American Express 2014 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

|

|

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 23

REGULATORY MATTERS AND CAPITAL ADEQUACY

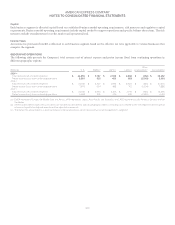

The Company is supervised and regulated by the Federal Reserve and is subject to the Federal Reserve’s requirements for risk-based capital

and leverage ratios. The Company’s two U.S. bank operating subsidiaries, American Express Centurion Bank (Centurion Bank) and

American Express Bank, FSB (FSB) (together, the Banks), are subject to supervision and regulation, including similar regulatory capital

requirements by the Federal Deposit Insurance Corporation (FDIC) and the Office of the Comptroller of the Currency (OCC), respectively.

Under the risk-based capital guidelines of the Federal Reserve, the Company is required to maintain minimum ratios of Common Equity

Tier 1 (CET1), Tier 1 and Total (Tier 1 plus Tier 2) capital to risk-weighted assets, as well as a minimum leverage ratio (Tier 1 capital to

average adjusted on-balance sheet assets).

Failure to meet minimum capital requirements can initiate certain mandatory, and possibly additional, discretionary actions by

regulators, that, if undertaken, could have a direct material effect on the Company’s and the Banks’ operating activities.

As of December 31, 2014 and 2013, the Company and its Banks met all capital requirements to which each was subject and maintained

regulatory capital ratios in excess of those required to qualify as well capitalized.

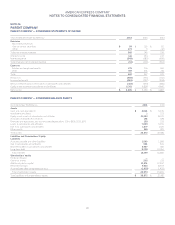

The following table presents the regulatory capital ratios for the Company and the Banks:

(Millions, except percentages)

CET1

capital(b)

Tier 1

capital

Total

capital

CET1

capital ratio(b)

Tier 1

capital ratio

Total

capital ratio

Tier 1

leverage ratio

December 31, 2014:(a)

American Express Company $ 17,525 $ 18,176 $ 20,801 13.1 % 13.6% 15.6% 11.8 %

American Express Centurion Bank 6,174 6,174 6,584 18.8 18.8 20.1 18.7

American Express Bank, FSB 6,722 6,722 7,604 14.2 14.2 16.0 15.1(c)

December 31, 2013:

American Express Company (b) $ 16,174 $ 18,585 (b) 12.5% 14.4% 10.9 %

American Express Centurion Bank (b) 6,366 6,765 (b) 19.9 21.2 19.0

American Express Bank, FSB (b) 6,744 7,662 (b) 15.6 17.7 17.5(c)

Well-capitalized ratios(e) (f) 6.0% 10.0% 5.0 %(d)

Minimum capital ratios(e) 4.0 % 5.5% 8.0% 4.0 %

(a) Beginning in 2014, as a Basel III Advanced Approaches institution, capital ratios are reported using Basel III capital definitions, inclusive of transition provisions

and Basel I risk-weighted assets.

(b) As part of the new Basel III capital rule, effective for 2014, Basel III Advanced Approaches institutions are required to disclose Common Equity Tier 1 capital and

associated ratio.

(c) FSB Tier 1 leverage ratio is calculated using ending total assets in 2013 and average total assets in 2014 as prescribed by OCC regulations applicable to federal

savings banks.

(d) Represents requirements for banking subsidiaries to be considered “well-capitalized” pursuant to regulations issued under the Federal Deposit Insurance

Corporation Improvement Act. There is no “well-capitalized” definition for the Tier 1 leverage ratio for a bank holding company.

(e) As defined by the regulations issued by the Federal Reserve, OCC and FDIC for the year ended December 31, 2014.

(f) Beginning January 1, 2015, Basel III CET1 well-capitalized ratios become relevant capital measures under the prompt and corrective action requirements defined

by the regulations for Advanced Approaches institutions.

116