Cabela's 2006 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

71

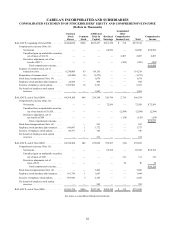

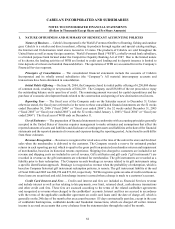

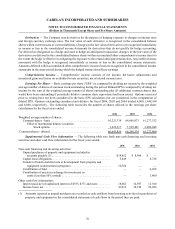

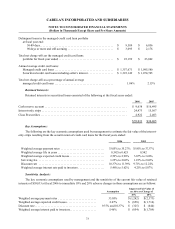

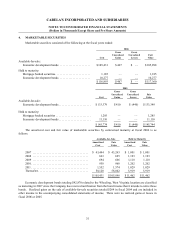

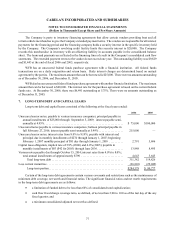

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

Recently Issued Accounting Pronouncements and Regulatory Matters —

In fiscal 2006, SEC Staff Accounting Bulletin No. 108, Considering the Effects of Prior Year Misstatements

when Quantifying Misstatements in Current Year Financial Statements (“SAB 108”) became effective for the

Company. SAB 108 requires that registrants quantify errors using both a balance sheet approach and an income

statement approach and then evaluate whether either approach results in a misstated amount that, when all relevant

quantitative and qualitative factors are considered, is material. The adoption of this bulletin did not have a material

effect on the Company’s financial position or results of operations.

On May 18, 2006, the State of Texas enacted House Bill 3 (“the Bill”), which replaced the State’s current

franchise tax with a “margin tax.” The margin tax is assessed at one-half of one percent of Texas-sourced taxable

margin for retailers and wholesalers. Although the Bill is not an income tax, it has characteristics of an income tax

and accordingly is accounted for as an income tax item under FAS 109, Accounting for Income Taxes. The margin tax

is effective for tax returns originally due on or after January 1, 2008. However, as required by FAS 109, all effects of a

tax law change should be accounted for in the period of the law’s enactment. The impact of this bill on the Company’s

financial position, liquidity, results of operations and effective tax rate was not material for fiscal 2006.

In June 2006, the EITF Task Force reached a consensus on Issue No. 06-3, How Taxes Collected From Customers

and Remitted to Governmental Authorities Should Be Presented in the Income Statement (That Is, Gross versus Net

Presentation). EITF 06-3 concluded that entities should present taxes imposed concurrently on a specific revenue-

producing transaction between a seller and a customer in the income statement on either a gross or a net basis based

on their accounting policy. Disclosure is required if such taxes are significant and presented on a gross basis. This

disclosure is effective for financial statement presentations beginning after December 15, 2006, or beginning in

fiscal 2007 for the Company. Management does not believe that this statement will have a material effect on the

Company’s financial position or results of operations.

On July 13, 2006, the FASB issued Interpretation No. 48, Accounting for Uncertainty in Income Taxes – an

Interpretation of FASB Statement No. 109 (“FIN 48”) which prescribes a recognition threshold and measurement

attribute, as well as criteria for subsequently recognizing, derecognizing and measuring uncertain tax positions for

financial statement purposes. FIN 48 also requires expanded disclosure with respect to the uncertainty in income

tax assets and liabilities. FIN 48 is effective for fiscal years beginning after December 15, 2006, or beginning in

fiscal 2007 for the Company. Management of the Company has determined that the adoption of this statement will

not have a material effect on the Company’s financial position or results of operations.

On August 9, 2006, the Michigan Legislature approved a legislative initiative that repeals the Michigan Single

Business Tax for tax years beginning after December 31, 2007. No replacement tax was included with the repeal. The

Company cannot measure the impact of this change until the replacement tax is enacted.

In February 2006, the FASB issued FAS No. 155, Accounting for Certain Hybrid Financial Instruments – an

amendment to FASB Statements No. 133 and 140 (“FAS 155”) to address issues which had arisen related to FAS

No.133, Accounting for Derivative Instruments and Hedging Activities. FAS 155 allows, among other provisions, a

company to elect fair value measurement of instruments in cases in which a derivative would otherwise have to be

bifurcated. FAS 155 is effective for all financial instruments acquired, issued or subject to a remeasurement (new

basis) event after the beginning of an entity’s first fiscal year beginning after September 15, 2006, or beginning in

fiscal 2007 for the Company. Management does not believe that the adoption of the provisions of this statement will

have a material effect on the Company’s financial position or results of operations.

In March 2006, the FASB issued FAS No. 156, Accounting for Servicing of Financial Assets – an amendment

of FASB Statement No. 140 (“FAS 156”). FAS 156 requires that an entity separately recognize a servicing asset

or servicing liability when it undertakes an obligation to service a financial asset under a servicing contract in

certain situations. Such servicing assets or servicing liabilities are required to be initially measured at fair value, if

practicable. FAS 156 also allows an entity to choose one of two methods when subsequently measuring its servicing