BB&T 2014 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2014 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Table of Contents

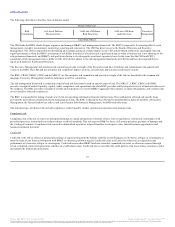

The following table shows the effect that the indicated changes in interest rates would have on net interest income as projected for the next twelve months

assuming a gradual change in interest rates as described below. Key assumptions in the preparation of the table include prepayment speeds of mortgage-

related and other assets, cash flows and maturities of derivative financial instruments, loan volumes and pricing, deposit sensitivity, customer preferences and

capital plans. The resulting change in net interest income reflects the level of interest rate sensitivity that income has in relation to the investment, loan and

deposit portfolios.

Up 200 bps 5.25 % 5.25 % 2.06 % 2.27 %

Up 100 4.25 4.25 1.46 1.35

No Change 3.25 3.25 ― ―

Down 25 3.00 3.00 0.33 0.39

The MRLCC has established parameters related to interest sensitivity that prescribe a maximum negative impact on net interest income under different

interest rate scenarios. In the event the results of the Simulation model fall outside the established parameters, management will make recommendations to

the MRLCC on the most appropriate response given the current economic forecast. The following parameters and interest rate scenarios are considered

BB&T’s primary measures of interest rate risk:

·Maximum negative impact on net interest income of 2% for the next 12 months assuming a linear change in interest rates totaling 100 basis points

over four months followed by a flat interest rate scenario for the remaining eight month period.

·Maximum negative impact on net interest income of 4% for the next 12 months assuming a linear change of 200 basis points over eight months

followed by a flat interest rate scenario for the remaining four month period.

If a rate change of 200 basis points cannot be modeled due to a low level of rates, a proportional limit applies. Management currently only models a negative

25 basis point decline because larger declines would have resulted in a Federal funds rate of less than zero. In a situation such as this, the maximum negative

impact on net interest income is adjusted on a proportional basis. Regardless of the proportional limit, the negative risk exposure limit will be the greater of

1% or the proportional limit.

Management has also established a maximum negative impact on net interest income of 4% for an immediate 100 basis points change in rates and 8% for an

immediate 200 basis points change in rates. These “interest rate shock” limits are designed to create an outer band of acceptable risk based upon a significant

and immediate change in rates.

Management must also consider how the balance sheet and interest rate risk position could be impacted by changes in balance sheet mix. Liquidity in the

banking industry has been very strong during the current economic cycle. Much of this liquidity increase has been due to a significant increase in

noninterest-bearing demand deposits. Consistent with the industry, Branch Bank has seen a significant increase in this funding source. The behavior of these

deposits is one of the most important assumptions used in determining the interest rate risk position of BB&T. A loss of these deposits in the future would

reduce the asset sensitivity of BB&T’s balance sheet as the Company increases interest-bearing funds to offset the loss of this advantageous funding source.

Beta represents the correlation between overall market interest rates and the rates paid by BB&T on interest-bearing deposits. BB&T applies an average beta

of approximately 80% to its managed rate deposits for determining its interest rate sensitivity. Managed rate deposits are high beta, premium money market

and interest checking accounts, which attract significant client funds when needed to support balance sheet growth. BB&T regularly conducts sensitivity on

other key variables to determine the impact they could have on the interest rate risk position. This allows BB&T to evaluate the likely impact on its balance

sheet management strategies due to a more extreme variation in a key assumption than expected.

The following table shows the effect that the loss of demand deposits and an associated increase in managed rate deposits would have on BB&T’s interest-

rate sensitivity position. For purposes of this analysis, BB&T modeled the incremental beta for the replacement of the lost demand deposits at 100%.

73

Source: BB&T CORP, 10-K, February 25, 2015 Powered by Morningstar® Document Research℠

The information contained herein may not be copied, adapted or distributed and is not warranted to be accurate, complete or timely. The user assumes all risks for any damages or losses arising from any use of this information,

except to the extent such damages or losses cannot be limited or excluded by applicable law. Past financial performance is no guarantee of future results.