Cabela's 2006 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

43

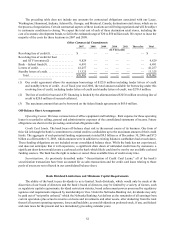

Delinquencies

We consider the entire balance of an account, including any accrued interest and fees, delinquent if the

minimum payment is not received by the payment due date. Our aging methodology is based on the number of

completed billing cycles during which a customer has failed to make a required payment. Delinquencies not only

have the potential to reduce earnings by increasing the unrealized loss recognized to reduce the loans to market

value and reducing securitization income, but they also result in additional operating costs dedicated to resolving the

delinquencies. The following chart shows the percentage of our managed loans that have been delinquent as of the

end of fiscal 2006, 2005 and 2004.

Fiscal Year

Number of days delinquent 2006 2005 2004

Greater than 30 days. . . . . . . . . . . . . . . . . . . . . 0.75% 0.67% 0.71%

Greater than 60 days. . . . . . . . . . . . . . . . . . . . . 0.44% 0.38% 0.41%

Greater than 90 days. . . . . . . . . . . . . . . . . . . . . 0.18% 0.16% 0.19%

Charge-offs

Gross charge-offs reflect the uncollectible principal, interest and fees on a customer’s account. Recoveries

reflect the amounts collected on previously charged-off accounts. Most bankcard issuers charge off accounts at 180

days. We charge off accounts on the 24th day of the month after an account becomes 115 days contractually delinquent,

except in the case of cardholder bankruptcies and cardholder deaths. Cardholder bankruptcies are charged off 30

days after notification, and delinquencies caused by cardholder deaths are charged off on the 24th day of the month

after an account is 60 days contractually delinquent. As a result, our charge-off rates are not directly comparable to

other participants in the bankcard industry. Our charge-off activity for the managed portfolio for fiscal years 2006,

2005 and 2004 is summarized below:

Fiscal Year

2006 2005 2004

(Dollars in Thousands)

Gross charge-offs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $31,068 $27,829 $23,134

Recoveries ............................................. 5,869 4,227 3,477

Net charge-offs ......................................... 25,199 23,602 19,657

Net charge-offs as a percentage of average managed loans . . . . . . . 1.86% 2.15% 2.21%

Liquidity and Capital Resources

Overview

Our merchandising business and our Financial Services segment have significantly different liquidity and capital

needs. The primary cash requirements of our merchandising business relate to capital for new destination retail stores,

purchases of economic development bonds related to the construction of new destination retail stores, purchases of

inventory, investments in our management information systems and other infrastructure, and other general working

capital needs. We historically have met these requirements by generating cash from our merchandising business

operations, borrowing under revolving credit facilities, issuing debt and equity securities, obtaining economic

development grants from state and local governments in connection with developing our destination retail stores,

collecting principal and interest payments on our economic development bonds and from the retirement of economic

development bonds. The cash flow we generate from our merchandising business is seasonal, with our peak cash

requirements for inventory occurring between May and November. While we have consistently generated overall

positive annual cash flow from our operating activities, other sources of liquidity are generally required by our

merchandising business during these peak cash use periods. These sources historically have included short-term