APC 2007 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2007 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

|

|

5

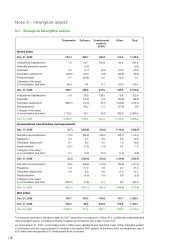

Consolidated financial statements at December 31, 2007

ranges from 3 to 10 years. The amortization charge is in-

cluded in the cost of the related products and classified

into “Cost of sales” when the products are sold.

Software implementation

External and internal costs for the programming, coding

and testing of Enterprise Resource Planning (ERP) appli-

cations are capitalized and amortized over the applications’

useful lives.

1.9 - Property, plant and equipment

Land, buildings, plant and equipment are carried at cost,

less accumulated depreciation and any accumulated im-

pairment losses, in accordance with the cost model pro-

vided for in IAS 16 –

Property, plant and equipment

.

Each part of an item of property, plant and equipment with

a useful life that is different from that of the item as a whole

is depreciated separately on a straight-line basis. The main

useful lives are as follows:

The useful life of operating assets, such as production

lines, reflects the related products’ estimated life cycles.

Useful lives are reviewed periodically and may be adjusted

prospectively if appropriate.

The depreciable amount of an asset is determined after

deducting its residual value, when the residual value is ma-

terial.

Depreciation is charged to the income statement or in-

cluded in the production cost of inventory or the cost of in-

ternally-generated intangible assets. It is recognized under

"Cost of sales", "Research expenses" or “Selling, general

and administrative expenses”, depending on the case.

Property, plant and equipment are tested for impairment

when there is any indication that their recoverable amount

may be less than their carrying amount. Impairment losses

are charged to the income statement under “Other operat-

ing income/(expense)”.

Leases

Finance leases, defined as leases that transfer substan-

tially all the risks and rewards of ownership to the lessee,

are recognized as an asset and a liability.

Leases that do not transfer substantially all the risks and

rewards of ownership are classified as operating leases

and the related payments are recognized as an expense

on a straight-line basis over the lease term.

Borrowing costs

Borrowing costs incurred during the construction or acqui-

sition of property, plant and equipment and intangible as-

sets are expensed when incurred, in accordance with the

recommended treatment under IAS 23 –

Borrowing Costs

.

1.10 - Impairment of assets

In accordance with IAS 36 –

Impairment of Assets

– the re-

coverable amount of long-lived assets is assessed as fol-

lows:

All depreciable and amortizable property, plant and

equipment and intangible assets are reviewed at each bal-

ance sheet date to determine whether there is any indica-

tion that the asset may be impaired. Indications of impair-

ment are identified on the basis of external or internal

information. If such an indication exists, the Group tests

the asset for impairment by comparing its carrying amount

to the higher of fair value less costs to sell and value in

use.

Non-amortizable intangible assets and goodwill are

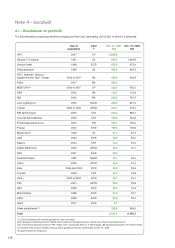

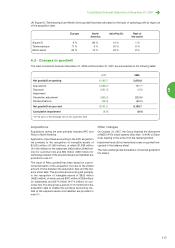

tested for impairment at least annually and when there is

any indication that the asset may be impaired.

Value in use is determined by discounting estimated future

cash flows that will be generated by the tested assets, gen-

erally over a period of not more than five years. Estimated

future cash flows are based on management’s economic

assumptions and operating forecasts. The discount rate

corresponds to Schneider Electric’s weighted average cost

of capital (7.5% at December 31, 2007 and 2006), plus a

risk premium depending on the region in question.

Impairment tests are performed at the level of the cash-

generating unit (CGU) to which the asset belongs. A cash-

generating unit is the smallest group of assets that

generates cash inflows that are largely independent of

those cash flows from other assets or groups of assets. At

Schneider Electric, CGUs generally correspond to the Op-

erating Divisions (Europe, North America, Asia-Pacific and

Rest of the World). Each of the Growth Platform busi-

nesses is also a CGU.

Goodwill is allocated to a CGU when initially recognized.

This allocation is made on the basis used to track the per-

formance of Group operations and to assess the benefits

derived from the synergies of the business combination.

If the recoverable amount of an asset or CGU is lower than

its carrying amount, an impairment loss is recognized. To

the extent possible, impairment losses on CGUs compris-

ing goodwill are recorded as a deduction from goodwill.

The majority of the Group’s goodwill is allocated to CGUs

in Europe and the United States. This goodwill is tested for

impairment using a discount rate equal to the Group’s

weighted average cost of capital, with no risk premium. The

perpetutity growth rate for these CGUs was 2% in 2007,

unchanged from the previous year.

1.11 - Non-current financial assets

Investments in non-consolidated companies are classified

in available-for-sale financial assets. They are initially

recorded at cost and subsequently measured at fair value,

when fair value can be reliably determined.

The fair value of equity instruments quoted in an active

market corresponds to the quoted price on the balance

sheet date.

In cases where fair value can not be reliably determined,

the instruments are measured at cost net of any accumu-

lated impairment losses. The recoverable amount is deter-

mined by reference to the Group’s equity in the underlying

entity’s net assets and the entity’s expected future prof-

itability and business outlook. This rule is applied in partic-

ular to equity instruments that do not have a quoted market

price in an active market.

Changes in fair value are accumulated in equity under

"Other reserves” up to the date of sale, at which time they

are recognized in the income statement. Unrealized losses

on assets that are considered to be permanently impaired

are recorded under "Finance costs and other financial in-

come and expense, net".

Buildings : 20-40 years

Plant and equipment : 3-10 years

Other : 3-12 years

109