APC 2007 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2007 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

|

|

Companies acquired or sold during the year are included

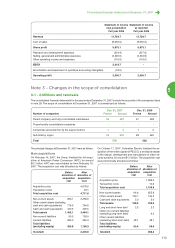

in or removed from the consolidated financial statements

as of the date when effective control is acquired or relin-

quished.

Intragroup balances and transactions are eliminated in

consolidation.

The list of consolidated subsidiaries and associates is pro-

vided in note 29.

Group consolidation is based on closing figures as of De-

cember 31 of the period.

1.5 - Business combinations

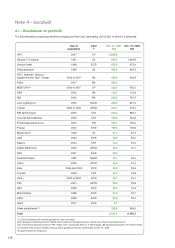

Business combinations are accounted for using the pur-

chase method, in accordance with IFRS 3 –

Business

Combinations

. In accordance with the option provided by

IFRS 1 –

First-Time Adoption of IFRS

– business combi-

nations recorded before January 1, 2004 have not been

restated.

All identified acquired assets, liabilities and contingent lia-

bilities are recognized at their fair value as of the date of ac-

quisition. Provisional fair values are adjusted within a

maximum of twelve months following the date of acquisi-

tion.

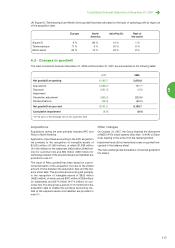

If the cost of acquisition is higher than the fair value of as-

sets acquired and liabilities assumed at the date of acqui-

sition, the excess is recorded under goodwill. If the cost of

acquisition is lower than the fair value of assets acquired

and liabilities assumed at the date of acquisition, the neg-

ative goodwill is immediately recognized in the income

statement.

Goodwill is not amortized, but tested for impairment at

least annually and when there is an indication that it may

be impaired (note 1.10). Any impairment losses are rec-

ognized under "Other operating income/(expense)".

1.6 - Translation of the financial

statements of foreign subsidiaries

The consolidated financial statements are drawn up in

euros.

The financial statements of subsidiaries that use another

functional currency are translated into euros as follows:

Assets and liabilities are translated at official year-end

exchange rates.

Income statement and cash flow items are translated at

weighted-average annual exchange rates.

Differences arising on translation are recorded in equity

under "Translation reserve". In accordance with IFRS 1 –

First Time Adoption of IFRS

– cumulative translation ad-

justments were reset to zero at January 1, 2004 by ad-

justing opening retained earnings, without any impact on

total equity.

1.7 - Foreign currency transactions

Foreign currency transactions are recorded using the offi-

cial exchange rate in effect at the date the transaction is

recorded or the hedging rate. At year-end, foreign currency

payables and receivables are translated into the reporting

currency at year-end exchange rates or the hedging rate.

Gains or losses on foreign currency conversion are

recorded in the income statement under "Other financial

income and expense, net". Foreign currency hedging is de-

scribed below, in note 1.22.

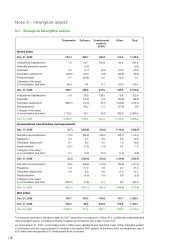

1.8 - Intangible assets

Intangible assets acquired separately or as

part of a business combination

Intangible assets acquired separately are initially recog-

nized in the balance sheet at historical cost. They are sub-

sequently measured using the cost model, in accordance

with IAS 38 –

Intangible Assets

.

Trademarks, customer lists and other identifiable assets of

acquired companies are recognized in the balance sheet

at fair value, determined by qualified experts for the most

significant assets and internally for the rest. The valuations

are performed using generally accepted methods, based

on expected future cash flows. The assets are regularly

tested for impairment.

Intangible assets other than trademarks are amortized on

a straight-line basis over their useful life or the period of

legal protection. Amortized intangible assets are tested for

impairment when there is any indication that their recover-

able amount may be less than their carrying amount.

Amortization and impairment losses on intangible assets

recognized on business combinations are presented under

"Amortization and impairment of purchase accounting in-

tangibles" in the income statement.

Impairment losses on other intangible assets are recog-

nized under "Other operating income/(expense)".

Trademarks

Trademarks acquired as part of a business combination

are not amortized when they are considered to have an in-

definite life.

This is determined on the basis of:

Brand awareness.

The Group’s strategy for integrating the trademark into its

existing portfolio.

Non-amortized trademarks are tested for impairment at

least annually and when there is any indication that their

recoverable amount may be less than their carrying

amount. When necessary, an impairment loss is recorded.

Internally-generated intangible assets

Research and development costs

Research costs are recognized in the income statement

when incurred.

Systems were set up to track and capitalize development

costs in 2004. As a result, only development costs for new

products launched since 2004 are capitalized in the IFRS

accounts.

Development costs for new projects are capitalized if, and

only if:

The project is clearly identified and the related costs are

separately identified and reliably tracked.

The project’s technical feasibility has been demon-

strated and the Group has the intention and financial re-

sources to complete the project and to use or sell the

related products.

It is probable that the future economic benefits attribut-

able to the project will flow to the Group.

Development costs that do not meet these criteria are ex-

pensed in the year in which they are incurred.

Capitalized development costs are amortized over the es-

timated life of the underlying technology, which generally

108