assets and liabilities: The fair values of derivatives are determined based on quoted market prices and internal pricing models that are primarily

sensitive to market observable data. The fair values of interest rate lock commitments, which are related to mortgage loan commitments and are categorized as

Level 3, are based on quoted market prices adjusted for commitments that are not expected to fund and include the value attributable to the net servicing

fees.

Private equity and similar investments: Private equity and similar investments are measured at fair value based on the investment’s net asset value. In many

cases there are no observable market values for these investments and therefore management must estimate the fair value based on a comparison of the

operating performance of the company to multiples in the marketplace for similar entities. This analysis requires significant judgment, and actual values in a

sale could differ materially from those estimated.

Short-term borrowings: Short-term borrowings represent debt securities sold short that are entered into as a hedging strategy for the purposes of supporting

institutional and retail client trading activities.

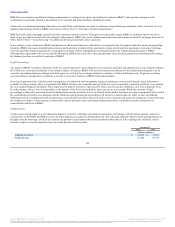

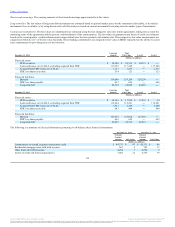

The following tables present activity for financial assets and liabilities that are valued using Level 3 inputs:

Balance at January 1, 2014 $ 861 $ 1,047 $ (11) $ 291

Total realized and unrealized gains (losses):

Included in earnings:

Interest income 33 ― ― ―

Mortgage banking income ― (221) 94 ―

Other noninterest income ― ― (2) 27

Included in unrealized net holding gains (losses) in OCI (38) ― ― ―

Purchases ― ― ― 67

Issuances ― 141 75 ―

Sales ― ― ― (50)

Settlements (111) (123) (139) (7)

Transfers into Level 3 ― ― ― 1

Balance at December 31, 2014 $ 745 $ 844 $ 17 $ 329

Change in unrealized gains (losses) included in earnings for the period,

attributable to assets and liabilities still held at December 31, 2014 $ 33 $ (221) $ 17 $ 15

136

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.