Toyota 2006 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2006 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

98

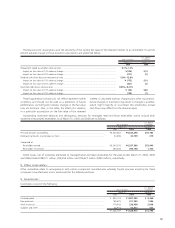

Unrealized losses continuously over a 12 month period or

more in the aggregate were not material at March 31, 2005

and 2006.

At March 31, 2005 and 2006, debt securities classified as

available-for-sale mainly consist of government bonds and

corporate debt securities with maturities from 1 to 10 years.

Proceeds from sales of available-for-sale securities were

¥183,808 million, ¥121,369 million and ¥157,707 million

($1,342 million) for the years ended March 31, 2004, 2005

and 2006, respectively. On those sales, gross realized gains

were ¥8,780 million, ¥14,551 million and ¥2,104 million ($18

million) and gross realized losses were ¥139 million, ¥231 mil-

lion and ¥1,207 million ($10 million), respectively.

During the year ended March 31, 2006, in accordance with

EITF Issue No. 91-5, Nonmonetary Exchange of Cost-Method

Investments, Toyota reclassified ¥143,366 million ($1,220 mil-

lion) of gain from Unrealized gains on securities included in

the “Accumulated other comprehensive income” on the con-

solidated balance sheet to Other income included in the

“Other income, net” on the consolidated statement of

income. The gain was recognized based on the merger

between UFJ Holdings, Inc. and Mitsubishi Tokyo Financial

Group, Inc. on October 1, 2005, and determined as the

amount between the cost of the pre-merger entity, UFJ

Holdings, Inc. common shares which Toyota had continuously

held and the fair market value of the post-merger entity,

Mitsubishi UFJ Financial Group, Inc. common shares which

Toyota received in exchange for UFJ Holdings, Inc. common

shares. The gain was non-cash gain and included in the cost

of the available-for-sale equity securities as of March 31,

2006.

During the years ended March 31, 2004, 2005 and 2006,

Toyota recognized impairment losses on available-for-sale

securities of ¥3,063 million, ¥2,324 million, and ¥4,163 mil-

lion ($35 million), respectively, which are included in “Other

income, net” in the accompanying consolidated statements of

income.

In the ordinary course of business, Toyota maintains long-

term investment securities, included in “Marketable securities

and other securities investments” and issued by a number of

non-public companies which are recorded at cost, as their fair

values were not readily determinable. Management employs a

systematic methodology to assess the recoverability of such

investments by reviewing the financial viability of the underly-

ing companies and the prevailing market conditions in which

these companies operate to determine if Toyota’s investment

in each individual company is impaired and whether the

impairment is other-than-temporary. Toyota performs this

impairment test semi-annually for significant investments

recorded at cost. If the impairment is determined to be other-

than-temporary, the cost of the investment is written-down by

the impaired amount and the losses are recognized currently

in operations.

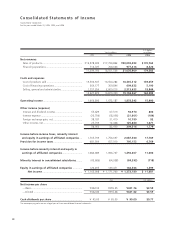

7. Finance receivables:

Finance receivables consist of the following:

U.S. dollars

Yen in millions in millions

March 31, March 31,

2005 2006 2006

Retail .................................................................................................................................. ¥ 4,716,961 ¥ 5,930,822 $ 50,488

Finance leases ..................................................................................................................... 756,732 741,280 6,310

Wholesale and other dealer loans ........................................................................................ 1,773,440 1,998,814 17,016

7,247,133 8,670,916 73,814

Deferred origination costs ................................................................................................... 65,189 92,798 790

Unearned income................................................................................................................ (233,417) (334,796) (2,850)

Allowance for credit losses .................................................................................................. (91,829) (101,383) (863)

Total finance receivables, net....................................................................................... 6,987,076 8,327,535 70,891

Less—Current portion ......................................................................................................... (3,010,135) (3,497,319) (29,772)

Noncurrent finance receivables, net ............................................................................. ¥ 3,976,941 ¥ 4,830,216 $ 41,119