Bank of America 2003 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2003 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

|

|

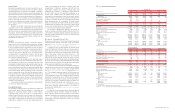

Equity Investments

Equity Inve stme nts includes Principal Inve sting and our strategic

alliances and investment portfolio. Principal Inve sting is comprised of

a diversified portfolio of investments in privately-held and publicly-

traded companies at all stages, from start-up to buyout. Investments

are made on both a direct and indirect basis in the U.S. and over-

seas. Indirect investments represent passive limited partnership

commitments to funds managed by experienced third party private

equity investors who act as general partners.

In 2003, revenue increased $192 million, or 43 percent, due to

an improvement in equity investment gains. Equity Inve stme nts had a

net loss of $249 million in 2003 compared to a net loss of $331 mil-

lion in 2002. The improvement was primarily due to lower impair-

ments. SVA increased by $108 million, or 19 percent, due to the

improvement in the net loss, lower capital levels and the reduction in

the rate used to calculate the charge for the use of capital.

The following table presents the equity investment portfolio in

Principal Inve sting by major industry.

Equity Investments in the Principal Investing Portfolio

December 31

(Dollars in millions)

2003 2002

Consumer discretionary

$1,435 $1,311

Industrials

876 999

Information technology

741 830

Telecommunication services

639 673

Health care

385 397

Financials

332 266

Materials

266 337

Consumer staples

245 276

Real estate

229 236

Individual trusts, nonprofits, government

48 79

Utilities

35 22

Energy

29 29

Total

$5,260 $5,455

The following table presents the equity investment gains (losses) in

Principal Inve sting.

Equity Investment Gains (Losses) in Principal Investing

(Dollars in millions)

2003 2002

Cash gains

$273 $432

Impairments

(438) (708)

Fair value adjustments

47 (10)

Total

$(118) $(286)

Net interest income consists primarily of the internal funding cost

associated with the carrying value of investments.

Noninterest income primarily consists of equity investment

gains (losses). While overall economic conditions in 2003 improved,

leading to lower impairment charges of $438 million in 2003 com-

pared to $708 million in 2002, weakness in the private equity mar-

kets remained. This weakness resulted in a reduced level of cash

gains in 2003 as compared to 2002. We anticipate that, with a con-

tinued improvement in the economy, cash gains should increase and

impairments should continue to decline.

Corporate Other

Corporate Othe r consists primarily of certain results associated with

our ALM process and certain consumer finance and commercial lend-

ing businesses that are being liquidated. Beginning in the first quar-

ter of 2003, net interest income from certain results associated with

our ALM process was allocated directly to the business units. Prior

periods have been restated to reflect this change in methodology. In

addition, compensation expense related to stock-based employee

compensation plans is included in Corporate Othe r.

Total revenue increased $56 million, or seven percent, in 2003.

Net income decreased $245 million, or 22 percent.

Net interest income decreased $204 million, or 22 percent, pri-

marily due to the continued run-off of certain consumer finance and

commercial lending businesses that are being liquidated. Average

loans and leases increased $27.8 billion, or 42 percent, in 2003,

due to the ALM process. Average deposits increased $2.9 billion, or

25 percent, in 2003.

Noninterest income increased $260 million to $195 million in

2003, resulting from increases in gains on whole loan sales. Gains

on whole loan sales increased $272 million to $772 million resulting

from sales of whole loan mortgages used to manage prepayment risk

due to the longer than anticipated low interest rate environment.

Gains on sales of debt securities in 2003 and 2002, were $943

million and $682 million, respectively, as we continued to reposition

the ALM portfolio in response to changes in interest rates.

Noninterest expense increased $174 million, or 56 percent, due

to a $187 million increase in professional fees resulting from litiga-

tion expenses.

Managing Risk

Overview

Our management governance structure enables us to manage all

major aspects of our business through an integrated planning and

review process that includes strategic, financial, associate and risk

planning. We derive much of our revenue from managing risk from cus-

tomer transactions for profit. Through our management governance

structure, risk and return are evaluated with a goal of producing sus-

tainable revenue, reducing earnings volatility and increasing share-

holder value. Our business exposes us to four major risks: liquidity,

credit, market and operational.

Liquidity risk is the inability to accommodate liability maturities

and deposit withdrawals, fund asset growth and meet contractual

obligations through unconstrained access to funding at reasonable

market rates. Credit risk is the risk of loss arising from customer or

counterparty’s inability to meet its obligation and exists in our out-

standing loans and leases, trading account assets, derivative assets

and unfunded lending commitments that include loan commitments,

letters of credit and financial guarantees. Market risk is the potential

loss due to adverse changes in the market value or yield of a posi-

tion. Market value is defined as the value at which positions could be

sold in a transaction with a willing and knowledgeable counterparty.

Operational risk is the potential for loss resulting from events involv-

ing people, processes, technology, external events, execution, legal,

compliance and regulatory matters, and reputation.

