Humana 2012 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2012 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

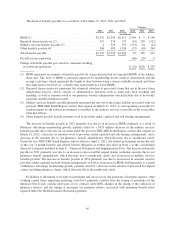

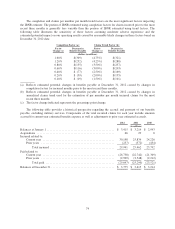

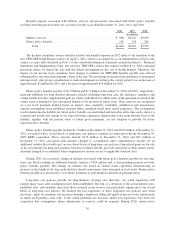

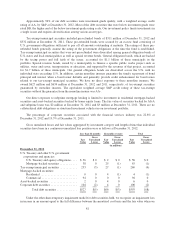

The following table summarizes the changes in estimate for incurred claims related to prior years

attributable to our key assumptions. As previously described, our key assumptions consist of trend and

completion factors estimated using an assumption of moderately adverse conditions. The amounts below

represent the difference between our original estimates and the actual benefits expense ultimately incurred as

determined from subsequent claim payments.

Favorable Development by Changes in Key Assumptions

2012 2011 2010

Amount

Factor

Change (a) Amount

Factor

Change (a) Amount

Factor

Change (a)

(dollars in millions)

Trend factors ....................... $(138) (2.4)% $(189) (3.8)% $(213) (4.7)%

Completion factors .................. (119) 0.7% (183) 1.2% (221) 1.6%

Total ......................... $(257) $(372) $(434)

(a) The factor change indicated represents the percentage point change.

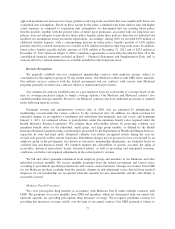

As previously discussed, our reserving practice is to consistently recognize the actuarial best estimate of our

ultimate liability for claims. Actuarial standards require the use of assumptions based on moderately adverse

experience, which generally results in favorable reserve development, or reserves that are considered redundant.

There was favorable medical claims reserve development related to prior fiscal years of $257 million in 2012,

$372 million in 2011, and $434 million in 2010. The table below details our favorable medical claims reserve

development related to prior fiscal years by segment for 2012, 2011, and 2010.

Favorable Medical Claims Reserve

Development Change

2012 2011 2010 2012 2011

(in millions)

Retail Segment ................................... $(192) $(245) $(343) $ (53) $(98)

Employer Group Segment .......................... (48) (114) (73) (66) 41

Other Businesses ................................. (17) (13) (18) 4 (5)

Total ........................................... $(257) $(372) $(434) $(115) $(62)

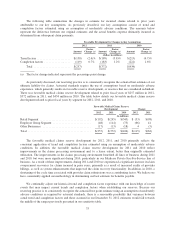

The favorable medical claims reserve development for 2012, 2011, and 2010 primarily reflects the

consistent application of trend and completion factors estimated using an assumption of moderately adverse

conditions. In addition, the favorable medical claims reserve development for 2011 and 2010 reflect

improvements in the claims processing environment and, to a lesser extent, better than originally estimated

utilization. The improvements in the claims processing environment benefited all lines of business during 2011

and 2010, but were more significant during 2010, particularly in our Medicare Private Fee-For-Service line of

business. As a result of these improvements, during 2011 and 2010 we experienced a significant increase in claim

overpayment recoveries for claims incurred in prior years, primarily as a result of increased audits of provider

billings, as well as system enhancements that improved the claim recovery functionality. In addition, in 2010, a

shortening of the cycle time associated with provider claim submissions was a contributing factor. We believe we

have consistently applied our methodology in determining our best estimate for benefits payable.

We continually adjust our historical trend and completion factor experience with our knowledge of recent

events that may impact current trends and completion factors when establishing our reserves. Because our

reserving practice is to consistently recognize the actuarial best point estimate using an assumption of moderately

adverse conditions as required by actuarial standards, there is a reasonable possibility that variances between

actual trend and completion factors and those assumed in our December 31, 2012 estimates would fall towards

the middle of the ranges previously presented in our sensitivity table.

75