Humana 2012 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2012 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

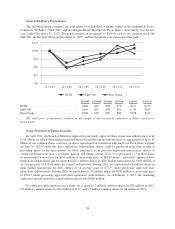

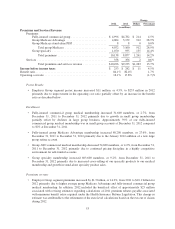

• Year-over-year comparisons within Other Businesses are impacted by the transition to the new

TRICARE South Region contract on April 1, 2012, including a change in profitability under the new

contract in connection with our bid strategy, benefits expense of approximately $46 million incurred

related to the settlement of litigation associated with our military services business during 2012, and

benefits expense of $29 million for reserve strengthening associated with our closed-block of long-term

care policies during 2012 as discussed in Note 17 to the consolidated financial statements included in

Item 8. – Financial Statements and Supplementary Data.

Health Insurance Reform

The Patient Protection and Affordable Care Act and The Health Care and Education Reconciliation Act of

2010 (which we collectively refer to as the Health Insurance Reform Legislation) enacted significant reforms to

various aspects of the U.S. health insurance industry. While regulations and interpretive guidance on some

provisions of the Health Insurance Reform Legislation have been issued to date by the Department of Health and

Human Services, or HHS, the Department of Labor, the Treasury Department, and the National Association of

Insurance Commissioners, there are many provisions of the legislation that will require additional guidance and

clarification in the form of regulations and interpretations in order to fully understand the impacts of the

legislation on our overall business, which we expect to occur over the next several years.

Implementation dates of the Health Insurance Reform Legislation began in September 2010 and continue

through 2018. The following outlines certain provisions of the Health Insurance Reform Legislation:

• Many changes are already effective and have been implemented by the Company, including:

elimination of pre-existing condition limits for enrollees under age 19, elimination of certain annual

and lifetime caps on the dollar value of benefits, expansion of dependent coverage to include adult

children until age 26, a requirement to provide coverage for prescribed preventive services without cost

to members, new claim appeal requirements, and the establishment of an interim high risk program for

those unable to obtain coverage due to a pre-existing condition or health status.

• Effective January 1, 2011, minimum benefit ratios were mandated for all commercial fully-insured

medical plans in the large group (85%), small group (80%), and individual (80%) markets, with annual

rebates to policyholders if the actual benefit ratios, calculated in a manner prescribed by HHS, do not

meet these minimums. We began accruing for rebates in 2011, based on the manner prescribed by

HHS, with initial rebate payments made in July 2012. Our benefit ratios reported herein, calculated

from financial statements prepared in accordance with accounting principles generally accepted in the

United States of America, or GAAP, differ from the benefit ratios calculated as prescribed by HHS

under the Health Insurance Reform Legislation. The more noteworthy differences include the fact that

the benefit ratio calculations prescribed by HHS are calculated separately by state and legal entity;

independently for individual, small group, and large group fully-insured products; reflect actuarial

adjustments where the membership levels are not large enough to create credible size; exclude some of

our health insurance products; include taxes and fees as reductions of premium; treat changes in

reserves differently than GAAP; and classify rebate amounts as additions to incurred claims as opposed

to adjustments to premiums for GAAP reporting.

• Medicare Advantage payment benchmarks for 2011 were frozen at 2010 levels and in 2012, additional

cuts to Medicare Advantage plan payments began to take effect (with plan payment benchmarks

ultimately ranging from 95% in high-cost areas to 115% in low-cost areas of Medicare fee-for-service

rates), with changes being phased-in over two to six years, depending on the level of payment

reduction in a county. In addition, beginning in 2011 the gap in coverage for Medicare Part D

prescription drug coverage is incrementally closing.

• Beginning in 2014, the Health Insurance Reform Legislation requires: all individual and group health

plans to guarantee issuance and renew coverage without pre-existing condition exclusions or health-

status rating adjustments; the elimination of annual limits on coverage on certain plans; the

45