American Express 2014 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

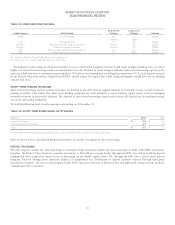

AMERICAN EXPRESS COMPANY

2014 FINANCIAL REVIEW

TABLE 21: UNSECURED DEBT RATINGS

Credit Agency Entity Rated

Short-Term

Ratings

Long-Term

Ratings Outlook

DBRS All rated entities R-1 A Stable

(middle) (high)

Fitch All rated entities F1 A+ Stable

Moody’s TRS and rated operating subsidiaries(a) Prime-1 A2 Stable

Moody’s American Express Company Prime-2 A3 Stable

S&P TRS and rated operating subsidiaries(a)(b) A-2 A- Stable

S&P American Express Company A-2 BBB+ Stable

(a) American Express Travel Related Services Company, Inc.

(b) S&P does not provide a rating for TRS short-term debt.

Downgrades in the ratings of our unsecured debt or asset securitization program securities could result in higher funding costs, as well as

higher fees related to borrowings under our unused lines of credit. Declines in credit ratings could also reduce our borrowing capacity in the

unsecured debt and asset securitization capital markets. We believe our funding mix, including the proportion of U.S. retail deposits insured

by the Federal Deposit Insurance Corporation (FDIC), should reduce the impact that credit rating downgrades would have on our funding

capacity and costs.

SHORT-TERM FUNDING PROGRAMS

Short-term borrowings, such as commercial paper, are defined as any debt with an original maturity of 12 months or less, as well as interest-

bearing overdrafts with banks. Our short-term funding programs are used primarily to meet working capital needs, such as managing

seasonal variations in receivables balances. The amount of short-term borrowings issued in the future will depend on our funding strategy,

our needs and market conditions.

We had the following short-term borrowings outstanding as of December 31:

TABLE 22: SHORT-TERM BORROWINGS OUTSTANDING

(Billions) 2014 2013

Commercial paper(a) $0.8$0.2

Other short-term borrowings 2.7 4.8

Total $3.5$5.0

(a) Average commercial paper outstanding was $0.2 billion and $0.1 billion in 2014 and 2013, respectively.

Refer to Note 9 to the Consolidated Financial Statements for further description of these borrowings.

DEPOSIT PROGRAMS

We offer deposits within our American Express Centurion Bank (Centurion Bank) and American Express Bank, FSB (FSB) subsidiaries

(together, the Banks). These funds are currently insured up to $250,000 per account holder through the FDIC. Our ability to obtain deposit

funding and offer competitive interest rates is dependent on the Banks’ capital levels. We, through the FSB, have a direct retail deposit

program, Personal Savings from American Express, to supplement our distribution of deposit products sourced through third-party

distribution channels. The direct retail program makes FDIC-insured certificates of deposit (CDs) and high-yield savings account products

available directly to consumers.

44