Yahoo 2009 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2009 Yahoo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

|

|

on the date of grant based on the implied volatility of publicly traded options on our common stock, with a term

of one year or greater. We believe that implied volatility calculated based on actively traded options on our

common stock is a better indicator of expected volatility and future stock price trends than historical volatility.

Therefore, expected volatility for the year ended December 31, 2009 was based on a market-based implied

volatility. The assumptions used in calculating the fair value of stock-based awards represent our best estimates,

but these estimates involve inherent uncertainties and the application of management judgment. As a result, if

factors change and we use different assumptions, our stock-based compensation expense could be materially

different in the future. In addition, we are required to estimate the expected pre-vesting award forfeiture rate, as

well as the probability that performance conditions that affect the vesting of certain awards will be achieved, and

only recognize expense for those shares expected to vest. We estimate this forfeiture rate based on historical

experience of our stock-based awards that are granted and cancelled. If our actual forfeiture rate is materially

different from our original estimates, the stock-based compensation expense could be significantly different from

what we have recorded in the current period. Changes in the estimated forfeiture rate can have a significant effect

on reported stock-based compensation expense, as the effect of adjusting the forfeiture rate for all current and

previously recognized expense for unvested awards is recognized in the period the forfeiture estimate is changed.

In addition, because many of our stock-based awards have vesting schedules of two or three years cliff vests, a

significant change in our actual or expected forfeiture experience will result in the reversal of stock-based

compensation which was recorded in prior years for all unvested awards. If the actual forfeiture rate is higher

than the estimated forfeiture rate, then an adjustment will be made to increase the estimated forfeiture rate, which

will result in a decrease to the expense recognized in the consolidated financial statements. If the actual forfeiture

rate is lower than the estimated forfeiture rate, then an adjustment will be made to lower the estimated forfeiture

rate, which will result in an increase to the expense recognized in the consolidated financial statements. See

Note 12—“Employee Benefits” in the Notes to the consolidated financial statements for additional information.

Recent Accounting Pronouncements

See Note 1—“The Company and Summary of Significant Accounting Policies” in the Notes to the consolidated

financial statements.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

We are exposed to the impact of interest rate changes, foreign currency exchange rate fluctuations, and changes

in the market values of our investments.

Interest Rate Risk. Our exposure to market risk for changes in interest rates relates primarily to our cash and

marketable debt securities portfolio. We invest excess cash in money market funds, time deposits, and liquid debt

instruments of the U.S. and foreign governments and their agencies, U.S. municipalities, and high-credit

corporate issuers which are classified as marketable debt securities and cash equivalents.

Investments in fixed rate and floating rate interest earning instruments carry a degree of interest rate risk. Fixed

rate securities may have their fair market value adversely impacted due to a rise in interest rates, while floating

rate securities may produce less income than expected if interest rates fall. Due in part to these factors, our future

investment income may fall short of expectations due to changes in interest rates or we may suffer losses in

principal if forced to sell securities that have declined in market value due to changes in interest rates. As of

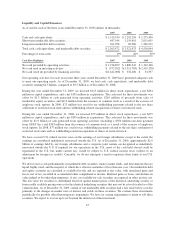

December 31, 2009 and 2008, we had investments in short-term marketable debt securities of approximately $2.0

billion and $1.2 billion, respectively. Such investments had a weighted-average yield of less than 1.0 percent and

1.2 percent, respectively. As of December 31, 2009 and 2008, we had investments in long-term marketable debt

securities of approximately $1.2 billion and $70 million, respectively. Such investments had a weighted average

yield of approximately 1.0 percent and 4.0 percent, respectively. A hypothetical 100 basis point increase in

interest rates would result in an approximate $25 million and $2 million decrease in the fair value of our

available-for-sale debt securities as of December 31, 2009 and 2008, respectively.

54