Cabela's 2006 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

52

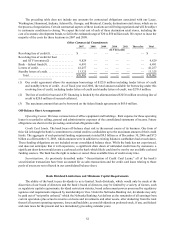

The preceding table does not include any amounts for contractual obligations associated with our Lacey,

Washington; Hammond, Indiana; Adairsville, Georgia; and Montreal, Canada; destination retail stores, which are in

the process of negotiations. Certain contractual aspects of these locations are still being negotiated and will be subject

to customary conditions to closing. We expect the total cost of each of these destination retail stores, including the

cost of economic development bonds, to fall in the estimated range of $30 to $50 million each. We expect to incur the

majority of the costs for these locations in 2007 and 2008.

Other Commercial Commitments

2007 2008 2009 2010 2011 Thereafter Total

(In Thousands)

Revolving line of credit(1). . . . . . . . . . . . . . . . $ — — — — — — $ —

Revolving line of credit for boat

and ATV inventory(2) . . . . . . . . . . . . . . . . 9,829 — — — — — 9,829

Bank – federal funds(3) . . . . . . . . . . . . . . . . . . 6,491 — — — — — 6,491

Letters of credit . . . . . . . . . . . . . . . . . . . . . . . . 41,257 — — — — — 41,257

Standby letters of credit. . . . . . . . . . . . . . . . . . 13,325 — — — — — 13,325

Total .............................. $70,902 — — — — — $70,902

(1) Our credit agreement allows for maximum borrowings of $325.0 million including lender letters of credit

and standby letters of credit. As of fiscal year end 2006, the total amount available for borrowing under this

revolving line of credit, including lender letters of credit and standby letters of credit, was $270.4 million.

(2) The line of credit for boat and ATV financing is limited by the aforementioned $325.0 million revolving line of

credit to $20.0 million of secured collateral.

(3) The maximum amount that can be borrowed on the federal funds agreements is $85.0 million.

Off-Balance Sheet Arrangements

Operating Leases. We lease various items of office equipment and buildings. Rent expense for these operating

leases is recorded in selling, general and administrative expenses of the consolidated statements of income. Future

obligations are shown in the preceding contractual obligations table.

Credit Card Limits. The bank bears off-balance sheet risk in the normal course of its business. One form of

this risk is through the bank’s commitment to extend credit to cardholders up to the maximum amount of their credit

limits. The aggregate of such potential funding requirements totaled $9.5 billion as of December 30, 2006 and $7.5

billion as of December 31, 2005, which amounts were in addition to existing balances cardholders had at such dates.

These funding obligations are not included on our consolidated balance sheet. While the bank has not experienced,

and does not anticipate that it will experience, a significant draw down of unfunded credit lines by customers, a

significant draw down would create a cash need at the bank which likely could not be met by our available cash and

funding sources. The bank has the right to reduce or cancel these available lines of credit at any time.

Securitizations. As previously described under “-Securitization of Credit Card Loans,” all of the bank’s

securitization transactions have been accounted for as sales transactions and the credit card loans relating to those

pools of assets are not reflected in our consolidated balance sheet.

Bank Dividend Limitations and Minimum Capital Requirements

The ability of the bank to pay dividends to us is limited. Such dividends, which would only be made at the

discretion of our board of directors and the bank’s board of directors, may be limited by a variety of factors, such

as regulatory capital requirements, dividend restriction statutes, broad enforcement powers possessed by regulatory

agencies and requirements imposed by membership in Visa. Under the Nebraska Banking Act, dividends may only

be paid out of “net profits on hand,” which the Nebraska Banking Act defines as the remainder of all earnings from

current operations plus actual recoveries on loans and investments and other assets, after deducting from the total

thereof all current operating expenses, losses and bad debts, accrued dividends on preferred stock, if any, and federal

and state taxes for the present and two immediately preceding calendar years.