APC 2010 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2010 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

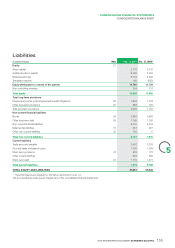

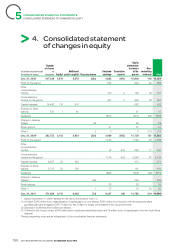

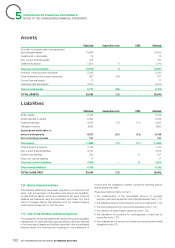

CONSOLIDATED FINANCIAL STATEMENTS

5NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

Note1

Accounting Policies

1.1 - Accounting standards

The consolidated financial statements have been prepared in

compliance with the international accounting standards (IFRS) as

adopted by the European Union as of December31, 2010. The

same accounting methods were used as for the consolidated

fi nancial statements for the year ended December31, 2009, with

the exception, notably, of the fi rst application of the revised IFRS3

- Business Combinations and revised IAS27 – Consolidated and

Seperate Financial Statements norms

IAS27 (revised) presents the consolidated fi nancial statements of a

group as those of a single economic entity with two categories of

owners: fi rstly the equity holders of the parent (Schneider Electric

SA shareholders) and secondly non-controlling interests (minority

shareholders in the subsidiaries). A non-controlling interest is defi ned

as the equity in a subsidiary not attributable, directly or indirectly, to

a parent (hereinafter “minority interests”). Under this new approach,

changes in a parent’s ownership interest in a subsidiary not resulting

in a loss of control are accounted for as equity transactions since

there is no change in control within the economic entity. Thus, from

January1, 2010, when increasing its interest in a consolidated

subsidiary, the Group recognises the difference between the

acquisition cost and the book value of the minority interests as a

change in equity attributable to the shareholders of Schneider Electric

SA. Conversely, the Group recognises any gains or losses generated

on share sales resulting in a loss of control of the subsidiary in the

statement of income.

IFRS3 (revised) introduced a series of changes to the acquisition

method as defi ned in IFRS3 prior to the revision, notably including:

•the option to measure the minority interests in the acquiree either

as their proportionate interest in the identifi able net assets of the

acquiree or at fair value. This option is available on a case by case

basis for each acquisition;

•the recognition of any adjustment to the purchase price at fair

value from the acquisition date;

•the recognition as an expense for the period of costs directly

associated with the acquisition;

•in the case of a business combination achieved in stages (step

acquisition), the fair value measurement on the acquisition date of

the interest previously held in the acquiree and the recognition of

any resulting gain or loss in the statement of income.

The impact on the statement of income of the application of IFRS3

(revised) and IAS27 (revised) is recognised under other operating

income/(expense). EUR31million in acquisition-related costs were

recognised in the statement of income in 2010.

The main areas of impact of the adoption of IFRS3 (revised) and

IAS27 (revised) on Schneider Electric’s consolidated financial

statements as of December31, 2010 were as follows:

•the treatment of the sale of shares in Schneider Electric South

Africa without a loss of control, recognised in equity and thus

not resulting in any gain on disposal being recognised in the

statement of income;

•the restatement in the 2009 comparative statement of income

of the EUR25.8million in acquisition costs incurred in 2009 on

deals concluded in 2010; these costs were previously capitalised

whereas they must be recognised as an expense for the period

under the new standard (see below: reconciliation between the

published 2009 statement of income and balance sheet as of

December 31, 2009 and those presented for comparative

purposes).

The following standards and interpretations that were applicable

during the period did not have a material impact on the consolidated

fi nancial statements as of December31, 2010:

•amendment to IFRS 1 – First-time Adoption of International

Financial Reporting Standards;

•amendment to IFRS 2 – Share-based Payment (Group cash-

settled share-based payment transactions);

•amendement of IAS39 – Financial instruments: Recognition and

Measurement – Exposures Qualifying for Hedge Accounting;

•IFRS improvements (May2008): amendment to IFRS5;

•IFRS improvements (April2009);

•IFRIC12 – Service Concession Arrangements;

•IFRIC15 – Agreements for the Construction of Real Estate;

•IFRIC16 – Hedges of a Net Investment in a Foreign Operation;

•IFRIC17 – Distributions of Non-cash Assets to Owners;

•IFRIC18 – Transfers of Assets from Customers.

There are no differences in practice between the standards applied

by Schneider Electric as of December31, 2010 and the IFRSs issued

by the International Accounting Standards Board (IASB), since the

application of standards and interpretations that are mandatory for

reporting periods beginning on or after January1, 2010 but not yet

adopted by the European Union would not have a material impact.

Lastly, the Group did not apply the following standards and

interpretations that had not yet been adopted by the European

Union as of December31, 2010 or that are mandatory at some

point subsequent to December31, 2010:

•standards adopted:

–IAS24 – Related party disclosures,

–amendment to IAS32 – Classifi cation of rights issues,

–amendment to IFRIC14 – Prepayments of a Minimum Funding

Requirement,

–IFRIC 19 - Extinguishing Financial Liabilities with Equity

Instruments;

•standards not yet adopted:

–improvements to IFRSs (May2010),

–IFRS9 - Financial Instruments,

–amendment to IFRS7 – Disclosures – Transfers of fi nancial

assets,

–amendments to IFRS1 – Severe Hyperinfl ation and Removal

of Fixed Dates for First-time Adopters,

–amendments to IAS12 – Deferred Tax: Recovery of Underlying

Assets.

Schneider Electric is currently assessing their potential impact on

the Group’s consolidated financial statements. At this stage of

analysis, the Group does not expect the impact on its consolidated

fi nancial statements to be material, except for IFRS9 for which an

impact analysis has not yet begun, due to its incomplete nature and

uncertainties surrounding the adoption process in Europe.

The fi nancial statements provide data prepared in accordance with

IFRS for the years ended December31, 2010 and December31,

2009. The fi nancial statements for the year ended December31,

2008, presented in the Registration Document registered with

Autorité des Marchés Financiers (AMF) under number D 09-0124

on March17, 2009, are incorporated by reference.

2010 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC158