Bank of America 2003 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

Debit card purchase volumes grew 22 percent while consumer

credit card purchases increased 13 percent in 2003 from 2002. Total

managed consumer credit card revenue, including interest income,

increased 25 percent in 2003. Average managed consumer credit

card receivables grew 15 percent in 2003 due to new account growth

from direct marketing programs and the branch network.

Asse t Manage me nt exceeded its goal of increasing the number

of financial advisors by 20 percent and ended the year with 1,150

financial advisors. The Premier Banking and Investments partnership

has developed an integrated financial services model and as a com-

ponent of the continued strategic distribution channel expansion

opened 10 new wealth centers. In addition, Marsico Capital

Management, LLC’s (Marsico) assets under management more than

doubled to $30.2 billion at December 31, 2003.

Global Corporate and Inve stme nt Banking maintained market

share in syndicated loans and fixed income areas and gained in areas

such as mergers and acquisitions and mortgage-backed securities.

Continued improvements in credit quality in our large corporate port-

folio drove the $731 million, or 61 percent, decrease in provision for

credit losses in Global Corporate and Inve stme nt Banking. Net charge-

offs in 2003 in the large corporate portfolio were at their lowest lev-

els in three years. In addition, large corporate nonperforming assets

dropped $1.7 billion, or 57 percent.

Financial Highlights

Net interest income on a fully taxable-equivalent basis increased $596

million to $22.1 billion in 2003. This increase was driven by higher

asset and liability management (ALM) portfolio levels (consisting of

securities, whole loan mortgages and derivatives), higher consumer

loan levels, larger trading-related contributions, higher mortgage ware-

house and core deposit funding levels. Partially offsetting these

increases was the impact of lower interest rates and reductions in the

large corporate, foreign and exited consumer loan businesses portfo-

lios. The net interest yield on a fully taxable-equivalent basis declined

39 basis points (bps) to 3.36 percent in 2003 due to the negative

impact of increases in lower-yielding trading-related assets and declin-

ing rates offset partially by our ALM portfolio repositioning.

Noninterest income increased $2.9 billion to $16.4 billion in

2003, due to increases in (i) mortgage banking income of $1.2 billion,

(ii) equity investment gains of $495 million, (iii) other noninterest

income of $485 million, (iv) card income of $432 million and (v) con-

sumer-based fee income of $244 million. The increase in mortgage

banking income was driven by gains from higher volumes of mortgage

loans sold into the secondary market and improved profit margins.

Other noninterest income of $1.1 billion included gains of $772 mil-

lion, an increase of $272 million over 2002, as we sold whole loan

mortgages to manage prepayment risk due to the longer than antici-

pated low interest rate environment. Additionally, other noninterest

income included the equity in the earnings of our investment in Grupo

Financiero Santander Serfin (GFSS) of $122 million.

Gains on sales of debt securities in 2003 and 2002, were $941

million and $630 million, respectively, as we continued to reposition

the ALM portfolio in response to interest rate fluctuations.

The provision for credit losses declined $858 million to $2.8 bil-

lion in 2003 due to an improvement in the commercial portfolio

partially offset by a stable but growing consumer portfolio.

Nonperforming assets decreased $2.2 billion to $3.0 billion, or 0.81

percent of loans, leases and foreclosed properties at December 31,

2003 compared to 1.53 percent at December 31, 2002. This decline

was driven by reduced levels of inflows to nonperforming assets in

Global Corporate and Inve stme nt Banking,together with loan sales and

payoffs facilitated by high levels of liquidity in the capital markets.

Noninterest expense increased $1.7 billion in 2003 from 2002,

driven by higher personnel costs, increased professional fees includ-

ing legal expense and increased marketing expense. Higher personnel

costs resulted from increased costs of employee benefits of $504

million and revenue-related incentives of $435 million. Employee ben-

efits expense increased due to stock option expense of $120 million

in 2003 and the impacts of a change in the expected long-term rates

of return on plan assets to 8.5 percent for 2003 from 9.5 percent in

2002 and a change in the discount rate to 6.75 percent in 2003 from

7.25 percent in 2002 for the Bank of America Pension Plan. The

increase in professional fees of $319 million was driven by an

increase in litigation accruals of $220 million associated with pend-

ing litigation principally related to securities matters. Marketing

expense increased by $232 million due to higher advertising costs,

as well as marketing investments in direct marketing for the credit

card business. In addition, recorded in other expense during the third

quarter of 2003 was a $100 million charge related to issues sur-

rounding our mutual fund practices.

Income tax expense was $5.1 billion reflecting an effective tax

rate of 31.8 percent in 2003 compared to $3.7 billion and 28.8 per-

cent in 2002, respectively. The 2002 effective tax rate was impacted

by a $488 million reduction in income tax expense resulting from a

settlement with the IRS generally covering tax years ranging from

1984 to 1999 but including tax returns as far back as 1971.

The result of the above was a 17 percent growth in net income

in 2003 compared to 2002. Management does not currently expect

that this level of growth will recur in 2004.

FleetBoston Merger

On October 27, 2003, we announced a definitive agreement to merge

with FleetBoston Financial Corporation (FleetBoston). The merger is

expected to create a banking institution with a truly national scope,

with an increased presence in America’s growth and wealth markets

and leading market shares throughout the Northeast, Southeast,

Southwest, Midwest and West regions of the United States. The

merger will be a stock-for-stock transaction with a purchase price

currently estimated to be approximately $46.0 billion. Each share of

FleetBoston common stock will be exchanged for 0.5553 of a share

of our common stock, resulting in the issuance of approximately 600

million shares of our common stock. FleetBoston shareholders will

receive cash instead of any fractional shares of our common stock

that would have otherwise been issued at the completion of the merger.

