APC 2006 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2006 APC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

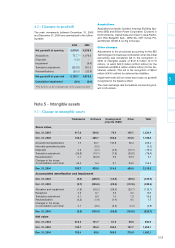

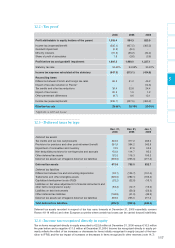

Note 2 - Application of IAS 32 and IAS 39 as from January 1, 2005

IAS 32 –

Financial Instruments – Disclosure and Presentation

and IAS 39 –

Financial Instruments – Recognition and Measure-

ment

– have been applied as from January 1, 2005.

The following table, which reconciles the closing balance sheet for 2004 with the opening balance sheet for 2005, shows the

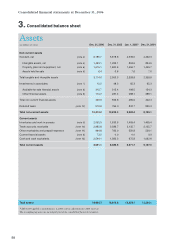

impact on the main balance sheet items affected by the application of IAS 32 and IAS 39.

Dec. 31, 2004 Treasury Fair value Hedging Derivative Perpetual Puts Jan. 1, 2005

IFRS before stock adjustment instruments instruments bonds granted IFRS

IAS 32 and 39 not qualifying to minority including

for hedge interests IAS 32 and 39

Goodwill 4,462.3 76.7 4,539.0

Available-for-sale financial assets 154.3 44.2 198.5

Deferred tax assets 830.3 1.0 1.4 832.7

Other accounts receivable 529.1 19.9 1.8 550

.

8

Cash and cash equivalents 1,062.8 (87.0) 975.8

Other assets 6,257.3 6,257.3

Total Assets 13,296.1 (87.0) 44.2 19.9 2.8 1.4 76.7 13,354.1

Retained earnings, net of tax 1,797.5 (1.2) (2.7) 1,793.6

Own shares reserve (199.7) (87.0) (286.7)

Other reserves, net of tax 22.3 29.0 12.9 64.2

Translation reserve (84.5) 0.2 (84.3)

Total equity attributable to equity

holders of the parent 7,395.1 (87.0) 29.0 12.9 (1.0) (2.7) 0.0 7,346.3

Minority interests 72.8 3.4 76.2

Perpetual bonds 73.3 (73.3) 0.0

Long-term financial debt 24.9 47.6 72.5

Deferred tax liabilities 203.2 15.2 7.0 0.5 225.9

Short-term financial debt 254.3 (26.6) 227.7

Other non current liabilities 104.4 73.3 177.7

Other current liabilities 279.2 3.3 56.4 338.9

Other liabilities 4,888.9 4,888.9

Total Liabilities 13,296.1 (87.0) 44.2 19.9 2.8 1.4 76.7 13,354.1

107

5

2.1 - Treasury stock

IAS 32 requires all Schneider Electric shares held by

the parent company and subsidiaries to be recorded

as a deduction from equity, whatever the purpose for

which the shares are held. In accordance with this

standard, Schneider Electric shares with a value of

87 million carried in assets in the French GAAP bal-

ance sheet at December 31, 2004, under "Cash and

cash equivalents", have been reclassified as a deduc-

tion from equity.

2.2 - Available-for-sale

financial assets

In accordance with IAS 39, investments in non-consol-

idated companies have been reclassified as available-

for-sale financial assets and measured at fair value

(corresponding to market value in the case of listed

shares). Gains and losses arising from remeasure-

ment at fair value are accumulated in equity under

other reserves.

Fair value adjustments to available-for-sale financial

assets at January 1, 2005 amounted to 44.2 million.

2.3 - Derivative instruments

and hedge accounting

IAS 39 requires all derivative instruments to be recog-

nized in the balance sheet and measured at fair value,

whereas in the French GAAP accounts, these instru-

ments were generally carried off-balance sheet. The

treatment of gains and losses arising from remeasure-

ment at fair value depends on whether or not the instru-

ments qualify for hedge accounting under IAS 39.

Currency instruments qualified as cash flow hedges

under IAS 39 have been recognized in the balance

sheet under other receivables at their fair value of

12.2 million, leading to an adjustment of equity in the

same amount, recorded under other reserves.

Hedges of future metal purchases qualified as cash

flow hedges under IAS 39 have been recognized in the

balance sheet under other receivables at their fair

value of 7.7 million, leading to an adjustment of equi-

ty in the same amount, recorded under other reserves.

2.4 - Derivative instruments

not qualifying for hedge accounting

Derivative instruments not qualifying for hedge account-

ing under IAS 39 have been recognized at fair value in

the balance sheet, in assets for 1.8 million and in lia-

bilities for 3.3 million, leading to corresponding adjust-

ments to equity. The instruments concerned consist

mainly of interest rate hedges on intragroup debt.