American Express 2014 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

AMERICAN EXPRESS COMPANY

2014 FINANCIAL REVIEW

CURRENT BUSINESS ENVIRONMENT/OUTLOOK

Our results for 2014 reflect higher spending by our Card Members, growth in average Card Member loans, credit quality indicators at or near

historical lows and continued control over operating expenses, while our strong balance sheet allowed us to return a substantial amount of

capital to our shareholders. We believe we produced solid earnings given the current economic and competitive environment, but recognize

we face a number of increasing challenges in 2015.

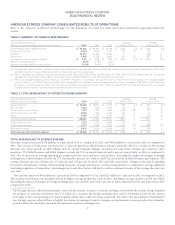

In 2014, we exceeded $1 trillion in annual Card Member global spend on our network for the first time. Card Member billed business

increased 7 percent annually over the prior year, with a modest deceleration of the growth rate in the fourth quarter. Discount revenue

increased 4 percent annually over the prior year. Billed business growth outpaced discount revenue growth primarily due to accelerated

growth of our GNS business (where we share discount revenue we earn from merchants with our issuing bank partners), certain contract

signings and payments made to corporate clients and merchant partners, strong growth in our cash rebate rewards products and changes in

the mix of spending by location and industry. These factors as well as competition and pricing regulation (including regulation of

competitors’ interchange rates) will likely result in a continuation of this trend over time.

Average loans grew 4 percent during 2014, which, along with lower funding costs, led to an 8 percent increase in net interest income. Net

write-off rates remained at or near historically low levels, though the overall rate of improvement slowed in 2014. We expect, at some point,

net write-off rates will increase from these historic lows, which will result in a growth in provision for losses assuming average loans remain

at or above current levels.

As previously noted, our 2014 results include net gains from the business travel joint venture transaction in the second quarter ($626

million pretax) and the sale of our investment in Concur in the fourth quarter ($719 million pretax). We used a substantial portion of those

gains to make additional investments in business building activities and initiatives designed to improve operating efficiencies. Specifically,

marketing, promotion and rewards expenses reflect incremental investments, as well as a charge related to the renewal of our long-term

relationship with Delta. We also undertook restructuring actions in the second quarter ($133 million pretax) and fourth quarter ($313

million pretax) designed to make us more efficient, contain operating expenses, and, as a result, better enable us to invest in new and

enhanced products and services.

Operating expenses for the year decreased 6 percent and adjusted operating expenses, a non-GAAP measure, were flat year over year. Refer

to Table 1 for details of adjusted operating expenses.

While our business is diversified by product and geography, including a range of consumer and commercial card offerings, a large

international business and GNS partners around the world, we face a number of increasing challenges in 2015.

Regulation of the payments industry has increased significantly in recent years and various governments around the world have

established or are proposing to establish payment system regulatory regimes. In the European Union (EU), proposed regulatory changes in

the card payment sector, including the introduction of price regulation, the elimination of honor-all-cards and “anti-steering” rules, and

requirements on granting access to our network, among other important changes, will likely negatively impact the discount revenue derived

from our business in the EU and could significantly limit our flexibility to compete with the more entrenched bankcard networks. See

‘‘Certain Legislative, Regulatory and Other Developments” for additional information on the legislative and regulatory environment.

In addition, global economic growth continues at a modest and mixed pace. Our 2014 results were negatively impacted by the

strengthening U.S. dollar, and we currently expect foreign exchange to have an adverse impact in 2015. Our results could be adversely

affected by increases in short-term interest rates or the failure of the U.S. Congress to continue the renewal of legislation regarding our active

financing income, which could increase our effective tax rate and have an adverse impact on net income in 2015 and beyond.

Competition remains extremely intense across the payments industry. Within the co-brand space, we are focusing on those relationships

that offer the best value to our Card Members while also providing appropriate returns to our business and shareholders. We recently

renewed and extended our relationships with Delta, Starwood and Cathay Pacific. More intense competition has generally increased our cost

of renewing and extending co-brand relationships which are an important component of our business model. We will continue to strive for a

diverse and balanced portfolio of product categories.

20