Humana 2012 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2012 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

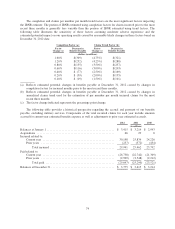

Interest rate risk also represents a market risk factor affecting our consolidated financial position due to our

significant investment portfolio, consisting primarily of fixed maturity securities of investment-grade quality

with a weighted average S&P credit rating of AA- at December 31, 2012. Our net unrealized position improved

$203 million from a net unrealized gain position of $525 million at December 31, 2011 to a net unrealized gain

position of $728 million at December 31, 2012. At December 31, 2012, we had gross unrealized losses of $8

million on our investment portfolio primarily due to an increase in market interest rates and tighter liquidity

conditions in the current markets than when the securities were purchased, and as such, there were no material

other-than-temporary impairments during 2012. While we believe that these impairments are temporary and we

currently do not have the intent to sell such securities, given the current market conditions and the significant

judgments involved, there is a continuing risk that future declines in fair value may occur and material realized

losses from sales or other-than-temporary impairments may be recorded in future periods.

Duration is the time-weighted average of the present value of the bond portfolio’s cash flow. Duration is

indicative of the relationship between changes in fair value and changes in interest rates, providing a general

indication of the sensitivity of the fair values of our fixed maturity securities to changes in interest rates.

However, actual fair values may differ significantly from estimates based on duration. The average duration of

our investment portfolio, including cash and cash equivalents, was approximately 4.0 years as of December 31,

2012 and 3.9 years as of December 31, 2011. Based on the duration including cash equivalents, a 1% increase in

interest rates would generally decrease the fair value of our securities by approximately $443 million.

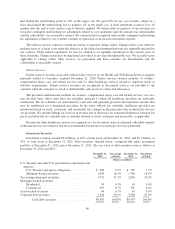

We have also evaluated the impact on our investment income and interest expense resulting from a hypothetical

change in interest rates of 100, 200, and 300 basis points over the next twelve-month period, as reflected in the

following table. The evaluation was based on our investment portfolio and our outstanding indebtedness at

December 31, 2012 and 2011. Our investment portfolio consists of cash, cash equivalents, and investment securities.

The modeling technique used to calculate the pro forma net change in pretax earnings considered the cash flows related

to fixed income investments and debt, which are subject to interest rate changes during a prospective twelve-month

period. This evaluation measures parallel shifts in interest rates and may not account for certain unpredictable events

that may affect interest income, including unexpected changes of cash flows into and out of the portfolio, changes in

the asset allocation, including shifts between taxable and tax-exempt securities, and spread changes specific to various

investment categories. In the past ten years, changes in 3 month LIBOR rates during the year have exceeded 300 basis

points once, have not changed between 200 and 300 basis points, have changed between 100 and 200 basis points four

times, and have changed by less than 100 basis points five times.

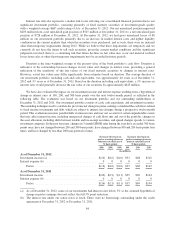

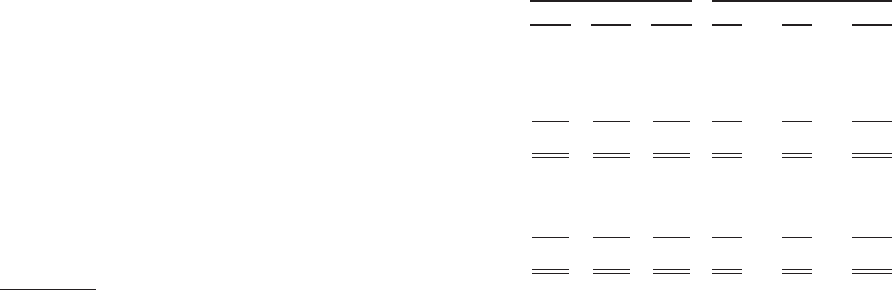

Increase (decrease) in

pretax earnings given an

interest rate decrease of

X basis points

Increase (decrease) in

pretax earnings given an

interest rate increase of

X basis points

(300) (200) (100) 100 200 300

(in millions)

As of December 31, 2012

Investment income (a) ................................ $(16) $(16) $(10) $33 $68 $102

Interest expense (b) ................................... 0 0 0 0 0 0

Pretax ......................................... $(16) $(16) $(10) $33 $68 $102

As of December 31, 2011

Investment income ................................... $(26) $(21) $(11) $35 $69 $104

Interest expense (b) ................................... 0 0 0 0 0 0

Pretax ......................................... $(26) $(21) $(11) $35 $69 $104

(a) As of December 31, 2012, some of our investments had interest rates below 3% so the assumed hypothetical

change in pretax earnings does not reflect the full 3% point reduction.

(b) The interest rate under our senior notes is fixed. There were no borrowings outstanding under the credit

agreement at December 31, 2012 or December 31, 2011.

84