Siemens 2007 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2007 Siemens annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

-

297

-

298

-

299

-

300

-

301

-

302

-

303

-

304

-

305

-

306

-

307

-

308

-

309

-

310

-

311

-

312

-

313

-

314

-

315

-

316

-

317

-

318

-

319

-

320

-

321

-

322

-

323

-

324

-

325

-

326

-

327

-

328

-

329

-

330

-

331

-

332

-

333

-

334

-

335

-

336

|

|

Management’s discussion and analysis 119

Management’s discussion and analysis

Fiscal 2007 – Results of Siemens

The following discussion presents selected information for Siemens for the fi scal

years ended:

Siemens booked €83.916 billion in new orders in fi scal 2007. This 12% rise

compared to fi scal 2006 resulted in a book-to-bill ratio of 1.16 for the year. Europe

outside Germany and the Americas were the two largest regions by volume, fol-

lowed by Germany and Asia Pacifi c. Europe outside Germany showed the fastest

growth of any region, with a 19% increase to €26.648 billion for the year led by

strong demand at PG, Med, PTD and A&D and numerous large new contracts.

Orders in Germany were €13.562 billion, up 6% including strong contributions

from A&D, PG and TS.

In the Americas region, orders rose 13% in fi scal 2007, to €22.831 billion,

despite considerable weakening of the U.S. dollar against the euro. Continuing

demand for energy solutions at PG, and for industrial automation solutions at A&D

and I&S, more than compensated for currency and market conditions that led to

reductions in orders in the U.S. at TS, Med, Osram and SBT. As a result, the U.S.

share of orders in the region fell to 73% compared to 78% in fi scal 2006. On an

organic basis, excluding the net effect of portfolio transactions and unusually

strong negative currency translation effects, orders were up 18% and 11% in the

Americas and the U.S. respectively.

Orders in Asia-Pacifi c came in at €13.291 billion, 18% higher than in the prior

year, with PG, A&D, PTD, Med and I&S all winning at least 20% more new business

in the region. Orders in China and India were €4.871 billion and €2.015 billion,

and grew at 12% and 15% respectively, and accounted for 52% of new Asia-Pacifi c

orders. A year earlier, their combined share was 54%. New orders in the Africa,

Near and Middle East, C.I.S. region came in 9% lower year-over-year, at €7.584 bil-

lion, primarily because the prior year included a large order at TS for both trains

and maintenance in Russia. For the region as a whole, PTD, A&D and Osram saw

double-digit order growth for the current period.

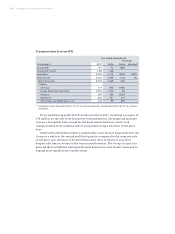

New Orders (location of customer)

Year ended

September 30,

% Change

vs. previous year therein

(€ in millions) 2007 2006 Actual Adjusted* Currency Portfolio

Germany 13,562 12,782 6% 5% 0% 1%

Europe (other than Germany) 26,648 22,351 19% 18% 0% 1%

Americas 22,831 20,202 13% 18% (9)% 4%

Asia-Pacifi c 13,291 11,250 18% 19% (3)% 2%

Africa, Near and

Middle East, C.I.S.** 7,584 8,359 (9)% (7)% (3)% 1%

Siemens 83,916 74,944 12% 13% (3)% 2%

* Excluding currency translation and portfolio effects.

** Commonwealth of Independent States.