Toyota 2006 Annual Report Download - page 97

Download and view the complete annual report

Please find page 97 of the 2006 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

95

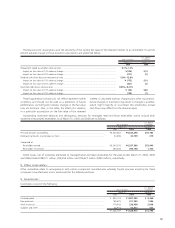

Accounting changes—

In December 2004, FASB issued FAS No. 153, Exchanges of

Nonmonetary Assets—an amendment of APB Opinion No. 29

(“FAS 153”). The guidance in APB Opinion No. 29, Accounting

for Nonmonetary Transactions, is based on the principle that

exchanges of nonmonetary assets should be measured based

on the fair value of the assets exchanged. The guidance in

that Opinion; however, included certain exceptions to that

principle. FAS 153 amends Opinion 29 to eliminate the excep-

tion for nonmonetary exchanges of similar productive assets

and replaces it with a general exception for exchanges of non-

monetary assets that do not have commercial substance. A

nonmonetary exchange has commercial substance if the

future cash flows of the entity are expected to change signifi-

cantly as a result of the exchange. Toyota adopted FAS 153

for nonmonetary asset exchanges occurring in and after fiscal

periods begun after June 15, 2005. The adoption of FAS 153

did not have material impact on Toyota’s consolidated finan-

cial statements.

In March 2005, FASB issued the FASB Interpretation No. 47,

Accounting for Conditional Asset Retirement Obligations—an

interpretation of FASB Statement No. 143 (“FIN 47”). This

Interpretation clarifies that the term conditional asset retire-

ment obligation as used in FASB Statement No. 143,

Accounting for Asset Retirement Obligations, refers to a legal

obligation to perform an asset retirement activity in which the

timing and (or) method of settlement are conditional on a

future event that may or may not be within the control of the

entity. FIN 47 requires a company to recognize a liability for

the fair value of a conditional asset retirement obligation if the

fair value of the liability can be reasonably estimated. The fair

value of a liability for the conditional asset retirement obliga-

tion should be recognized when incurred. Toyota adopted FIN

47 in the fiscal periods ended after December 15, 2005. The

adoption of FIN 47 did not have material impact on Toyota’s

consolidated financial statements.

Recent pronouncements to be adopted in future

periods—

In November 2004, FASB issued FAS No. 151, Inventory

Costs—an amendment of ARB No. 43, Chapter 4 (“FAS 151”).

FAS 151 amends the guidance in ARB No. 43, Chapter 4,

“Inventory Pricing,” to clarify the accounting for abnormal

amounts of idle facility expense, freight, handling costs, and

wasted material (spoilage). Paragraph 5 of ARB 43, Chapter 4,

previously stated that “…under some circumstances, items

such as idle facility expense, excessive spoilage, double freight,

and rehandling costs may be so abnormal as to require treat-

ment as current period charges…”. FAS 151 requires that

those items be recognized as current-period charges regard-

less of whether they meet the criterion of “so abnormal.”

In addition, this Statement requires that allocation of fixed

production overheads to the costs of conversion be based on

the normal capacity of the production facilities. FAS 151 is

effective for inventory costs incurred during fiscal years begin-

ning after June 15, 2005. Management does not expect this

statement to have a material impact on Toyota’s consolidated

financial statements.

In December 2004, FASB issued FAS No. 123(R), Share-

Based Payment (revised 2004) (“FAS 123(R)”). FAS 123(R) is a

revision of FAS 123, supersedes APB 25, and its related imple-

mentation guidance. FAS 123(R) requires a public entity to

measure the cost of employee services received in exchange

for an award of equity instruments based on the grant-date

fair value of the award. That cost will be recognized over the

period during which an employee is required to provide ser-

vice in exchange for the award. FAS 123(R) also requires a

public entity to initially measure the cost of employee services

received in exchange for an award of liability instruments

based on its current fair value; the fair value of that award will

be remeasured subsequently at each reporting date through

the settlement date. Changes in fair value will be recognized

as compensation cost over that period. Although Toyota is

required to implement the standard as of the beginning of the

first interim or annual period that begins after June 15, 2005

under Statement No. 123(R), the Securities and Exchange

Commission has amended the compliance date and Toyota is

required to adopt the Standard for the year ending March 31,

2007. Management does not expect this statement to have a

material impact on Toyota’s consolidated financial statements.

In May 2005, FASB issued FAS No. 154, Accounting

Changes and Error Corrections—a replacement of APB No. 20

and FAS No. 3 (“FAS 154”). FAS 154 replaces APB Opinion

No. 20, Accounting Changes, and FASB Statement No. 3,

Reporting Accounting Changes in Interim Financial

Statements, and changes the requirements for the accounting

for and reporting of a change in accounting principle. FAS

154 applies to all voluntary changes in accounting principle. It

also applies to changes required by an accounting pronounce-

ment when the pronouncement does not include specific

transition provisions. APB Opinion 20 previously required that

most voluntary changes in accounting principle be recognized

by including in net income of the period of the change the

cumulative effect of changing to the new accounting princi-

ple. FAS 154 requires retrospective application to prior peri-

ods’ financial statements of changes in accounting principle.

FAS 154 is effective for accounting changes and corrections of

errors made in fiscal years beginning after December 15,

2005. The impact of applying FAS 154 will depend on the

change, if any, that Toyota may identify and record in future

periods.