The agreement has been approved by both boards of directors and is

subject to customary regulatory and shareholder approvals. The clos-

ing is expected in April of 2004. At the time of the merger announce-

ment, we anticipated repurchasing approximately 67 million shares

through 2004 and 23 million shares in 2005, net of option exercises,

as a result of the merger. The effect on our liquidity of this transac-

tion is expected to be minimal.

In connection with the merger, we have been developing a plan

to integrate our operations with FleetBoston’s. The integration costs

have been estimated to be $800 million after-tax, or $1.3 billion

pre-tax. The specific details of this plan will continue to be refined

over the next several months.

Fourth Quarter 2003 Results

Net income totaled $2.7 billion, or $1.83 per diluted common share

for the fourth quarter of 2003. The return on average common share-

holders’ equity was 22 percent for the three months ended

December 31, 2003. Total revenue on a fully taxable-equivalent basis

was $9.8 billion. Fully taxable-equivalent net interest income

increased $268 million to $5.7 billion from third quarter 2003 levels

due to the impact of interest rates, higher ALM portfolio levels and

higher levels of consumer loans offset by lower mortgage warehouse

levels. Mortgage banking income decreased to $292 million in the

fourth quarter from $666 million in the third quarter of 2003 due to

lower levels of refinancing production. Equity investment gains were

$215 million in the fourth quarter of 2003 due to $212 million in

gains from securities sold that were received in satisfaction of debt

that had been restructured and charged off in prior periods. Trading-

related results were negatively impacted as we marked down the

value of our derivative exposure by $92 million relating to Parmalat

Finanziera SpA and its related entities (Parmalat). For additional infor-

mation on our exposure to Parmalat see “Credit Quality Performance”

beginning on page 46. Gains recognized in our whole mortgage loan

portfolio were $48 million in the fourth quarter of 2003 compared to

$197 million in the third quarter of 2003. During the quarter, we gen-

erated $139 million in gains on sales of debt securities compared to

$233 million in the third quarter of 2003. The income tax rate

decreased from 31.3 percent in the third quarter of 2003 to 30.2

percent in the fourth quarter of 2003 due to adjustments related to

our normal tax accrual review, tax refunds received and reductions in

previously accrued taxes.

26 BANK OF AMERICA 2003 BANK OF AMERICA 2003 27

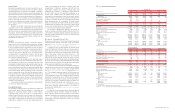

Table 1

Five-Year Summary of Selected Financial Data(1)

(Dollars in millions, except per share information)

2003 2002 2001 2000 1999

Income statement

Net interest income

$21,464 $20,923 $ 20,290 $ 18,349 $ 18,127

Noninterest income

16,422 13,571 14,348 14,582 14,179

Total revenue

37,886 34,494 34,638 32,931 32,306

Provision for credit losses

2,839 3,697 4,287 2,535 1,820

Gains on sales of debt securities

941 630 475 25 240

Noninterest expense

20,127 18,436 20,709 18,633 18,511

Income before income taxes

15,861 12,991 10,117 11,788 12,215

Income tax expense

5,051 3,742 3,325 4,271 4,333

Net income

10,810 9,249 6,792 7,517 7,882

Average common shares issued and outstanding (in thousands)

1,486,703 1,520,042 1,594,957 1,646,398 1,726,0

06

Average diluted common shares issued and outstanding (in thousands)

1,515,178 1,565,467 1,625,654 1,664,929 1,760,0

58

Performance ratios

Return on average assets

1.41% 1.40% 1.04% 1.12% 1.28

%

Return on average common shareholders’ equity

21.99 19.44 13.96 15.96 16.93

Total equity to total assets (at year end)

6.52 7.61 7.80 7.41 7.02

Total average equity to total average assets

6.44 7.18 7.49 7.01 7.55

Dividend payout

39.58 40.07 53.44 45.02 40.54

Per common share data

Earnings

$7.27 $6.08 $ 4.26 $ 4.56 $ 4.56

Diluted earnings

7.13 5.91 4.18 4.52 4.48

Dividends paid

2.88 2.44 2.28 2.06 1.85

Book value

33.26

33.

49 31.07 29.47 26.44

Average balance sheet

Total loans and leases

$356,148 $336,819 $ 365,447 $ 392,622 $ 362,783

Total assets

764,132 662,943 650,083 672,067 617,352

Total deposits

406,233 371,479 362,653 353,294 341,748

Long-term debt(2)

68,432 66,045 69,622 70,293 57,574

Common shareholders’ equity

49,148 47,552 48,609 47,057 46,527

Total shareholders’ equity

49,204 47,613 48,678 47,132 46,601

Capital ratios (at year end)

Risk-based capital:

Tier 1 capital

7.85% 8.22% 8.30% 7.50% 7.35

%

Total capital

11.87 12.43 12.67 11.04 10.88

Leverage

5.73 6.29 6.55 6.11 6.26

Market price per share of common stock

Closing

$80.43 $69.57 $ 62.95 $ 45.88 $ 50.19

High closing

83.53 76.90 65.00 59.25 75.50

Low closing

65.63 54.15 46.75 38.00 48.00

(1) As a result of the adoption of Statement of Financial Accounting Standards (SFAS) No. 142 “Goodwill and Other Intangible Assets” (SFAS 142) on January 1, 2002, the Corporation no longer amortizes

goodwill. Goodwill amortization expense was $662, $635 and $635 in 2001, 2000 and 1999, respectively.

(2) Includes long-term debt related to trust preferred securities (Trust Securities).