BB&T 2014 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

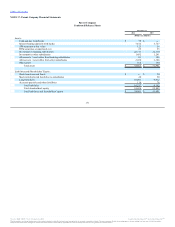

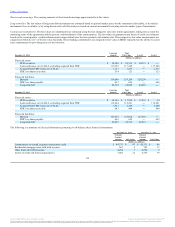

Assets:

Trading securities $ 381 $ 256 $ 125 $ ―

AFS securities:

U.S. Treasury 595 ― 595 ―

MBS issued by GSE 17,929 ― 17,929 ―

States and political subdivisions 1,851 ― 1,851 ―

Non-agency MBS 291 ― 291 ―

Other 45 10 35 ―

Acquired from FDIC 1,393 ― 532 861

LHFS 1,222 ― 1,222 ―

Residential MSRs 1,047 ― ― 1,047

Derivative assets:

Interest rate contracts 862 ― 859 3

Foreign exchange contracts 2 ― 2 ―

Private equity and similar investments 291 ― ― 291

Total assets $ 25,909 $ 266 $ 23,441 $ 2,202

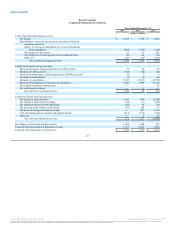

Liabilities:

Derivative liabilities:

Interest rate contracts $ 967 $ ― $ 953 $ 14

Foreign exchange contracts 3 ― 3 ―

Short-term borrowings 84 ― 84 ―

Total liabilities $ 1,054 $ ― $ 1,040 $ 14

The following discussion focuses on the valuation techniques and significant inputs for Level 2 and Level 3 assets and liabilities.

A third-party pricing service is generally utilized in determining the fair value of the securities portfolio. Management independently evaluates the fair

values provided by the pricing service through comparisons to other third party pricing sources, review of additional information provided by the third party

pricing service and other third party sources for selected securities and back-testing to compare the price realized on any security sales to the daily pricing

information received from the pricing service. Fair value measurements are derived from market-based pricing matrices that were developed using observable

inputs that include benchmark yields, benchmark securities, reported trades, offers, bids, issuer spreads and broker quotes. As described by security type

below, additional inputs may be used, or some inputs may not be applicable. In the event that market observable data was not available, which would

generally occur due to the lack of an active market for a given security, the valuation of the security would be subjective and may involve substantial

judgment by management.

Trading securities: Trading securities include various types of debt and equity securities, primarily consisting of debt securities issued by the U.S. Treasury,

GSEs, or states and political subdivisions. The valuation techniques used for these investments are more fully discussed below.

U.S. Treasury securities: Treasury securities are valued using quoted prices in active over the counter markets.

GSE securities and MBS issued by GSE: GSE pass-through securities are valued using market-based pricing matrices that are based on observable inputs

including benchmark TBA security pricing and yield curves that were estimated based on U.S. Treasury yields and certain floating rate indices. The pricing

matrices for these securities may also give consideration to pool-specific data supplied directly by the GSE. GSE CMOs are valued using market-based

pricing matrices that are based on observable inputs including offers, bids, reported trades, dealer quotes and market research reports, the characteristics of a

specific tranche, market convention prepayment speeds and benchmark yield curves as described above.

States and political subdivisions: These securities are valued using market-based pricing matrices that are based on observable inputs including MSRB

reported trades, issuer spreads, material event notices and benchmark yield curves.

Non-agency MBS: Pricing matrices for these securities are based on observable inputs including offers, bids, reported trades, dealer quotes and market

research reports, the characteristics of a specific tranche, market convention prepayment speeds and benchmark yield curves as described above.

135

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.