American Express 2014 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

|

|

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

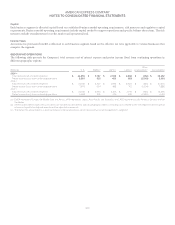

As of December 31, 2014 and 2013, the Company’s most significant concentration of credit risk was with individuals, including Card

Member receivables and loans. These amounts are generally advanced onanunsecuredbasis.However,theCompanyreviewseachpotential

customer’s credit application and evaluates the applicant’s financial history and ability and willingness to repay. The Company also considers

credit performance by customer tenure, industry and geographic location in managing credit exposure.

The following table details the Company’s Card Member loans and receivables exposure (including unused lines-of-credit on Card Member

loans) in the U.S. and outside the U.S. as of December 31:

(Billions) 2014 2013

On-balance sheet:

U.S. $94$89

Non-U.S. 21 22

On-balance sheet(a)(b) 115 111

Unused lines-of-credit – individuals:

U.S. 234 219

Non-U.S. 44 46

Total unused lines-of-credit – individuals $278$265

(a) Represents Card Member loans to individuals as well as receivables from individuals and corporate institutions as discussed in footnotes (a) and (d) from the

previous table.

(b) The remainder of the Company’s on-balance sheet exposure includes cash, investments, other loans, other receivables and other assets including derivative

financial instruments. These balances are primarily within the U.S.

NOTE 25

REPORTABLE OPERATING SEGMENTS AND GEOGRAPHIC OPERATIONS

REPORTABLE OPERATING SEGMENTS

The Company is a leading global payments and travel company that is principally engaged in businesses comprising four reportable

operating segments: USCS, ICS, GCS and GNMS.

The Company considers a combination of factors when evaluating the composition of its reportable operating segments, including the

results reviewed by the chief operating decision maker, economic characteristics, products and services offered, classes of customers, product

distribution channels, geographic considerations (primarily U.S. versus non-U.S.), and regulatory environment considerations. The following

is a brief description of the primary business activities of the Company’s four reportable operating segments:

폷USCS issues a wide range of card products and services to consumers and small businesses in the U.S., and provides consumer travel

services to Card Members and other consumers.

폷ICS issues proprietary consumer and small business cards outside the U.S. and operates coalition loyalty business in various countries.

폷GCS offers global corporate payment services to large and mid-sizedcompanies.TheCompany’sbusinesstraveloperations,whichhad

been included in GCS, were deconsolidated effective June 30, 2014 in connection with the GBT JV transaction.

폷GNMS operates a global payments network that processes and settles proprietary and non-proprietary card transactions. GNMS acquires

merchants and provides point-of-sale products, multi-channel marketing programs and capabilities, services and data, leveraging the

Company’s global closed-loop network. It enters into partnership agreements with third-party card issuers and acquirers, licensing the

American Express brand and extending the reach of the global network.

Corporate functions and certain other businesses, including the Company’s Enterprise Growth Group and other operations, are included in

Corporate & Other.

118