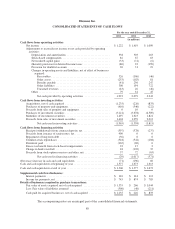

Humana 2012 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2012 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Fair Value

Assets and liabilities measured at fair value are categorized into a fair value hierarchy based on whether the

inputs to valuation techniques are observable or unobservable. Observable inputs reflect market data obtained

from independent sources, while unobservable inputs reflect our own assumptions about the assumptions market

participants would use. The fair value hierarchy includes three levels of inputs that may be used to measure fair

value as described below.

Level 1 – Quoted prices in active markets for identical assets or liabilities. Level 1 assets and liabilities

include debt securities that are traded in an active exchange market.

Level 2 – Observable inputs other than Level 1 prices such as quoted prices in active markets for similar

assets or liabilities, quoted prices for identical or similar assets or liabilities in markets that are not active, or

other inputs that are observable or can be corroborated by observable market data for substantially the full

term of the assets or liabilities. Level 2 assets and liabilities include debt securities with quoted prices that

are traded less frequently than exchange-traded instruments as well as debt securities whose value is

determined using a pricing model with inputs that are observable in the market or can be derived principally

from or corroborated by observable market data.

Level 3 – Unobservable inputs that are supported by little or no market activity and are significant to the fair

value of the assets or liabilities. Level 3 includes assets and liabilities whose value is determined using

pricing models, discounted cash flow methodologies, or similar techniques reflecting our own assumptions

about the assumptions market participants would use as well as those requiring significant management

judgment.

Fair value of actively traded debt securities are based on quoted market prices. Fair value of other debt

securities are based on quoted market prices of identical or similar securities or based on observable inputs like

interest rates generally using a market valuation approach, or, less frequently, an income valuation approach and

are generally classified as Level 2. We obtain at least one quoted price for each security from a third party

pricing service. These prices are generally derived from recently reported trades for identical or similar

securities, including adjustments through the reporting date based upon observable market information. When

quoted prices are not available, the third party pricing service may use quoted market prices of comparable

securities or discounted cash flow analyses, incorporating inputs that are currently observable in the markets for

similar securities. Inputs that are often used in the valuation methodologies include benchmark yields, reported

trades, credit spreads, broker quotes, default rates, and prepayment speeds. We are responsible for the

determination of fair value and as such we perform analysis on the prices received from the third party pricing

service to determine whether the prices are reasonable estimates of fair value. Our analysis includes a review of

monthly price fluctuations as well as a quarterly comparison of the prices received from the pricing service to

prices reported by our third party investment advisor. In addition, on a quarterly basis we examine the underlying

inputs and assumptions for a sample of individual securities across asset classes, credit rating levels, and various

durations.

Fair value of privately held debt securities, including venture capital investments as well as auction rate

securities, are estimated using a variety of valuation methodologies, including both market and income

approaches, where an observable quoted market does not exist and are generally classified as Level 3. For

privately-held debt securities, such methodologies include reviewing the value ascribed to the most recent

financing, comparing the security with securities of publicly-traded companies in similar lines of business, and

reviewing the underlying financial performance including estimating discounted cash flows. Auction rate

securities are debt instruments with interest rates that reset through periodic short-term auctions. From time to

time, liquidity issues in the credit markets have led to failed auctions. Given the liquidity issues, fair value could

98