Cabela's 2006 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

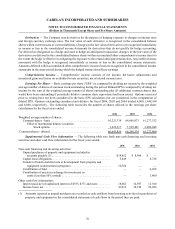

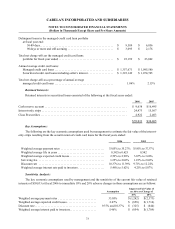

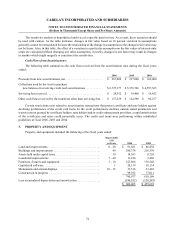

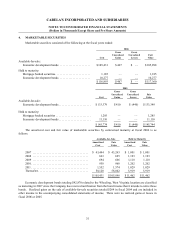

76

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

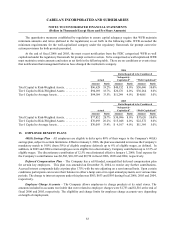

5. TIME DEPOSITS

WFB accepts time deposits only in amounts of at least one hundred thousand dollars. All time deposits are

interest bearing. The aggregate amount of time deposits by maturity as of fiscal 2006 was as follows:

2007 ...................................... $ 33,401

2008 ...................................... 15,300

2009 ...................................... 14,695

2010 ....................................... 19,300

2011 ....................................... 19,000

Thereafter .................................. 500

102,196

Less current maturities . . . . . . . . . . . . . . . . . . . . . . . . (33,401 )

Deposits classified as non-current liabilities . . . . . . . $ 68,795

6. REVOLVING CREDIT FACILITIES

On July 15, 2005, the Company amended and restated its credit agreement with several banks. The amended

and restated credit agreement provides for a $325,000 unsecured revolving credit facility that expires on June 30,

2010. The credit agreement was also amended eliminating certain limitations regarding pay downs of revolving

loans advanced; therefore, advances made pursuant to this credit agreement are classified as long-term debt. The

credit facility may be increased to $450,000 upon request of the Company and the consent of the banks party to the

credit agreement. The credit agreement permits the issuance of up to $150,000 in letters of credit and standby letters

of credit, the nominal amount of which are applied against the overall credit limit available under the credit facility.

During the term of the facility, the Company is required to pay a quarterly facility fee, which ranges from 0.10% to

0.25% of the average daily unused principal balance on the line of credit. Interest on advances on this credit facility

is calculated at the greater of (i) the lead lender’s prime rate, (ii) the average rate on the federal funds rate in effect for

the day plus one-half of one percent or (iii) the Eurodollar rate of interest plus a margin, as defined. The weighted

average interest rate for borrowings on the line of credit was 5.84% during fiscal 2006. At December 30, 2006, no

principal amounts were outstanding on the line of credit. However, letters of credit and standby letters of credit

totaling $54,582 were outstanding at December 30, 2006. The average principal amount outstanding during fiscal

2006 was $6,851. The credit agreement requires that the Company comply with certain financial and other customary

covenants, including

• a fixed charge coverage ratio (as defined) of no less than 1.50 to 1.00 as of the last day of any fiscal

quarter;

• a cash flow leverage ratio (as defined) of no more than 3.00 to 1.00 as of the last day of any fiscal quarter;

and

• a minimum tangible net worth standard (as defined).

The credit agreement includes a dividend provision limiting the amount that the Company could pay to

stockholders, which at December 30, 2006, was not in excess of $99,471. The agreement also has a provision

permitting acceleration by the lenders in the event there is a change in control, as defined. In addition, the credit

agreement contains cross default provisions to other outstanding debt. In the event the Company fails to comply with

these covenants, a default is triggered. In the event of default, all outstanding letters of credit and all principal and

outstanding interest would immediately become due and payable. See “Credit Facilities and Other Indebtedness”

under “Liquidity and Capital Resources” in the “Management’s Discussion and Analysis of Financial Condition

and Results of Operations” for additional information on the covenants associated with this credit agreement. The

Company was in compliance with all financial debt covenants at December 30, 2006.