Cabela's 2006 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

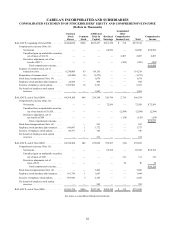

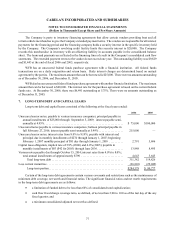

67

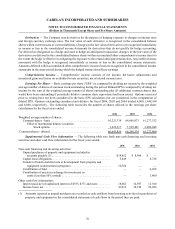

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

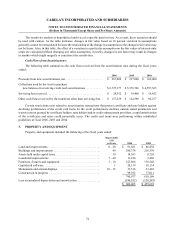

held under capital lease agreements are amortized using the straight-line method over the shorter of the estimated

useful lives of the assets or the lease term. Major improvements that extend the useful life of an asset are charged

to the property and equipment accounts. Routine maintenance and repairs are charged against earnings. The cost of

property and equipment retired or sold and the related accumulated depreciation are removed from the accounts and

any related gain or loss is included in earnings. Long-lived assets used by the Company are reviewed for impairment

whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.

The Company capitalizes interest costs on construction of projects while they are being constructed and before they

are placed into service. For fiscal 2006 and 2005, the Company capitalized interest costs totaling $355 and $371,

respectively.

The Company follows the provisions of American Institute of Certified Public Accountants Statement of

Position (“SOP”) No. 98-1, Accounting for the Cost of Computer Software Developed or Obtained for Internal

Use. In accordance with SOP 98-1, the Company capitalizes all costs related to internally developed or purchased

software and amortizes these costs on a straight-line basis over their estimated useful lives.

Intangible Assets — Intangible assets consist of deferred financing costs, non-compete agreements, purchased

credit card relationships and goodwill and are recorded in other assets. Intangible assets totaled $3,172 and $3,617 at

the end of fiscal 2006 and 2005, respectively, which is net of accumulated amortization of $3,847 and $7,762 for the

respective years. The purchased credit card relationships were fully amortized in fiscal 2005. Intangible assets are

amortized over three to 17 years. Amortization expense for these intangible assets for the next five fiscal years is

estimated to approximate $609 (2007), $326 (2008), $326 (2009), $318 (2010) and $207 (2011).

Land Held for Sale or Development — The Company has a wholly-owned subsidiary whose primary activity

is real estate development. Land that is purchased and held for sale is shown in other assets. Proceeds from sale of

land are recorded in other revenue and the corresponding cost of the land sold is recorded in cost of other revenue.

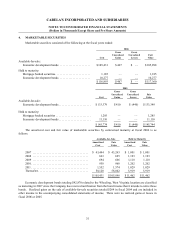

Marketable Securities — Economic development bonds (“bonds”) issued by state and local municipalities that

management has the positive intent and ability to hold to maturity are classified as held-to-maturity and recorded at

amortized cost. For bonds classified as available-for-sale where quoted market prices are not available, fair values

are estimated using present value or other valuation techniques. The fair value estimates are made at a specific point

in time, based on available market information and judgments about the bonds, such as estimates of timing and

amount of expected future cash flows. Such estimates do not reflect any premium or discount that could result from

offering for sale at one time the Company’s entire holdings of a particular bond, nor do they consider the tax impact

of the realization of unrealized gains or losses.

Declines in the fair value of held-to-maturity and available-for-sale bonds and securities below cost that are

deemed to be other than temporary are reflected in earnings as realized losses. Gains and losses on the sale of

securities are recorded on the trade date and determined using the specific identification method.

Government Economic Assistance — In conjunction with the Company’s expansion into new communities,

the Company often receives economic assistance from the local governmental unit in order to encourage economic

expansion in that local government’s area. This assistance typically comes through the use of proceeds from the sale

of economic development bonds and grants. The bond proceeds and grants are made available to fund the purchase

of land (where not donated), construction of the retail facility and infrastructure improvements. The economic

development bonds issued to fund the project, in certain cases, will be repaid by sales taxes generated from the sales

of that retail destination store, while in other cases the economic development bonds are repaid through property

taxes generated within a designated tax area. The government grants have been recorded as deferred grant income

and have been classified as a reduction to the cost basis of the applicable property and equipment. The deferred grant

income is amortized to earnings, as a reduction of depreciation expense, over the average estimated useful life of

the project.