Cabela's 2006 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

69

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

Deferred income taxes are computed using the liability method under which deferred income taxes are provided

on the temporary differences between the tax bases of assets and liabilities and their financial reported amounts.

Stock-Based Compensation — Effective January 1, 2006, the Company adopted the provisions of FAS No.

123 (revised 2004), Share-Based Payment (“FAS 123R”), which requires the measurement and recognition of

compensation expense in the financial statements for all share-based payment awards to employees and directors

including employee stock option awards and employee stock purchases under an employee stock purchase plan.

The Company adopted FAS 123R using the modified prospective transition method, therefore, prior fiscal year

amounts were not restated. Under this method, in accordance with the provisions of FAS 123R, the Company is

recognizing compensation expense for (i) equity awards issued after January 1, 2006, based on grant date estimated

fair value on a straight-line basis over the requisite service period for the entire award, and (b) all awards granted

prior to, but not yet vested as of January 1, 2006, based on the grant date fair value estimated in accordance with

the original provisions of Accounting Principles Board (“APB”) Opinion No. 25, Accounting for Stock Issued to

Employees. The cumulative effect of the adoption of FAS 123R related to estimating forfeitures of outstanding

awards was not significant. In addition to the recognition of expense in the consolidated financial statements, FAS

123R also requires that the cash retained resulting from tax deductions in excess of the cumulative compensation cost

recognized for share-based arrangements be presented as a financing activity inflow in the consolidated statements

of cash flows on a prospective basis.

As a result of the adoption of FAS 123R, the Company’s consolidated net income for fiscal 2006 includes

compensation expense of $3,615 ($2,259 after-tax, or $.03 per diluted share). This share-based compensation expense

is recorded as a component of selling, general and administrative expenses in the consolidated statement of income.

For fiscal 2006, the excess tax benefit from stock option exercises totaling $495 is presented in financing activities

in the consolidated statement of cash flows.

Prior to January 1, 2006, as permitted by FAS 123, Accounting for Stock-Based Compensation (“FAS 123”),

the Company accounted for stock-based payments under the provisions of APB Opinion No. 25, Accounting for Stock

Issued to Employees and related interpretations. The Company also had adopted the disclosure-only provisions of

FAS 123, whereby the Company disclosed the pro forma net income and earnings per share as if the Company had

applied the fair value recognition provisions to its share-based payment awards.

See Note 14 for additional stock-based compensation disclosures under FAS 123R, stock option activity and

the assumptions used in determining the fair value of stock options.

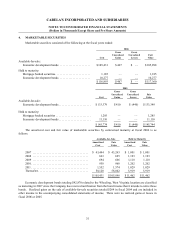

Financial Instruments and Credit Risk Concentrations — Financial instruments, which potentially subject

the Company to concentrations of credit risk, are primarily cash, investments and accounts receivable. The Company

invests primarily in money market accounts, tax-free municipal bonds or commercial paper with short-term maturities

and limits the amount of credit exposure to any one entity. Concentrations of credit risk with respect to accounts

receivable are limited due to the nature of the Company’s receivables.

Fair Value of Financial Instruments — The carrying amount of cash and cash equivalents, receivables, credit

card loans held for sale, retained interests in asset securitizations, accounts payable, short-term borrowings, notes

payable to banks and accrued expenses approximate fair value because of the short maturity of these instruments.

The fair values of each of the Company’s long-term debt instruments are based on the amount of future cash flows

associated with each instrument discounted using the Company’s current borrowing rate for similar debt instruments

of comparable maturity. The fair value estimates are made at a specific point in time and the underlying assumptions

are subject to change based on market conditions. At fiscal 2006 and 2005, the total carrying amount of the Company’s

long-term debt was $311,382 and $119,826, respectively, with an estimated fair value of approximately $315,979 and

$120,125, respectively. For purposes of estimating fair value, time deposits are pooled in homogeneous groups and

the future cash flows of those groups are discounted using current market rates offered for similar products. At fiscal

2006 and 2005, the carrying amounts of the Company’s time deposits were $102,196 and $109,488, respectively, with

estimated fair values of approximately $102,739 and $113,632, respectively.