Cabela's 2006 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2006 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

56

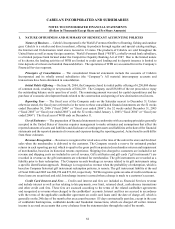

In June 2006, the EITF Task Force reached a consensus on Issue No. 06-3, How Taxes Collected From Customers

and Remitted to Governmental Authorities Should Be Presented in the Income Statement (That Is, Gross versus Net

Presentation). EITF 06-3 concluded that entities should present taxes imposed concurrently on a specific revenue-

producing transaction between a seller and a customer in the income statement on either a gross or a net basis based

on their accounting policy. Disclosure is required if such taxes are significant and presented on a gross basis. This

disclosure is effective for financial statement presentations beginning after December 15, 2006, or beginning in

fiscal 2007 for the Company. We do not believe that this statement will have a material effect on the Company’s

financial position or results of operations.

On July 13, 2006, the FASB issued Interpretation No. 48, Accounting for Uncertainty in Income Taxes – an

Interpretation of FASB Statement No. 109 (“FIN 48”) which prescribes a recognition threshold and measurement

attribute, as well as criteria for subsequently recognizing, derecognizing and measuring uncertain tax positions for

financial statement purposes. FIN 48 also requires expanded disclosure with respect to the uncertainty in income tax

assets and liabilities. FIN 48 is effective for fiscal years beginning after December 15, 2006, or beginning in fiscal

2007 for the Company. We have determined that this statement will not have a material effect on the Company’s

financial position or results of operations.

In February 2006, the FASB issued FAS No. 155, Accounting for Certain Hybrid Financial Instruments – an

amendment to FASB Statements No. 133 and 140 (“FAS 155”) to address issues which had arisen related to FAS

No.133, Accounting for Derivative Instruments and Hedging Activities. FAS 155 allows, among other provisions, a

company to elect fair value measurement of instruments in cases in which a derivative would otherwise have to be

bifurcated. FAS 155 is effective for all financial instruments acquired, issued or subject to a remeasurement (new

basis) event after the beginning of an entity’s first fiscal year beginning after September 15, 2006, or beginning in

fiscal 2007 for the Company. We do not believe that the adoption of the provisions of this statement will have a

material effect on the Company’s financial position or results of operations.

In March 2006, the FASB issued FAS No. 156, Accounting for Servicing of Financial Assets – an amendment

of FASB Statement No. 140 (“FAS 156”). FAS 156 requires that an entity separately recognize a servicing asset

or servicing liability when it undertakes an obligation to service a financial asset under a servicing contract in

certain situations. Such servicing assets or servicing liabilities are required to be initially measured at fair value, if

practicable. FAS 156 also allows an entity to choose one of two methods when subsequently measuring its servicing

assets and servicing liabilities: (1) the amortization method or (2) the fair value measurement method This statement

is effective as of the beginning of an entity’s first fiscal year that begins after September 15, 2006, or beginning

in fiscal 2007 for the Company. We do not believe that the adoption of the provisions of this statement will have a

material effect on the Company’s financial position or results of operations.

In September 2006, the FASB issued FAS No. 157, Fair Value Measurements (“FAS 157”). This statement

enhances existing guidance for measuring and disclosing the fair value of assets and liabilities for more consistency

and comparability. FAS 157 provides a single definition of fair value, together with a framework for measuring it,

and requires expanded disclosures to provide information about the extent to which fair value is used to measure

assets and liabilities, the methods and assumptions used to measure fair value, and the effect of fair value measures

on earnings. FAS 157 is effective for financial statements issued in fiscal years beginning after November 15, 2007.

We do not believe that the adoption of the provisions of this statement will have a material effect on the Company’s

financial position or results of operations.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We are exposed to interest rate risk through our bank’s operations and, to a lesser extent, through our

merchandising operations. We also are exposed to foreign currency risk through our merchandising operations.

Financial Services Interest Rate Risk

Interest rate risk refers to changes in earnings or the net present value of assets and off-balance sheet positions

less liabilities (termed “economic value of equity”) due to interest rate changes. To the extent that interest income

collected on managed loans and interest expense do not respond equally to changes in interest rates, or that rates do

not change uniformly, securitization earnings and economic value of equity could be affected. Our net interest income

on managed credit card loans is affected primarily by changes in short term interest rate indices such as LIBOR and