Toyota 2006 Annual Report Download - page 111

Download and view the complete annual report

Please find page 111 of the 2006 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

109

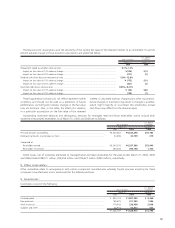

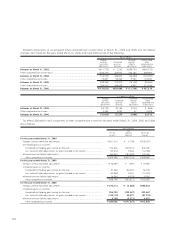

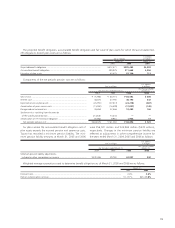

The Japanese Commercial Code provides that an amount

equal to at least 10% of cash dividends and other distribu-

tions from retained earnings paid by the parent company and

its Japanese subsidiaries be appropriated as a legal reserve. No

further appropriation is required when total amount of the

legal reserve and capital surplus reaches 25% of stated capital.

The legal reserve included in retained earnings as of March 31,

2005 and 2006 was ¥141,064 million and ¥145,103 million

($1,235 million), respectively. The legal reserve is restricted

and unable to be used for dividend payments, and is excluded

from the calculation of the profit available for dividend.

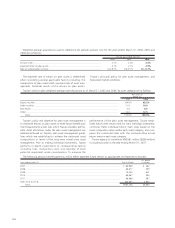

The amounts of statutory retained earnings of the parent

company available for dividend payments to shareholders

were ¥4,864,555 million and ¥5,255,265 million ($44,737

million) as of March 31, 2005 and 2006, respectively. In

accordance with customary practice in Japan, the appropria-

tions are not accrued in the financial statements for the corre-

sponding period, but are recorded in the subsequent

accounting period after shareholders’ approval has been

obtained. Retained earnings at March 31, 2006 include

amounts representing year-end cash dividends of ¥178,297

million ($1,518 million), ¥55 ($0.47) per share, which were

approved at the Ordinary General Shareholders’ Meeting held

on June 23, 2006.

Retained earnings at March 31, 2006 include ¥1,055,422

million ($8,985 million) relating to equity in undistributed

earnings of companies accounted for by the equity method.

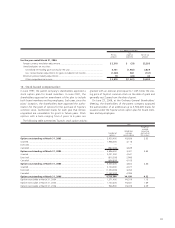

In June 26, 1997, the shareholders of the parent company

approved a stock repurchase policy at the Ordinary General

Shareholders’ Meeting in accordance with the Japanese

Commercial Code, which allows the company to purchase

treasury stock only for the purpose of retirement of the stock

with a resulting reduction in retained earnings. Under the

stock repurchase policy, the shareholders authorized the

parent company to repurchase up to 370 million shares of its

common stock without the limitation of time, subject to the

approval of the Board of Directors. In October 2001, the

Japanese Commercial Code was changed to allow the compa-

ny to purchase treasury stock without limitation of reason

during the whole period until the next Ordinary General

Shareholders’ Meeting by the resolution of the Board of

Directors up to the limitation of number of shares and aggre-

gated acquisition costs approved at the Ordinary General

Shareholders’ Meeting. In response to the Japanese

Commercial Code revision, on June 26, 2002, at the Ordinary

General Shareholders’ Meeting, the shareholders of the parent

company approved the amendment of the stock repurchase

policy in the Articles of Incorporation to be deleted the limita-

tion of the purpose of purchasing treasury stock noted above.

As a result, Toyota’s unused authorized shares for the repur-

chase of shares of common stock under the legacy policy

elapsed. In the same Shareholders’ Meeting, the shareholders

of the parent company also approved the purchase as treasury

stock of up to 170 million shares at a cost up to ¥600,000

million during the period until the next Ordinary General

Shareholders’ Meeting which was held on June 26, 2003. As a

result, the parent company repurchased approximately 170

million shares during the approved period of time. On June

26, 2003, at the Ordinary General Shareholders’ Meeting, the

shareholders of the parent company again approved to pur-

chase up to 150 million of its common stock at a cost up to

¥400,000 million during the period until the next Ordinary

General Shareholders’ Meeting which was held on June 23,

2004. According to this authorization, the parent company

purchased approximately 113 million shares of its treasury

stock during the approved period of time. On June 23, 2004,

at the Ordinary Shareholders’ Meeting, the shareholders of

the parent company again approved to purchase up to 65

million of its common stock at a cost up to ¥250,000 million

during the period until the next Ordinary General

Shareholders’ Meeting which was held on June 23, 2005,

and, in response to the Japanese Commercial Code revision,

also approved to change the Articles of Incorporation to

authorize the Board of Directors to repurchase treasury stock

on the basis of its resolution. During this approved period of

time, the parent company purchased approximately 59 million

of shares. On June 23, 2005, the shareholders of the parent

company approved to purchase up to 65 million of its

common stock at a cost up to ¥250,000 million during the

period until the next Ordinary General Shareholders’ Meeting

which was held on June 23, 2006. As a result, the parent

company repurchased approximately 38 million shares during

the approved period of time. In addition, on June 23, 2006, at

the Ordinary General Shareholders’ Meeting, the shareholders

of the parent company approved to purchase up to 30 million

of its common stock at a cost up to ¥200,000 million during

the purchase period of one year from the following day. These

approvals by the shareholders on and after the resolution in

the Ordinary General Shareholders’ Meeting on June 23, 2004

are not required under the current regulation.

In years prior to 1997, Toyota had made free distributions

of shares to its shareholders for which no accounting entry is

required in Japan. Had the distributions been accounted for in

a manner used by companies in the United States of America,

¥2,576,606 million ($21,934 million) would have been trans-

ferred from retained earnings to the appropriate capital

accounts.