American Express 2014 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

|

|

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

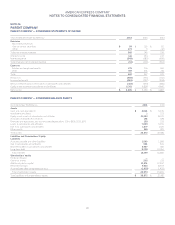

RESTRICTED NET ASSETS OF SUBSIDIARIES

Certain of the Company’s subsidiaries are subject to restrictions on the transfer of net assets under debt agreements and regulatory

requirements. These restrictions have not had any effect on the Company’s shareholder dividend policy and management does not anticipate

any impact in the future. Procedures exist to transfer net assets between the Company and its subsidiaries, while ensuring compliance with

the various contractual and regulatory constraints. As of December 31, 2014, the aggregate amount of net assets of subsidiaries that are

restricted to be transferred to the Company was approximately $11.0 billion.

BANK HOLDING COMPANY DIVIDEND RESTRICTIONS

The Company is limited in its ability to pay dividends by the Federal Reserve, which could prohibit a dividend that would be considered an

unsafe or unsound banking practice. It is the policy of the Federal Reserve that bank holding companies generally should pay dividends on

preferred and common stock only out of net income available to common shareholders generated over the past year, and only if prospective

earnings retention is consistent with the organization’s current and expected future capital needs, asset quality and overall financial

condition. Moreover, bank holding companies are required by statute to be a source of strength to their insured depository institution

subsidiaries and should not maintain dividend levels that undermine their ability to do so. On an annual basis, the Company is required to

develop and maintain a capital plan, which includes planned dividends over a two-year horizon, and to submit the capital plan to the Federal

Reserve.

BANKS’ DIVIDEND RESTRICTIONS

In the years ended December 31, 2014 and 2013, Centurion Bank paid dividends from retained earnings to its parent of $1.9 billion and $1.4

billion, respectively, and FSB paid dividends from retained earnings to its parent of $2.1 billion and $1.8 billion, respectively.

The Banks are subject to statutory and regulatory limitations on their ability to pay dividends. The total amount of dividends that may be

paid at any date, subject to supervisory considerations of the Banks’ regulators, is generally limited to the retained earnings of the respective

bank. As of December 31, 2014 and 2013, the Banks’ retained earnings, in the aggregate, available for the payment of dividends were $3.6

billion and $4.6 billion, respectively. In determining the dividends to pay its parent, the Banks must also consider the effects on applicable

risk-based capital and leverage ratio requirements, as well as policy statements of the federal regulatory agencies. In addition, the Banks’

banking regulators have authority to limit or prohibit the payment of a dividend by the Banks under a number of circumstances, including if,

in the banking regulator’s opinion, payment of a dividend would constitute an unsafe or unsound banking practice in light of the financial

condition of the banking organization.

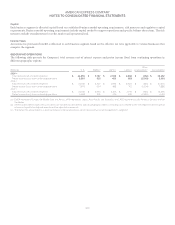

NOTE 24

SIGNIFICANT CREDIT CONCENTRATIONS

Concentrations of credit risk exist when changes in economic, industry or geographic factors similarly affect groups of counterparties whose

aggregate credit exposure is material in relation to American Express’ total credit exposure. The Company’s customers operate in diverse

industries, economic sectors and geographic regions.

ThefollowingtabledetailstheCompany’smaximumcreditexposurebycategory,includingthecreditexposureassociatedwithderivative

financial instruments, as of December 31:

(Billions) 2014 2013

On-balance sheet:

Individuals(a) $101$98

Financial institutions(b) 25 22

U.S. Government and agencies(c) 44

All other(d) 17 17

Total on-balance sheet(e) 147 141

Unused lines-of-credit – individuals(f) $278$265

(a) Individuals primarily include Card Member loans and receivables.

(b) Financial institutions primarily include debt obligations of banks, broker-dealers, insurance companies and savings and loan associations.

(c) U.S. Government and agencies represent debt obligations of the U.S. Government and its agencies, states and municipalities and government-sponsored

entities.

(d) All other primarily includes Card Member receivables from other corporate institutions.

(e) Certain distinctions between categories require management judgment.

(f) Because charge card products generally have no preset spending limit, the associated credit limit on charge products is not quantifiable. Therefore, the

quantified unused line-of-credit amounts only include the approximate credit line available on lending products.

117