Target 2011 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2011 Target annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

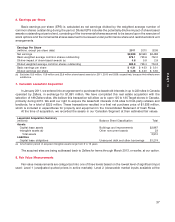

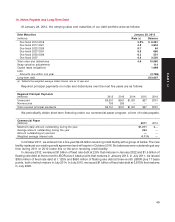

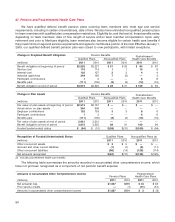

As further explained in Note 10, we maintain an accounts receivable financing program through which we sell

credit card receivables to a bankruptcy remote, wholly owned subsidiary, which in turn transfers the receivables to a

Trust. The Trust, either directly or through related trusts, sells debt securities to third parties.

Nonrecourse Debt Collateralized by Credit Card Receivables

(millions) 2011 2010

Balance at beginning of period $ 3,954 $ 5,375

Issued ——

Accretion (a) 41 45

Repaid (b) (2,995) (1,466)

Balance at end of period $ 1,000 $ 3,954

(a) Represents the accretion of the 7 percent discount on the 47 percent interest in credit card receivables sold to JPMC.

(b) Includes repayments of $226 million and $566 million for the 2008 series of secured borrowings during 2011 and 2010 due to declines in

gross credit card receivables and payment of $2,769 million, excluding the make-whole premium, to repurchase and retire in full this

series of secured borrowings.

Other than debt backed by our credit card receivables, substantially all of our outstanding borrowings are

senior, unsecured obligations. Most of our long-term debt obligations contain covenants related to secured debt

levels. In addition to a secured debt level covenant, our credit facility also contains a debt leverage covenant. We

are, and expect to remain, in compliance with these covenants, which have no practical effect on our ability to pay

dividends.

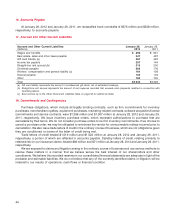

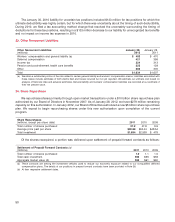

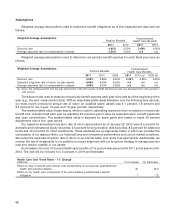

20. Derivative Financial Instruments

Historically our derivative instruments have primarily consisted of interest rate swaps, which are used to

mitigate our interest rate risk. We have counterparty credit risk resulting from our derivative instruments, primarily

with large global financial institutions. We monitor this concentration of counterparty credit risk on an ongoing

basis. See Note 8 for a description of the fair value measurement of our derivative instruments.

In July 2011, in conjunction with our $350 million fixed rate debt issuance, we entered into an interest rate swap

with a matching notional amount, under which we pay a variable rate and receive a fixed rate. This swap has been

designated as a fair value hedge for accounting purposes. At the inception of the hedge, we assessed whether the

swap was highly effective in offsetting changes in fair value of the hedged item and concluded the hedge was

perfectly effective. Therefore, no ineffectiveness was recorded in 2011. We had no derivative instruments

designated as accounting hedges in 2010 or 2009.

Outstanding Interest Rate Swap Summary January 28, 2012

Designated Swap De-designated Swaps

(dollars in millions) Pay Floating Pay Floating Pay Fixed

Weighted average rate:

Pay three-month LIBOR one-month LIBOR 2.6%

Receive 1.0% 5.0% one-month LIBOR

Weighted average maturity 2.5 years 2.4 years 2.4 years

Notional $350 $1,250 $1,250

46