Google 2015 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2015 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

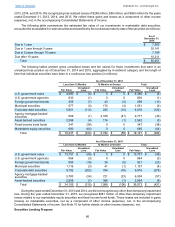

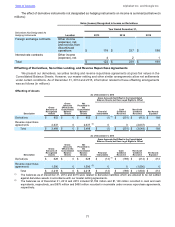

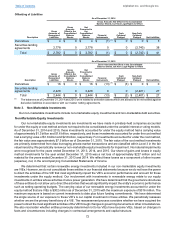

Table of Contents Alphabet Inc. and Google Inc.

62

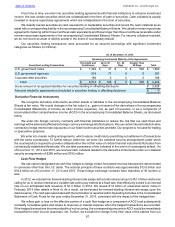

We have accounted for our non-marketable investments that meet the definition of a debt security as available-

for-sale securities. Since these securities do not have contractual maturity dates and we do not intend to liquidate

them in the next 12 months, we have classified them as non-current assets on the accompanying Consolidated Balance

Sheet.

Variable Interest Entities

We make a determination at the start of each arrangement whether an entity in which we have made an investment

is considered a Variable Interest Entity (“VIE”). We consolidate VIEs in which we have a controlling financial interest.

If we do not have a controlling financial interest in a VIE, we account for the investment under either the equity or cost

method.

Impairment of Marketable and Non-Marketable Investments

We periodically review our marketable and non-marketable investments for impairment. If we conclude that any

of these investments are impaired, we determine whether such impairment is other-than-temporary. Factors we consider

to make such determination include the duration and severity of the impairment, the reason for the decline in value

and the potential recovery period and our intent to sell. For debt securities, we also consider whether (1) it is more

likely than not that we will be required to sell the security before recovery of its amortized cost basis, and (2) the

amortized cost basis cannot be recovered as a result of credit losses. If any impairment is considered other-than-

temporary, we will write down the asset to its fair value and record the corresponding charge as other income (expense),

net.

Accounts Receivable

We record accounts receivable at the invoiced amount and we normally do not charge interest. We maintain an

allowance for doubtful accounts to reserve for potentially uncollectible receivables. We review the accounts receivable

by amounts due by customers which are past due to identify specific customers with known disputes or collectability

issues. In determining the amount of the reserve, we make judgments about the creditworthiness of significant

customers based on ongoing credit evaluations. We also maintain a sales allowance to reserve for potential credits

issued to customers. We determine the amount of the reserve based on historical credits issued.

Property and Equipment

We account for property and equipment at cost less accumulated depreciation and amortization. We compute

depreciation using the straight-line method over the estimated useful lives of the assets, generally two to five years.

We depreciate buildings over periods up to 25 years. We amortize leasehold improvements over the shorter of the

remaining lease term or the estimated useful lives of the assets. Construction in progress is the construction or

development of property and equipment that have not yet been placed in service for our intended use. Depreciation

for equipment commences once it is placed in service and depreciation for buildings and leasehold improvements

commences once they are ready for our intended use. Land is not depreciated.

Software Development Costs

We expense software development costs, including costs to develop software products or the software component

of products to be marketed to external users, before technological feasibility is reached. Technological feasibility is

typically reached shortly before the release of such products and as a result, development costs that meet the criteria

for capitalization were not material for the periods presented.

Software development costs also include costs to develop software to be used solely to meet internal needs and

cloud based applications used to deliver our services. We capitalize development costs related to these software

applications once the preliminary project stage is complete and it is probable that the project will be completed and

the software will be used to perform the function intended. Costs capitalized for developing such software applications

were not material for the periods presented.

Business Combinations

We include the results of operations of the businesses that we acquire as of the respective dates of acquisition.

We allocate the fair value of the purchase price of our acquisitions to the assets acquired and liabilities assumed based

on their estimated fair values. The excess of the fair value of the purchase price over the fair values of these identifiable

assets and liabilities is recorded as goodwill.

Long-Lived Assets Including Goodwill and Other Acquired Intangible Assets

We review property and equipment, long-term prepayments and intangible assets, excluding goodwill, for

impairment whenever events or changes in circumstances indicate the carrying amount of an asset may not be