APC 2010 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2010 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

|

|

CONSOLIDATED FINANCIAL STATEMENTS

5

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

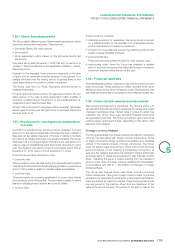

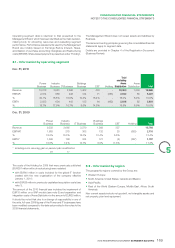

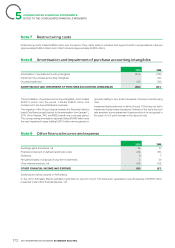

1.11 - Impairment of assets

In accordance with IAS36 – Impairment of Assets – the Group

assesses the recoverable amount of its long-lived assets as follows:

•for all property, plant and equipment subject to depreciation and

intangible assets subject to amortisation, the Group carries out a

review at each balance sheet date to assess whether there is any

indication that they may be impaired. Indications of impairment

are identifi ed on the basis of external or internal information. If

such an indication exists, the Group tests the asset for impairment

by comparing its carrying amount to the higher of fair value minus

costs to sell and value in use;

•non-amortisable intangible assets and goodwill are tested for

impairment at least annually and whenever there is an indication

that the asset may be impaired.

Value in use is determined by discounting future cash fl ows that will

be generated by the tested assets, generally over a period of not

more than fi ve years. These future cash fl ows are based on Group

management’s economic assumptions and operating forecasts. The

discount rate corresponds to the Group’s weighted average cost

of capital (WACC) at the measurement date plus a risk premium

depending on the region in question. The WACC stood at 8.4% at

December31, 2010, a slight increase on the 8.1% at December31,

2009. This rate is based on (i) a long-term interest rate of 3.8%,

corresponding to the average interest rate for 10year OAT treasury

bonds over the past few years, (ii) the average premium applied to

fi nancing obtained by the Group in the fourth quarter of 2010, and

(iii) the weighted country risk premium for the Group’s businesses in

the countries in question.

The perpetuity growth rate was 2%, unchanged on the previous

fi nancial year.

Impairment tests are performed at the level of the cash-generating

unit (CGU) to which the asset belongs. A cash-generating unit is the

smallest group of assets that generates cash infl ows that are largely

independent of the cash fl ows from other assets or groups of assets.

The cash-generating units correspond to the Power, Industry, IT,

Buildings, CST businesses, which have operated as divisions since

the reorganisation on January1, 2010. Entities were reallocated to

the new CGUs at the lowest possible level on the basis of their

business activities; in the case of mixed entities, their assets were

allocated to each business (Power and Industry mainly) pro-rata to

their revenue in that business.

At end-2010, the Distribution business acquired from Areva on

June7, 2010 wasn’t allocated to any specifi c CGU and hadn’t yet

been tested given the recent date of acquisition. Nevertheless, as

2010 results were slightly ahead of the forecasts in the business plan

used for the purposes of the acquisition, the Group does not feel

there that there are impairment risks with respect to these assets at

the balance sheet date.

The WACC used to determine the value in use of each CGU was

9.0% for Power and Industry, 9.2% for IT, 8.6% for Buildings and

CST.

Goodwill is allocated when initially recognised. The CGU allocation is

done on the same basis as used by Group management to monitor

operations and assess synergies deriving from acquisitions. As a

result of the organisational changes effective January1, 2010, the

allocation of goodwill has been changed to refl ect the new operating

segments defi ned in accordance with the newly issued IFRS8. This

modifi cation did not have an impact on asset impairment.

Where the recoverable amount of an asset or CGU is lower than

its book value, an impairment loss is recognised. Where the tested

CGU comprises goodwill, any impairment losses are fi rstly deducted

therefrom.

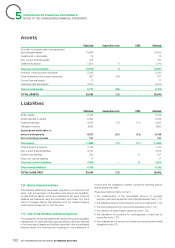

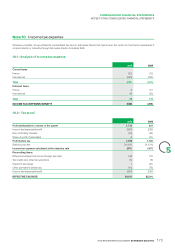

1.12 - Non-current financial assets

Investments in non-consolidated companies are classified as

available-for-sale fi nancial assets. They are initially recorded their

cost of acquisition and subsequently measured at fair value, when

fair value can be reliably determined.

The fair value of equity instruments quoted in an active market may

be determined reliably and corresponds to the quoted price on the

balance sheet date (Level 1 input as described in the amendment to

IFRS7 – Improving Disclosures about Financial Instruments).

In cases where fair value cannot be reliably determined (Level 3

inputs), the equity instruments are measured at net cost of any

accumulated impairment losses. The recoverable amount is

determined with reference to the Group’s share in the entity’s net

assets along with its expected future profi tability and outlook. This

rule is applied in particular to unlisted equity instruments.

Changes in fair value are accumulated in equity under “Other

reserves” up to the date of sale, at which time they are recognised

in the income statement. Unrealised losses on assets that are

considered to be permanently impaired are recorded under “Finance

costs and other fi nancial income and expense, net”.

Loans, recorded under “Other non-current fi nancial assets”, are

carried at amortised cost and tested for impairment where there

is an indication that they may have been impaired. Long-term

fi nancial receivables are discounted when the impact of discounting

is considered signifi cant.

1.13 - Inventories and work in process

Inventories and work in process are stated at the lower of their entry

cost (acquisition cost or production cost generally determined by the

weighted average price method) or of their estimated net realisable

value.

Net realisable value corresponds to the estimated selling price net of

remaining expenses to complete and/or sell the products.

Inventory impairment losses are recognised in “Cost of sales” for

the material component and in “Selling, general and administrative

expenses” for the fi nished products.

The cost of work in process, semi-fi nished and fi nished products,

includes the cost of materials and direct labor, subcontracting costs,

all production overheads based on normal capacity utilisation rates

and the portion of research and development costs related to the

production process (corresponding to the amortisation of capitalised

projects in production and product and range maintenance costs).

2010 REGISTRATION DOCUMENT SCHNEIDER ELECTRIC 163