American Express 2014 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2014 American Express annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

|

|

AMERICAN EXPRESS COMPANY

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

NOTE 3

ACCOUNTS RECEIVABLE AND LOANS

The Company’s charge and lending payment card products result in the generation of Card Member receivables and Card Member loans,

respectively.

CARD MEMBER AND OTHER RECEIVABLES

Card Member receivables, representing amounts due on charge card products, are recorded at the time a Card Member enters into a point-

of-sale transaction with a merchant. Each charge card transaction is authorized based on its likely economics, a Card Member’s most recent

credit information and spend patterns. Additionally, global spend limits are established to limit the maximum exposure for the Company.

Charge Card Members generally must pay the full amount billed each month. Card Member receivable balances are presented on the

Consolidated Balance Sheets net of reserves for losses (refer to Note 4), and include principal and any related accrued fees.

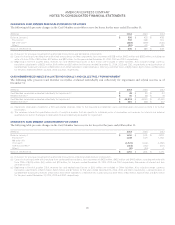

Accounts receivable by segment as of December 31, 2014 and 2013 consisted of:

(Millions) 2014 2013

U.S. Card Services(a) $ 22,468 $21,842

International Card Services 7,653 7,771

Global Commercial Services(b) 14,583 14,391

Global Network & Merchant Services(c) 147 159

Card Member receivables(d) 44,851 44,163

Less: Reserve for losses 465 386

Card Member receivables, net $ 44,386 $ 43,777

Other receivables, net(e) $2,614$3,408

(a) Includes $7.0 billion and $7.3 billion of gross Card Member receivables available to settle obligations of a consolidated VIE as of December 31, 2014 and 2013,

respectively.

(b) Includes $636 million and $836 million due from airlines, of which Delta Air Lines (Delta) comprises $606 million and $628 million as of December 31,2014and

2013, respectively.

(c) Includes receivables primarily related to the Company’s International Currency Card portfolios.

(d) Includes approximately $13.3 billion and $13.8 billion of Card Member receivables outside the U.S. as of December 31, 2014 and 2013, respectively.

(e) Other receivables primarily represent amounts related to (i) certain merchants for billed discount revenue and (ii) GNS partner banks for items such as royalty

andfranchisefees.Additionally,for2013,thebalance also included purchased GNS joint venture receivables. Other receivables are presented net of reserves

for losses of $61 million and $71 million as of December 31, 2014 and 2013, respectively.

CARD MEMBER AND OTHER LOANS

Card Member loans, representing revolving amounts due on lending card products, are recorded at the time a Card Member enters into a

point-of-sale transaction with a merchant, as well as amounts due from charge Card Members who utilize the lending-on-charge feature on

their account and elect to revolve a portion of the outstanding balance by entering into a revolving payment arrangement with the Company.

These loans have a range of terms such as credit limits, interest rates, fees and payment structures, which can be revised over time based on

new information about Card Members and in accordance with applicable regulations and the respective product’s terms and conditions.

Card Members holding revolving loans are typically required to make monthly payments based on pre-established amounts. The amounts

thatCardMemberschoosetorevolvearesubjecttofinancecharges.

Card Member loans are presented on the Consolidated Balance Sheets net of reserves for losses (refer to Note 4), and include principal,

accrued interest and fees receivable. The Company’s policy generally is to cease accruing interest on a Card Member loan at the time the

account is written off, and establish reserves for interest that the Company believes will not be collected.

79