Toyota 2006 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2006 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

80

Related Party Transactions

Toyota does not have any significant related party transactions

other than transactions with affiliated companies in the ordi-

nary course of business as described in note 12 to the consoli-

dated financial statements.

Legislation Regarding End-of-Life Vehicles

In September 2000, the European Union approved a directive

that requires member states to promulgate regulations imple-

ment the following:

• manufacturers shall bear all or a significant part of the costs

for taking back end-of-life vehicles put on the market after

July 1, 2002 and dismantling and recycling those vehicles.

Beginning January 1, 2007, this requirement will also be

applicable to vehicles put on the market before July 1, 2002;

• manufacturers may not use certain hazardous materials in

vehicles sold after July 2003;

• vehicles type-approved and put on the market after December

15, 2008, shall be re-usable and/or recyclable to a minimum

of 85% by weight per vehicle and shall be re-usable and/or

recoverable to a minimum of 95% by weight per vehicle; and

• end-of-life vehicles must meet actual re-use of 80% and re-

use as material or energy of 85%, respectively, of vehicle

weight by 2006, rising to 85% and 95%, respectively, by

2015.

See note 23 to the consolidated financial statements for further

discussion.

Recent Accounting Pronouncements

in the United States

In November 2004, the Financial Accounting Standards Board

(“FASB”) issued FAS No. 151, Inventory Costs—an amendment

of ARB No. 43, Chapter 4 (“FAS 151”). FAS 151 amends the

guidance in ARB No. 43, Chapter 4, “Inventory Pricing,” to clari-

fy the accounting for abnormal amounts of idle facility expense,

freight, handling costs, and wasted material (spoilage).

Paragraph 5 of ARB No. 43, Chapter 4, previously stated that

“...under some circumstances, items such as idle facility

expense, excessive spoilage, double freight, and rehandling

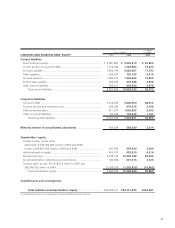

Yen in millions

Payments Due by Period

Less than 1 to 3 3 to 5 5 years and

Total 1 year years years after

Contractual Obligations:

Short-term borrowings (note 13)

Loans....................................................................................... ¥ 986,128 ¥ 986,128

Commercial paper.................................................................... 2,046,891 2,046,891

Long-term debt * (note 13).......................................................... 7,306,037 1,709,231 ¥3,161,232 ¥1,434,838 ¥1,000,736

Capital lease obligations (note 13)................................................ 58,341 14,657 17,402 25,736 546

Non-cancelable operating lease obligations (note 22) .................. 51,495 9,740 13,565 9,101 19,089

Commitments for the purchase of property,

plant and other assets (note 23)................................................. 103,324 97,152 6,172 — —

Total ........................................................................................ ¥10,552,216 ¥4,863,799 ¥3,198,371 ¥1,469,675 ¥1,020,371

* “Long-term debt” represents future principal payments.

Toyota expects to contribute ¥98,561 million to its pension plans in during fiscal 2007.

Yen in millions

Amount of Commitment Expiration Per Period

Total

Amounts Less than 1 to 3 3 to 5 5 years and

Committed 1 year years years after

Commercial Commitments:

Maximum potential exposure to guarantees given

in the ordinary course of business (note 23) ............................... ¥1,236,977 ¥380,152 ¥587,137 ¥223,862 ¥45,826

Total Commercial Commitments .............................................. ¥1,236,977 ¥380,152 ¥587,137 ¥223,862 ¥45,826