American Express 2014 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

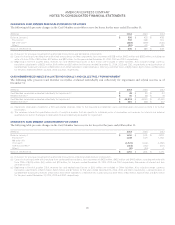

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Reserves for Card Member loans and receivables modified as TDRs are determined as the difference between the cash flows expected to be

received from the Card Member (taking into consideration the probability of subsequent defaults), discounted at the original effective

interest rates, and the carrying value of the Card Member loan or receivable balance. The Company determines the original effective interest

rate as the interest rate in effect prior to the imposition of any penalty interest rate. All changes in the impairment measurement are included

in the provision for losses in the Consolidated Statements of Income.

The following table provides additional information with respect to the Company’s impaired Card Member loans, which are not significant

for GCS, and Card Member receivables, which are not significant for ICS and GCS, as of or for the years ended December 31:

As of December 31, 2014

For the Year Ended

December 31, 2014

2014 (Millions)

Loans over

90 Days

Past Due

& Accruing

Interest(a)

Non-

Accrual

Loans(b)

Loans &

Receivables

Modified

as a TDR(c)

Total

Impaired

Loans &

Receivables

Unpaid

Principal

Balance(d)

Allowance

for TDRs(e)

Average

Balance of

Impaired

Loans

Interest

Income

Recognized

Card Member Loans:

U.S. Card Services $ 161 $ 241 $ 286 $ 688 $ 646 $ 67 $ 750 $ 49

International Card Services 57 — — 57 56 — 62 16

Card Member Receivables:

U.S. Card Services — — 48 48 48 35 47 —

Total $ 218 $ 241 $ 334 $ 793 $ 750 $ 102 $ 859 $ 65

As of December 31, 2013

For the Year Ended

December 31, 2013

2013 (Millions)

Loans over

90 Days

Past Due

& Accruing

Interest(a)

Non-

Accrual

Loans(b)

Loans &

Receivables

Modified

as a TDR(c)

Total

Impaired

Loans &

Receivables

Unpaid

Principal

Balance(d)

Allowance

for TDRs(e)

Average

Balance of

Impaired

Loans

Interest

Income

Recognized

Card Member Loans:

U.S. Card Services(f) $ 167 $ 294 $ 351 $ 812 $ 775 $ 78 $ 948 $ 46

International Card Services 54 4 5 63 62 — 67 16

Card Member Receivables:

U.S. Card Services — — 50 50 49 38 81 —

Total $ 221 $ 298 $ 406 $ 925 $ 886 $ 116 $ 1,096 $ 62

As of December 31, 2012

For the Year Ended

December 31, 2012

2012 (Millions)

Loans over

90 Days

Past Due

& Accruing

Interest(a)

Non-

Accrual

Loans(b)

Loans &

Receivables

Modified

as a TDR(c)

Total

Impaired

Loans &

Receivables

Unpaid

Principal

Balance(d)

Allowance

for TDRs(e)

Average

Balance of

Impaired

Loans

Interest

Income

Recognized

Card Member Loans:

U.S. Card Services $ 73 $ 426 $ 627 $ 1,126 $ 1,073 $ 152 $ 1,221 $ 47

International Card Services 59 5 6 70 69 1 75 16

Card Member Receivables:

U.S. Card Services — — 117 117 111 91 135 —

Total $ 132 $ 431 $ 750 $ 1,313 $ 1,253 $ 244 $ 1,431 $ 63

(a) The Company’s policy is generally to accrue interest through the date of write-off (i.e. 180 days past due). The Company establishes reserves for interest that

the Company believes will not be collected. Amounts presented exclude loans modified as a TDR.

(b) Non-accrual loans not in modification programs include certain Card Member loans placed with outside collection agencies for which the Company has ceased

accruing interest.

(c) Total loans and receivables modified as a TDR includes $34 million, $43 million and $320 million that are non-accrual and $26 million, $29 million and $6 million

that are past due 90 days and still accruing interest as of December 31, 2014, 2013 and 2012, respectively.

(d) Unpaid principal balance consists of Card Member charges billed and excludes other amounts charged directly by the Company such as interest and fees.

(e) Represents the reserve for losses for TDRs, which are evaluated individually for impairment. The Company records a reserve for losses for all impaired loans.

Refer to Card Member Loans Evaluated Individually and Collectively for Impairment in Note 4 for further disclosures regarding the reserve for losses on loans

over 90 days past due and accruing interest and non-accrual loans, which are evaluated collectively for impairment.

(f) For the year 2013, certain amounts and their related reserves have been reclassified between Non-Accrual Loans & Receivables Modified as TDR.

82