APC 2006 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2006 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Consolidated financial statements at December 31, 2006

Interest rate swaps

Interest rate swaps, which synthetically adjust interest

rates on certain indebtedness, involve the exchange of

fixed and floating-rate interest payments. The differen-

tial to be paid (or received) is accrued (or deferred) as

an adjustment to interest income or expense over the

life of the agreement. The Group does not apply hedge

accounting as described in IAS 39 for interest rate

swaps. The impact is immediately recognized in the

income statement.

Commodity contracts

The Group also enters into raw material forward pur-

chase contracts. Moreover the Group enters into con-

tracts including swaps and options to hedge price risks

on all or part of its forecast future purchases. Under

IAS 39, these qualify as cash flow hedges. The hedg-

ing instruments are recognized in the balance sheet

and are measured at fair value at the period-end. The

portion of the gain or loss on the hedging instrument

that is determined to be an effective hedge is accumu-

lated in equity, under other reserves, and reclassified

into the income statement under cost of sales when

the hedged transaction affects profit or loss, leading to

an adjustment of gross profit. The ineffective portion of

the gain or loss on the hedging instrument is immedi-

ately recognized in other financial income and

expense.

Cash flows from derivative financial instruments are

recognized in the statement of cash flows in a manner

consistent with the underlying transactions.

Asset-backed securities issued by the

Special Purpose Entity holding perpetual

bonds

In accordance with SIC 12 –

Special Purpose Entities

– and IAS 39, the special purpose entity that holds the

perpetual bonds issued by the Group in 1991 was con-

solidated at December 31, 2005.

The swaps taken out by the special purpose entity in

connection with the perpetual bonds have been meas-

ured at fair value.

Interest rate swaps on the perpetual bonds taken out

directly by the Group are classified as derivative instru-

ments that do not qualify for hedge accounting. They

are therefore measured at fair value and gains and

losses arising from remeasurement at fair value are

recorded in other financial income and expense.

On December 15, 2006, the Group bought back the

perpetual bonds issued in 1991 from the special pur-

pose entity. As a result, the special purpose entity was

no longer consolidated at December 31, 2006.

Put options granted to minority

shareholders

Under IAS 32 –

Financial Instruments: Disclosure and

Presentation,

commitments to buy out minority share-

holders (e.g. put options) must be recognized in debt,

in an amount corresponding to the purchase price of

the minority interest.

In the absence of established accounting practice, the

difference between the purchase price of the minority

interests and the share in the acquired net assets has

been posted to goodwill without remeasuring the

acquired assets and liabilities. Subsequent changes in

the fair value of the debt will be recognized by adjust-

ing goodwill.

1.22 - Revenue recognition

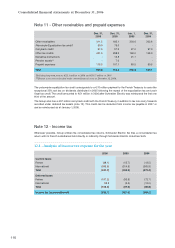

The Group’s revenues primarily include merchandise

sales and revenues from service and project contracts.

Merchandise sales

Revenue from sales is recognized when the product is

shipped and title transferred (standard shipping terms

are FOB).

Rebates offered to the distributors are accrued as a

deduction from revenue when the products are sold to

the distributor.

Certain subsidiaries also offer cash discounts to dis-

tributors. These discounts are deducted from sales.

Total sales are presented net of these discounts and

rebates.

Service contracts

Revenue from service contracts is recorded over the

contractual period of service. It is recognized when the

result of the transaction can be reliably determined, by

the percentage of completion method.

Long-term contracts

Income from long-term contracts is recognized using

the percentage-of-completion method, based either on

the percentage of costs incurred in relation to total esti-

mated costs of the entire contract, or on the contract’s

technical milestones, notably proof of installation or

delivery of equipment. When a contract includes per-

formance clauses in the Group’s favor, the related rev-

enue is recognized at each project milestone and a

provision is set aside if targets are not met.

Losses at completion for a given contract are provided

for in full as soon as they become probable. The cost

of work-in-process includes direct and indirect costs

relating to the contracts.

1.23 - Earnings per share

Earnings per share is calculated in accordance with

IAS 33 –

Earnings per share.

Diluted earnings per share is calculated by adjusting

profit and the weighted average number of shares out-

standing for the dilutive effect of the exercise of stock

options outstanding at the balance sheet date. The

dilutive effect of stock options is determined by apply-

ing the "treasury stock" method, which consists of tak-

ing into account the number of shares that could be

purchased, based on the average share price for the

year, using the proceeds from the exercise of the rights

attached to the options.

1.24 - Statement of cash flows

The consolidated statement of cash flows has been

prepared using the "indirect method", which consists

of reconciling net profit to net cash provided by opera-

tions. Net cash and cash equivalents represent cash

and cash equivalents as presented in the balance

sheet (note 1.15) net of bank overdrafts.

106