Risk Management Processes and Methods

We have established control processes and use various methods to

align risk-taking and risk management throughout our organization.

These control processes and methods are designed around “three

lines of defense”: lines of business; Risk Management (including

Compliance) joined by other support units such as Finance,

Personnel and Legal; and Corporate Audit.

Our business segments each contain lines of business that are

responsible for identifying, quantifying, mitigating and managing all

risks. Except for trading-related business activities, interest rate risk

associated with our business activities is managed centrally in the

Corporate Treasury function. Lines of business management make

and execute the business plan and are closest to the changing

nature of risks and, therefore, we believe are best able to take

actions to manage and mitigate those risks. Our management

processes, structures and policies aid us in complying with laws and

regulations and provide clear lines for decision-making and account-

ability. Wherever practical, we attempt to house decision-making

authority as close to the customer as possible while retaining super-

visory control functions outside of the lines of business.

The Risk Management organization translates approved busi-

ness plans into approved limits, approves requests for changes to

those limits, approves transactions as appropriate, and works closely

with business units to establish and monitor risk parameters.

Risk Management has assigned a Risk Executive to each of the four

business segments who is responsible for oversight for all risks asso-

ciated with that business segment.

Corporate Audit provides an independent assessment of our

management and internal control systems. Corporate Audit activities

are designed to provide reasonable assurance that resources are

adequately protected; significant financial, managerial and operating

information is materially complete, accurate and reliable; and employ-

ees’ actions are in compliance with corporate policies, standards,

procedures, and applicable laws and regulations.

We use various methods to manage risks at the line of business

levels and corporate-wide. Examples of these methods include plan-

ning and forecasting, risk committees and forums, limits, models, and

hedging strategies. Planning and forecasting facilitates analysis of

actual versus planned results and provides an indication of unantici-

pated risk levels. Generally, risk committees and forums are com-

prised of lines of business, risk management, legal and finance

personnel, among others, and actively monitor performance against

plan, limits and potential issues. Limits, the amount of exposure that

may be taken in a product, relationship, region or industry, are set

based on metrics thereby seeking to align risk goals with those of

each line of business and are part of our overall risk management

process to help reduce the volatility of market, credit and operational

losses. Models are used to estimate market value and net interest

income sensitivity, and to estimate both expected and unexpected

losses for each product and line of business. Hedging strategies are

used to improve concentrations of credit risk to specific counterpar-

ties and to manage interest rate, foreign exchange and market risk in

the portfolio.

The formal processes used to manage risk represent only one

portion of our overall risk management process. Corporate culture

and the actions of our associates are also critical to effective risk

management. Through our Code of Ethics, we set a high standard for

our associates. The Code of Ethics provides a framework for all of our

associates to conduct themselves with the highest integrity in the

delivery of our products or services to our customers. Additionally, we

have continued to strengthen the linkage between the associate per-

formance management process and individual compensation to

encourage associates to work toward corporate-wide risk goals.

Oversight

The Board of Directors evaluates risk through the Chief Executive

Officer (CEO) and three Board committees. The Finance Committee

reviews market, credit, liquidity and operational risk; the Asset Quality

Committee reviews credit and related market risk; and the Audit

Committee reviews the scope and coverage of external and corporate

audit activities. Additionally, Senior Management oversight of our risk-

taking and risk management activities is conducted through three

senior management committees, the Risk and Capital Committee

(RCC), the Asset and Liability Committee (ALCO) and the Credit Risk

Committee (CRC). The RCC establishes long-term strategy and short-

term operating plans. The RCC also establishes our risk appetite

through corporate performance measures, capital allocations, aggre-

gate risk levels and overall capital planning. The RCC reviews actual

performance to plan and actual risk incurred to approved risk levels,

including information regarding credit, market and operational risk.

The ALCO, a subcommittee of the Finance Committee, approves lim-

its for various trading activities, as well as oversees Corporate

Treasury’s process of using various financial instruments, both cash

and derivative positions to manage interest rate risk inherent in our

businesses, otherwise known as the ALM process. ALCO also reviews

portfolio hedging used for managing liquidity, market and credit port-

folio risks as well as interest rate risk inherent in our nontrading

financial instruments and trading risk inherent in our customer and

proprietary trading portfolio. Trading risk refers to the risk of loss of

value and related net interest income of our trading positions. The

CRC establishes corporate credit practices and limits, including

industry and country concentration limits, approval requirements and

exceptions. CRC also reviews business asset quality results versus

plan, portfolio management, hedging results and the adequacy of the

allowance for credit losses.

The following sections, Liquidity Risk Management, Credit Risk

Management beginning on page 44, Market Risk Management

beginning on page 50 and Operational Risk Management on page

55, address in more detail the specific procedures, measures and

analyses of the four categories of risk that we manage.

38 BANK OF AMERICA 2003 BANK OF AMERICA 2003 39