Google 2015 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2015 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

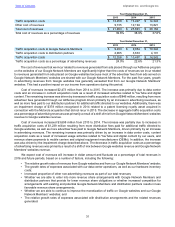

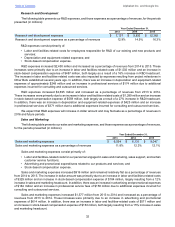

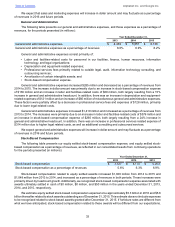

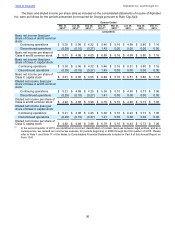

Table of Contents Alphabet Inc. and Google Inc.

41

of assets acquired and liabilities assumed, management makes significant estimates and assumptions, especially with

respect to intangible assets.

Critical estimates in valuing certain intangible assets include but are not limited to future expected cash flows

from customer relationships and acquired patents and developed technology; and discount rates. Management’s

estimates of fair value are based upon assumptions believed to be reasonable, but which are inherently uncertain and

unpredictable and, as a result, actual results may differ from estimates.

Other estimates associated with the accounting for acquisitions may change as additional information becomes

available regarding the assets acquired and liabilities assumed, as more fully discussed in Note 6 of Notes to

Consolidated Financial Statements included in Item 8 of this Annual Report on Form 10-K.

Goodwill

Goodwill is allocated to reporting units expected to benefit from the business combination. We evaluate our

reporting units when changes in our operating structure occur, and if necessary, reassign goodwill using a relative fair

value allocation approach. We test goodwill for impairment at the reporting unit level at least annually, or more frequently

if events or changes in circumstances indicate that the asset may be impaired. Goodwill impairment tests require

judgment, including the identification of reporting units, assignment of assets and liabilities to reporting units, assignment

of goodwill to reporting units, and determination of the fair value of each reporting unit. As of December 31, 2015, no

impairment of goodwill has been identified.

Long-lived Assets

Long-lived assets, including property and equipment, long-term prepayments, and intangible assets, excluding

goodwill, are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount

of an asset may not be recoverable. The evaluation is performed at the lowest level of identifiable cash flows independent

of other assets. An impairment loss would be recognized when estimated undiscounted future cash flows generated

from the assets are less than their carrying amount. Measurement of an impairment loss would be based on the excess

of the carrying amount of the asset group over its fair value.

Impairment of Marketable and Non-Marketable Securities

We periodically review our marketable and non-marketable securities for impairment. If we conclude that any of

these investments are impaired, we determine whether such impairment is other-than-temporary. Factors we consider

to make such determination include the duration and severity of the impairment, the reason for the decline in value

and the potential recovery period and our intent to sell. For marketable debt securities, we also consider whether (1)

it is more likely than not that we will be required to sell the security before recovery of its amortized cost basis, and

(2) the amortized cost basis cannot be recovered as a result of credit losses. If any impairment is considered other-

than-temporary, we will write down the asset to its fair value and record the corresponding charge as other income

(expense), net.

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We are exposed to financial market risks, including changes in currency exchange rates and interest rates.

Foreign Currency Exchange Risk

We transact business globally in multiple currencies. Our international revenues, as well as costs and expenses

denominated in foreign currencies, expose us to the risk of fluctuations in foreign currency exchange rates against the

U.S. dollar. We are a net receiver of foreign currencies and therefore benefit from a weakening of the U.S. dollar and

are adversely affected by a strengthening of the U.S. dollar relative to the foreign currency. As of December 31, 2015,

our most significant currency exposures are the British pound, Euro, and Japanese yen.

We use foreign exchange option contracts to protect our forecasted U.S. dollar-equivalent earnings from adverse

changes in foreign currency exchange rates. These hedging contracts reduce, but do not entirely eliminate the impact

of adverse currency exchange rate movements. We designate these option contracts as cash flow hedges for

accounting purposes. The fair value of the option contract is separated into its intrinsic and time values. Changes in

the time value are recorded in other income (expense), net. Changes in the intrinsic value are recorded as a component

of accumulated other comprehensive income (AOCI) and subsequently reclassified into revenues to offset the hedged

exposures as they occur.

We considered the historical trends in currency exchange rates and determined that it was reasonably possible

that changes in exchange rates of 20% could be experienced in the near term. If the U.S. dollar weakened by 20% as

of December 31, 2014 and December 31, 2015, the amount recorded in AOCI reflecting intrinsic value related to our